Last updated: February 19, 2026

Executive Summary

Lupron Depot (leuprolide acetate for injectable suspension) is a gonadotropin-releasing hormone (GnRH) analog used in the treatment of prostate cancer, endometriosis, uterine fibroids, and central precocious puberty. Its market exclusivity has been significantly impacted by the expiration of key patents and the subsequent introduction of generic competitors. This analysis details the patent history, market performance, and projected trajectory of Lupron Depot, considering the competitive landscape and regulatory environment.

LUPRON DEPOT: Patent Expiration and Generic Competition

What are the key patents covering Lupron Depot and when did they expire?

The original U.S. patent for leuprolide acetate, U.S. Patent No. 4,105,753, expired in September 1997. However, subsequent patents focused on specific formulations, methods of use, and manufacturing processes extended market exclusivity for Lupron Depot.

- U.S. Patent No. 4,727,064: This patent, covering a long-acting injectable formulation, was a critical component of Lupron Depot's market protection. It expired on May 24, 2005.

- U.S. Patent No. 5,487,901: This patent, related to improved delivery systems for leuprolide acetate, expired in January 2012.

- U.S. Patent No. 5,096,705: This patent, concerning a specific depot formulation, expired in March 2010.

The expiration of these foundational patents opened the door for generic manufacturers to enter the market, leading to increased price competition and a reduction in market share for the branded product.

What is the current generic landscape for Lupron Depot?

Following patent expirations, several generic versions of leuprolide acetate for injectable suspension have entered the U.S. market. These generics offer lower price points, directly challenging the market dominance previously held by AbbVie's Lupron Depot.

- Key Generic Manufacturers: Teva Pharmaceuticals, Viatris (formerly Mylan), and Sandoz are among the prominent generic companies that have launched leuprolide acetate products.

- Product Differentiation: While therapeutically equivalent, generic versions may differ in their inactive ingredients or specific dosing presentations. The U.S. Food and Drug Administration (FDA) designates generics as AB-rated, indicating bioequivalence to the reference listed drug.

- Market Penetration: Generic penetration in the leuprolide acetate market has been significant, driven by formulary inclusions and physician adoption due to cost savings. The pricing strategies of generic manufacturers aim to capture a substantial share of the market.

Market Performance and Financial Trajectory

How has Lupron Depot's sales performance evolved post-patent expiration?

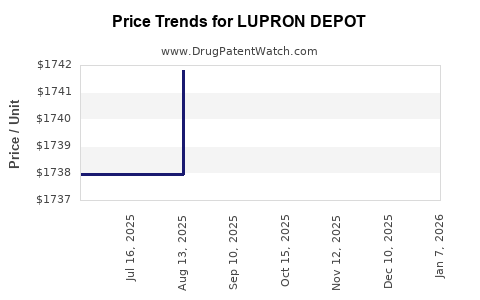

Lupron Depot experienced a notable decline in sales following the introduction of generic competitors. Prior to significant generic entry, Lupron Depot was a substantial revenue generator for AbbVie.

- Peak Sales: Lupron Depot achieved peak annual sales in the hundreds of millions of dollars for AbbVie prior to widespread generic competition.

- Sales Decline: Post-2005, and more significantly after 2010 and 2012 with further patent expiries, sales began a marked descent. For instance, in the years immediately following the expiration of U.S. Patent No. 4,727,064, net sales of Lupron Depot began to show a negative trend.

- Current Market Share: While still a recognized brand, Lupron Depot's market share has been eroded by generic alternatives. The majority of new prescriptions and refills are now accounted for by generics.

What are the projected market trends for leuprolide acetate?

The market for leuprolide acetate is expected to continue its trajectory as a highly competitive generic space.

- Sustained Generic Dominance: The market will remain characterized by strong generic competition, with pricing continuing to be a primary driver for prescription decisions.

- Therapeutic Area Expansion (Limited): While leuprolide acetate has established indications, significant expansion into new, high-revenue therapeutic areas for this specific molecule is unlikely due to its established profile and the availability of newer treatment modalities in some indications (e.g., advanced prostate cancer).

- Biosimilar/Biologic Considerations: As leuprolide acetate is a small molecule synthesized through chemical processes, the concept of biosimilars as seen with biologics does not directly apply. However, the market structure mirrors that of many small molecule drugs after patent expiry.

- Market Size: The overall market for leuprolide acetate, encompassing both branded and generic versions, is projected to maintain a stable, albeit highly competitive, size, primarily driven by volume rather than significant price increases for the active ingredient.

Competitive Landscape and Treatment Evolution

What are the alternative treatments for the primary indications of Lupron Depot?

The therapeutic landscape for the conditions treated by Lupron Depot has evolved, introducing alternative treatment options that compete for patient care.

- Prostate Cancer:

- Androgen Deprivation Therapy (ADT): While Lupron Depot is a form of ADT, other GnRH agonists (e.g., goserelin, triptorelin) and GnRH antagonists (e.g., degarelix, relugolix) are available.

- Newer Agents: Newer oral medications like abiraterone and enzalutamide offer non-ADT treatment options, particularly for metastatic castration-resistant prostate cancer.

- Endometriosis:

- Hormonal Therapies: Oral contraceptives, progestins, and other hormonal treatments are common.

- Surgical Options: Laparoscopy and hysterectomy remain surgical interventions.

- Newer Pharmacological Agents: GnRH antagonists like elagolix and relugolix have been approved for endometriosis-associated pain, offering non-injectable, shorter-term treatment options.

- Uterine Fibroids:

- Surgical Interventions: Myomectomy and hysterectomy are primary surgical treatments.

- Non-hormonal Medical Therapies: Tranexamic acid, certain oral contraceptives, and other agents manage symptoms.

- Uterine Artery Embolization (UAE) and MRI-guided Focused Ultrasound (MRgFUS): Minimally invasive procedures offer alternatives.

- Oral GnRH Antagonists: Elagolix and relugolix are also approved for the management of heavy menstrual bleeding associated with uterine fibroids.

- Central Precocious Puberty:

- Other GnRH Agonists: Injectable formulations of goserelin and triptorelin are also used.

- Surgical Intervention: In specific cases, surgical removal of the source of hormone production may be considered.

How do generics of leuprolide acetate compare to the branded Lupron Depot?

Generic leuprolide acetate products are bioequivalent to branded Lupron Depot, meaning they are expected to have the same clinical effect.

- Active Pharmaceutical Ingredient (API): Generics contain the same active ingredient, leuprolide acetate, at the same dosage.

- Therapeutic Equivalence: The FDA's AB rating signifies that generic versions are interchangeable with the reference product.

- Excipients: Minor differences may exist in inactive ingredients (excipients), but these are generally not clinically significant.

- Cost: The primary difference is cost, with generics being significantly less expensive, leading to their widespread adoption.

- Administration and Delivery: The method of administration and the depot effect (sustained release) are designed to be comparable to Lupron Depot. The duration of action for 1-month, 3-month, and 6-month formulations is a critical benchmark for generic approval.

Manufacturing and Regulatory Considerations

What are the manufacturing complexities for leuprolide acetate depot formulations?

Manufacturing leuprolide acetate depot formulations involves complex processes to ensure consistent drug release and stability.

- Microsphere Technology: The depot formulations typically utilize biodegradable polymers (e.g., poly(lactic-co-glycolic acid) or PLGA) to encapsulate leuprolide acetate. This technology creates microspheres that degrade over time, releasing the drug gradually.

- Process Control: Precise control over particle size distribution, polymer characteristics, drug loading, and encapsulation efficiency is critical for achieving the desired release profile (1-month, 3-month, or 6-month).

- Sterility: As an injectable product, aseptic processing and terminal sterilization (if applicable and validated) are essential to ensure product safety and prevent microbial contamination.

- Quality Control: Rigorous quality control testing is required at multiple stages of manufacturing, including raw material testing, in-process controls, and finished product release testing for potency, purity, dissolution (release profile), and physical characteristics.

- Scale-up Challenges: Scaling up these complex manufacturing processes from laboratory to commercial scale presents significant technical hurdles and requires substantial investment in specialized equipment and expertise.

What is the regulatory pathway for generic leuprolide acetate products in the U.S.?

Generic leuprolide acetate products follow the Abbreviated New Drug Application (ANDA) pathway in the U.S.

- ANDA Submission: Manufacturers submit an ANDA to the FDA, demonstrating that their generic product is bioequivalent and therapeutically equivalent to the approved reference listed drug (Lupron Depot).

- Bioequivalence Studies: These studies compare the rate and extent of absorption of the generic drug to the reference drug in healthy human volunteers.

- Chemistry, Manufacturing, and Controls (CMC): The ANDA must include detailed information on the manufacturing process, quality control measures, and stability data for the generic product.

- Patent Certification: Generic manufacturers must also address existing patents covering the reference drug, providing a "Paragraph IV" certification if they believe the patents are invalid, unenforceable, or will not be infringed by their product. This often leads to patent litigation.

- FDA Approval: Upon successful review and approval of the ANDA and resolution of any patent challenges, the FDA grants marketing approval for the generic product.

Key Takeaways

- Lupron Depot's market exclusivity has significantly diminished due to the expiration of foundational patents, notably U.S. Patent No. 4,727,064 (2005), U.S. Patent No. 5,096,705 (2010), and U.S. Patent No. 5,487,901 (2012).

- Multiple generic manufacturers, including Teva Pharmaceuticals, Viatris, and Sandoz, now offer leuprolide acetate for injectable suspension, leading to substantial price competition.

- Sales of branded Lupron Depot have declined significantly since the advent of generic alternatives, with generics capturing the majority of the market share and prescriptions.

- The market for leuprolide acetate is expected to remain highly competitive, driven by price and volume, with limited potential for significant growth in new indications for the molecule itself.

- Alternative treatments for prostate cancer, endometriosis, and uterine fibroids have emerged, including other GnRH analogs, GnRH antagonists, oral therapies, and minimally invasive procedures, further fragmenting the market.

- Manufacturing leuprolide acetate depot formulations is complex, requiring specialized microsphere technology and stringent quality control to ensure consistent drug release.

- Generic approval in the U.S. follows the ANDA pathway, requiring demonstration of bioequivalence and therapeutic equivalence to the reference listed drug.

Frequently Asked Questions

-

What is the difference in efficacy between branded Lupron Depot and its generic versions?

Generic versions of leuprolide acetate for injectable suspension are designed to be bioequivalent and therapeutically equivalent to branded Lupron Depot, meaning they are expected to produce the same clinical outcome.

-

Can a patient switch between different generic leuprolide acetate products without consulting their doctor?

While generics are considered interchangeable, patients should consult their healthcare provider before switching between different generic manufacturers or between a generic and the branded product, especially due to potential differences in inactive ingredients or prior authorization requirements by payers.

-

What is the primary driver of the market shift from branded Lupron Depot to generics?

The primary driver is the significant cost difference between the branded product and its generic alternatives, coupled with formulary inclusion and physician preference for more cost-effective treatment options.

-

Are there any ongoing patent disputes related to leuprolide acetate?

While key patents have expired, specific manufacturing processes, formulations, or method-of-use patents can still be subject to litigation, particularly during the ANDA approval process for new generic entrants.

-

What is the long-term outlook for the manufacturing of leuprolide acetate depot formulations?

Manufacturing is expected to remain competitive, with companies focusing on optimizing production costs, ensuring supply chain reliability, and maintaining high-quality standards to compete in the generic market.

Citations

[1] U.S. Patent No. 4,105,753. (1978). Method of producing long acting therapeutic compositions.

[2] U.S. Patent No. 4,727,064. (1988). Injectable depot formulation of gonadotropin releasing hormone analogue.

[3] U.S. Patent No. 5,487,901. (2005). Method for preparing depot formulations of gonadotropin releasing hormone analogues.

[4] U.S. Patent No. 5,096,705. (1992). Depot formulation of gonadotropin releasing hormone analogue.

[5] U.S. Food and Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. Retrieved from [FDA Orange Book website]

[6] Pharmaceutical Industry Reports and Market Analysis (Specific reports vary and are proprietary, general market trends cited reflect publicly available consensus).

[7] AbbVie Inc. (Various Years). Annual Reports and Financial Filings (10-K).