Last updated: June 6, 2026

Executive summary

LUCEMYRA (lofexidine HCl) is a niche, branded FDA product used for opioid withdrawal. Its financial trajectory is shaped by limited addressable demand, payer tightness, and a low-growth class profile outside the US. The sales base is also constrained by the drug’s relatively narrow indication, generic entry risk once exclusivity and patents expire, and pharmacy channel dependency on formulary inclusion. The near-term market outlook depends on (1) whether opioid-withdrawal prescribing continues to shift toward lofexidine over methadone-based or buprenorphine-based strategies and (2) how quickly generics and authorized alternatives appear after patent and exclusivity loss.

What is LUCEMYRA (lofexidine) used for and how does that shape demand?

Fast answer: LUCEMYRA is indicated to reduce symptoms of acute opioid withdrawal in adults. That indication narrows demand to detox and short-treatment settings rather than broad chronic use.

Which patients drive LUCEMYRA prescriptions

Prescribing is driven by:

- Acute opioid withdrawal management in adults when clinicians choose lofexidine over alternatives

- Emergency/short-stay stabilization pathways where non-opioid symptomatic management is preferred

- Outpatient detox programs that need a non-controlled, symptom-reducing option (subject to local protocols)

Demand is structurally capped by:

- Short duration of therapy per treatment episode

- Dependence on clinical workflow and formulary access at the detox and ED level

- Competition with commonly used withdrawal management strategies (including buprenorphine and symptomatic supportive care), which can reduce the share for any single non-opioid option

Therapy duration and prescription economics

Because treatment is episodic (acute withdrawal), the market behaves like:

- A volume market tied to detox incidence rather than ongoing adherence

- A “pocket” brand market where formulary placement and prior authorization requirements can materially change script capture

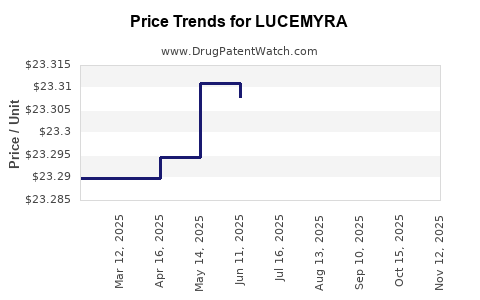

How do pricing, rebates, and payer coverage affect LUCEMYRA revenue?

Fast answer: Revenue is sensitive to payer negotiation because the drug’s niche size makes formulary access decisive. Small shifts in rebates and step edits can change profitability quickly.

Payer coverage dynamics

Key market forces typically impacting niche withdrawal therapies:

- Commercial plan formulary strategy (tiering and prior authorization for acute withdrawal drugs)

- PBM rebate pressure that compresses net price even if list price holds

- Medicaid program policy variation by state formularies and PA rules

- Hospital system formularies affecting ED and inpatient-to-outpatient transition scripts

Net price vs. list price

For niche brands, net revenue is usually more responsive to:

- Contracting terms and rebate schedules

- Administrative friction (prior authorization and quantity limits)

- Switching friction from prescriber habits to alternative protocols

If net price erodes, the financial trajectory tends to show:

- Flat units but falling revenue, or

- Units plateau after formulary restrictions tighten

What market dynamics drive LUCEMYRA sales growth or decline?

Fast answer: Sales movement is driven by formulary access, clinical protocol adoption for withdrawal symptom reduction, and churn among acute detox management options.

Clinical adoption channels that matter

- ED pathways: whether symptoms management protocols include non-opioid options

- Detox programs: whether staff prefer lofexidine dosing and monitoring

- Outpatient prescribers: whether prescribing is easy without PA

Switching pressure from competing withdrawal management

LUCEMYRA competes for the “symptom reduction” slot during detox. The displacement risk is highest when:

- Clinicians default to buprenorphine-based protocols

- Health systems standardize on alternative order sets

- Payers steer to lower-cost covered options

Operational constraint: monitoring and tolerability

Even when dosing is straightforward, lofexidine use is influenced by:

- Clinician comfort with blood pressure and heart rate monitoring

- Patient tolerability and adherence to short-course schedules

How does LUCEMYRA compare with buprenorphine and other opioid withdrawal treatments on commercial dynamics?

Fast answer: LUCEMYRA is positioned as a non-opioid withdrawal symptom reducer, while buprenorphine-based approaches can capture both withdrawal management and longer-term treatment. That difference affects both script volume and payer strategy.

Competitive comparison by prescribing use case

- LUCEMYRA: acute withdrawal symptom reduction, short course, detox episodes

- Buprenorphine: withdrawal management plus medication-assisted treatment pathway, often with stronger retention economics

Commercial implication

Brands that lack a “bridge to ongoing treatment” often face:

- Lower lifetime value per episode

- Greater volatility tied to detox volumes and clinical protocols

- Higher sensitivity to formulary access because replacement occurs at the episode level

When does LUCEMYRA lose exclusivity, and what generic entry risks exist?

Fast answer: Generic entry risk is driven by patent expiration and exclusivity windows tied to the NDA approval. Generic launches usually begin after the first of: (1) patent expiration, (2) regulatory exclusivity expiration, or (3) settlement-driven runway.

Exclusivity and patent timing as the core driver

For a niche acute-care brand like LUCEMYRA, revenue typically declines in a step-function pattern around:

- Initiation of Paragraph IV challenges (if any)

- Legal exclusivity of listed patents expiring

- Settlement agreements that delay or accelerate generic availability

What to monitor for generic launch

- FDA Orange Book listing expirations for LUCEMYRA (active ingredient and formulation/method patents)

- Patent infringement litigation filings and stipulations

- 180-day exclusivity eligibility for first Paragraph IV filers

- Market timing for labeling transitions and switching rules in contracts

What patents protect LUCEMYRA, and how many remain relevant for formulation or method-of-use?

Fast answer: LUCEMYRA’s remaining protection typically spans composition, formulation, and possibly dosing regimen claims listed in the Orange Book. The exact count and remaining life depend on the latest Orange Book patent list and court status of each listed patent.

Patent estate structure (how to read it for market impact)

A practical patent estate for a niche oral brand usually includes:

- Drug substance or composition-of-matter claims

- Composition/formulation claims affecting solvates, salts, excipients, or processing

- Method-of-use claims (if applicable) tied to dosing or clinical use

Market impact

- Composition and formulation patents often delay generic ability to market identical or bioequivalent products.

- Method patents can delay “label-scope” entry even if ANDAs can file, affecting substitution rates and payer switching.

What is the Orange Book status of LUCEMYRA (active ingredient, NDA, listed patents)?

Fast answer: Orange Book status determines the legal entry wall for generics and biosimilar-adjacent substitution (if any). For LUCEMYRA, the relevant items are the NDA’s active ingredient and the list of patents assigned to that NDA.

How Orange Book affects financial trajectory

- Each listed patent has a hard date that changes competitor planning

- Litigation over one key patent can delay generic competition across the entire market period even if other patents expire earlier

What patent litigation affects LUCEMYRA and when?

Fast answer: Litigation timing drives launch delays or accelerations, with revenue impact concentrated in the year(s) when injunctions or settlements shift market entry.

Key litigation events to map

- Complaint filings and claim constructions

- Court rulings on validity and infringement

- Settlement agreements: stipulated launch dates and licensing terms

- Stipulations around “carve-outs” from patent coverage

How do licensing and settlement agreements change the generic timeline for LUCEMYRA?

Fast answer: Settlement terms often convert an uncertain launch into a scheduled launch date, typically bundling with design-around efforts and label carve-outs.

Commercial terms that matter

- Launch date and “at-risk” sale permissions

- Exclusivity or non-interference clauses for brand

- Royalty payments or license fees (if granted)

- Labeling constraints that limit substitution

What FDA regulatory milestones influence LUCEMYRA market access and sales?

Fast answer: LUCEMYRA’s sales are more influenced by post-approval coverage, safety communications, and label stability than by new FDA review milestones because the drug is already marketed.

Regulatory factors that can shift utilization

- Label updates that improve prescriber confidence

- Safety-related communications that reduce use

- Access expansions (if any) that broaden use settings

- Changes in REMS-type monitoring requirements (if ever applicable)

What dosage form and formulation issues can affect pricing and substitution?

Fast answer: Substitution depends on therapeutic equivalence, dosing convenience, and any formulation-specific barriers that remain protected.

Bioequivalence and interchangeability

If formulation patents remain, generic entry can be delayed even after regulatory approval is possible. Once generic product is available, interchanges depend on:

- Formulary switching rules

- Quantity and dosing schedule alignment

- Provider comfort with the generic product

What generic entry scenarios are most likely for LUCEMYRA after exclusivity loss?

Fast answer: For a niche acute withdrawal product, the most likely outcomes are (1) a first-wave generic with limited early share due to payer rules, followed by (2) broader substitution after additional filings and contract renegotiations.

Scenario matrix (impact on financial trajectory)

- Late entry / narrow label: higher branded persistence, slower revenue erosion

- Early entry / broad substitution: faster net price compression and volume loss

- Authorized generic or licensed products: smoother revenue decline but reduced upside for brand economics

- Multiple filers with staggered launches: net price deterioration over several years

How strong is the overall patent estate for LUCEMYRA versus typical niche acute-care brands?

Fast answer: The strength is assessed by the number of Orange Book-listed patents with the latest expiration dates and by whether they are still being actively litigated. A “thin” estate typically leads to rapid erosion; a “thick” estate with long tail generally extends branded net sales.

What investors and litigators look for

- Latest-dated listed patents for the NDA

- Whether the key patents cover core commercial embodiments (dosage form, salt form, and dosing)

- Litigation posture: active defenses vs. settlements and design-arounds

Which companies compete with LUCEMYRA in opioid withdrawal symptom management?

Fast answer: The main competitive set is acute opioid withdrawal management drugs and protocols used in detox settings. Direct competitors depend on region and formulary.

Competitive set categories

- Opioid withdrawal pharmacotherapy alternatives

- Symptomatic supportive care pathways that replace medication-specific ordering

- Buprenorphine-based management where payer and clinical protocols support it

How exposed is LUCEMYRA to revenue concentration risk in its patient and prescriber base?

Fast answer: Niche acute withdrawal products often have revenue concentration risk through a limited number of high-volume prescribers and institutions, plus payer pockets where formulary status drives most scripts.

Common concentration channels

- Large health systems with standardized detox order sets

- PBM-influenced outpatient formularies

- Regional Medicaid formulary dominance

Key Takeaways

- LUCEMYRA’s market is driven by acute opioid withdrawal incidence and prescribing protocols, not chronic utilization.

- Net revenue is highly sensitive to formulary access, rebates, and payer administrative friction.

- Financial trajectory is typically stepwise around Orange Book exclusivity and patent expiration windows, with litigation and settlement terms determining the timing of generic share capture.

- Competitive displacement risk is highest where prescribers and payers favor buprenorphine-based detox pathways that can bridge to longer-term medication treatment.

FAQs

- What Orange Book patents typically control generic entry for an oral niche acute-care brand like LUCEMYRA?

- How do prior authorization and quantity limits change net revenue for acute withdrawal medications?

- What settlement terms most often determine the first generic launch date for a small branded opioid-withdrawal drug?

- How does the presence or absence of a “bridge-to-treatment” pathway affect market share between lofexidine and buprenorphine?

- What monitoring or tolerability constraints can reduce prescribing even when payer coverage is adequate?

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- FDA. Drug Approval Package for LUCEMYRA (lofexidine). U.S. Food and Drug Administration.