Last updated: April 25, 2026

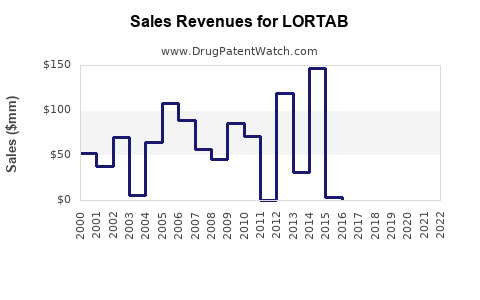

Lortab (hydrocodone bitartrate and acetaminophen) is a legacy, high-volume opioid analgesic whose market trajectory is dominated by (1) opioid-safety regulation and insurer controls, (2) aggressive product labeling and REMS-driven prescribing behavior, (3) payer step edits and limits driven by controlled-substance monitoring, and (4) erosion from newer abuse-deterrent and reformulated opioid options plus generic competition. Financial trajectory in the US has tracked the broader opioid “volume down” cycle: a peak-era rebound from generic expansion and multi-source availability, followed by sustained downtrend pressure as access tightened and litigation and compliance costs rose for manufacturers and distributors.

What is the market structure for Lortab?

Product role and competitive set

Lortab is an immediate-release (IR) combination opioid analgesic. Its competitive set is not limited to other hydrocodone combinations; it includes other IR opioids and combination analgesics that compete for the same chronic pain and acute pain prescribing lanes.

Key structure elements that shape pricing power:

- Multi-source generic presence: Lortab’s active ingredients are widely available through ANDA products and therapeutically equivalent alternatives.

- Class-level demand sensitivity: IR opioid demand responds strongly to regulatory scrutiny, guideline shifts, payer restrictions, and patient-monitoring requirements.

- Substitution across schedules: Even within Schedule II opioid analgesics, prescribers and payers switch among agents based on coverage rules, prior authorization criteria, and safety claims.

Pricing and contracting mechanics (US)

Lortab’s observable market economics are typically driven by:

- Wholesale and pharmacy acquisition costs tied to generic basket pricing.

- PBM fee schedules and formulary tier placement that reduce net prices when utilization rises or when coverage tightens.

- Contracting controls for controlled substances that can lower net revenue versus list price even if units remain stable.

How do regulation and safety controls shape Lortab demand?

Controlled-substance compliance and prescribing friction

Hydrocodone combination products operate in a highly monitored compliance environment. Prescription and dispensing are affected by:

- State prescription drug monitoring programs (PDMPs) that increase prescriber and pharmacist diligence.

- Limitations on early refills and quantity controls used by payers and health systems.

- Prior authorization and step edits for chronic pain regimens, especially where IR opioids are restricted without documentation.

Labeling and risk management

Risk content and opioid prescribing rules reduce volume for IR combinations over time by changing prescriber behavior and patient eligibility. In practical terms, safety communications and enforcement discourage long-duration IR prescribing, which compresses recoverable demand for legacy IR formats.

Litigation and manufacturer cost gravity

The US opioid litigation era increased compliance and legal costs across the supply chain and reduced risk tolerance for sustaining brand-like unit economics in mature, multi-source categories. Even where branded revenue is limited (given generic dominance), the class-level exposure reduces willingness to invest in marketing and distribution intensity and can pressure pricing strategies.

What demand indicators typically move Lortab’s sales?

For a legacy IR combination opioid like Lortab, unit demand and net revenue typically respond to these drivers:

- Formulary access: tier placement and PA requirements for hydrocodone combinations.

- Guideline adherence: shifts from opioids toward non-opioid and multimodal pain strategies reduce conversion rates from non-opioid therapy.

- Utilization limits: quantity caps for early refills and limits for dose escalation.

- Substitution effects: uptake of alternative hydrocodone products, other IR opioids, and reformulated options with different safety positioning.

- Market competition dynamics: generic price compression when new ANDA launches or when inventory is liquidated.

How has generic competition affected Lortab’s financial trajectory?

Loss of brand pricing power

Lortab is a legacy product whose economics are structurally constrained by:

- Generic availability that drives net price declines as competitive entrants increase.

- Manufacturer-level promotional dilution when PBMs and plans treat equivalents as interchangeable.

Channel dynamics

Controlled-substance channel tightening can reduce realized revenue even as retail demand remains. Net price compression comes from:

- Contracting rebates and fees tied to preferred status,

- Frequent formulary reevaluation cycles, and

- Increased monitoring and pharmacy compliance costs that shift economics downward.

What is the likely pricing and margin profile over the lifecycle?

Lifecycle pattern for legacy IR opioid combinations

Lortab’s financial profile over time is consistent with a standard mature generic-to-class regulation arc:

- Early/mid maturity: units remain robust; pricing stays higher than lowest generic levels.

- Mature phase: price compression accelerates as more competitors enter and as payer controls tighten.

- Late phase: volume declines or stagnates while net prices and margins fall due to continued formulary restrictions and opioid stewardship.

Net revenue sensitivity

Lortab’s revenue and profitability are most sensitive to:

- Net price per dose unit after PBM contracting and generic competition.

- Dispensing volume under payer controls and insurer opioid policies.

- Inventory and wholesaler channel fill cycles that can distort short-term sales vs long-term demand.

What financial trajectory should investors expect for Lortab-style products?

Baseline trajectory

The expected trajectory for hydrocodone/acetaminophen IR combinations in the US market is:

- Unit pressure from policy and prescribing restrictions.

- Downward net pricing from ongoing generic competition and utilization management.

- Higher compliance and transactional friction costs, reducing operating leverage in mature products.

Variance sources

Short-term deviations occur from:

- Contract wins or temporary formulary reinstatements,

- Supply disruptions that temporarily reduce availability, and

- Changes in state or payer opioid policies that affect dispensing volume.

How does substitution affect financial performance versus opioid alternatives?

Lortab’s substitution exposure is high because immediate-release hydrocodone/acetaminophen products are commonly compared against:

- Other opioid analgesic combinations (including alternative acetaminophen combinations),

- Single-entity opioids used under different dosing protocols, and

- Reformulated or abuse-deterrent opioids where safety claims influence payer and prescriber choices.

When payers tighten IR opioid access, Lortab-like products lose share to alternatives that match coverage rules better, even if those alternatives are also opioids, because coverage is often agent-specific.

What market events most often shift performance for Lortab?

High-impact catalysts

For Lortab and similar products, performance tends to shift during:

- Formulary updates driven by PBM and payer opioid management programs.

- Policy changes in PDMP enforcement or state prescribing limitations.

- Labeling updates that change prescriber comfort for specific dosing durations.

- Generic entry waves that intensify pricing pressure in the therapeutic equivalent segment.

What does the competitive landscape imply for Lortab’s future?

Near-term (12-24 months)

- Continued pressure from formulary and PA structures aimed at IR opioid use management.

- Sustained generic pricing compression.

- Ongoing substitution toward alternatives with coverage advantages.

Medium-term (3-5 years)

- Expected category shrinkage in IR opioid combination volume as opioid stewardship becomes more ingrained.

- Continued price pressure as mature generics compete on net realized prices.

- Increasing concentration risk if fewer manufacturers remain active at competitive net prices.

How should Lortab be interpreted in an investment or R&D portfolio?

Portfolio implication: low-to-moderate growth, higher risk-adjusted complexity

As a mature hydrocodone/acetaminophen IR product with high generic substitutability, Lortab-like assets typically deliver:

- Limited upside from differentiation,

- Revenue volatility tied to policy,

- Higher operational exposure to compliance and litigation overhang at the class level.

R&D implication: the bar shifts to safety and access differentiators

When access narrows and IR combinations face utilization limits, the development bar moves toward:

- Abuse-deterrent technologies,

- Non-opioid or opioid-sparing strategies,

- Payer-usable endpoints and real-world safety evidence.

Key Takeaways

- Lortab’s market dynamics are dominated by opioid-safety regulation, payer utilization management, and generics-driven net price compression.

- Financial trajectory is consistent with a mature, multi-source IR opioid: units face sustained policy pressure while net revenue declines under contracting and substitution.

- The primary levers shaping performance are formulary access, PDMP-driven prescribing friction, and agent-level substitution toward products favored by payer rules.

FAQs

1) Is Lortab primarily a brand or generic-driven market today?

It is primarily a multi-source generic market in practice because therapeutically equivalent hydrocodone/acetaminophen products are widely available.

2) What most directly affects Lortab net revenue versus list price?

PBM contracting (rebates/fees), formulary tier placement, and utilization management that reduce net realized pricing per unit.

3) Why does “opioid regulation” translate into sales changes for Lortab?

Regulatory and payer controls increase prescribing friction, restrict quantities, and reduce chronic IR opioid use, which lowers eligible patient volume.

4) Does Lortab compete mainly with other hydrocodone products?

No. It competes with a broader IR opioid and analgesic set for pain indications, with payer coverage often determining which agents capture share.

5) What is the most likely medium-term market outcome?

Category shrinkage or stagnation for IR opioid combinations, with continued net price pressure and share displacement to better-covered alternatives.

References

[1] FDA. “Drug Safety and Availability.” U.S. Food and Drug Administration. https://www.fda.gov/drugs/drug-safety-and-availability

[2] FDA. “Opioid Analgesic Risk Evaluation and Mitigation Strategy (REMS).” U.S. Food and Drug Administration. https://www.fda.gov/drugs/postmarket-drug-safety-information-patients-and-providers/extended-release-and-long-acting-opioid-pain-medicine-rems

[3] Centers for Disease Control and Prevention (CDC). “CDC Guideline for Prescribing Opioids for Pain.” https://www.cdc.gov/opioids/guidelines/

[4] National Association of Boards of Pharmacy (NABP). “Prescription Drug Monitoring Programs (PDMP).” https://www.nabp.pharmacy/programs/pdmp/

[5] U.S. Department of Health and Human Services. “Opioid Crisis.” https://www.hhs.gov/opioids/