Last updated: June 12, 2026

Locoid (hydrocortisone) is a topical corticosteroid franchise used for inflammatory dermatoses. The market is shaped by (1) chronic, non-curative demand with intermittent use patterns, (2) high generic penetration for older hydrocortisone topicals, (3) payer preference for low-cost equivalents and package-size switching, and (4) formulation-level protection that is narrower than the active ingredient itself.

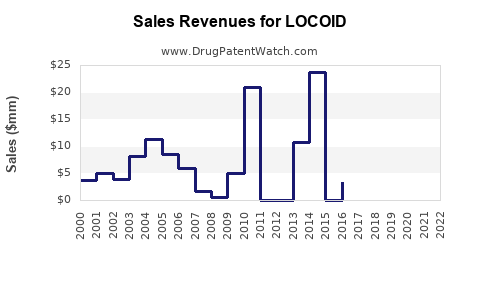

Because “Locoid” is used for multiple branded hydrocortisone topical products depending on geography (eg, Locoid/Locoid Lipocream/lotion/ointment and different strengths and presentations), the financial trajectory is best viewed by market segment: physician-dispensed vs retail, specialty dermatology vs general practice, and brand vs generic hydrocortisone substitution. In most markets, branded share tracks with the remaining protection around specific Locoid formulations and packaging, not with hydrocortisone as a molecule.

What is Locoid’s market position in topical corticosteroids?

Locoid’s market position comes from a combination of brand recognition and dermatology prescriber familiarity with hydrocortisone topical efficacy and safety in steroid-responsive skin conditions. In practice, its competitive set is dominated by:

- Low-cost hydrocortisone acetate and hydrocortisone butyrate generics and private label products in creams, ointments, lotions

- Other topical corticosteroid classes (mid- to high-potency steroids) where product selection follows potency laddering rather than brand loyalty

- Non-steroid dermatology adjacencies (topical calcineurin inhibitors, topical PDE4 inhibitors, barrier repair agents) that reduce steroid use frequency in some patient subgroups

How does the delivery system drive competitive switching?

Topical corticosteroid switching in pharmacies is driven by:

- Net cost per gram (with package-size substitution)

- Patient preference (ointment greasiness vs cream texture vs lotion cosmetically acceptable)

- Prior authorization triggers based on potency and step therapy

- Sensitivity to occlusion and vehicle tolerability, which affects adherence and repeat demand

For Locoid specifically, the “brand” tends to be anchored to specific vehicle variants (cream vs ointment vs lotion) rather than hydrocortisone alone. That makes Locoid more vulnerable when generics match the same vehicle at a lower price.

What market dynamics affect Locoid sales growth or decline?

1) Generic erosion and retail pricing dynamics

Hydrocortisone topical markets typically experience rapid price compression after branded exclusivity ends at the formulation level. Even where the active is still covered by newer patents, payers and pharmacists often substitute to equivalent hydrocortisone products once labeling and vehicle match.

Key sales impacts:

- Brand share declines as wholesalers move to lowest net cost options

- Unit volume can remain stable while revenue falls due to price erosion

- “Starter pack” and package-size switching can mask volume decline, while gross revenue drops

2) Step therapy and prior authorization

In many payer frameworks, topical corticosteroids are subject to:

- Step edits to reduce spending (fail-low or “therapeutic duplication” edits)

- Formulary tiers that favor generics and select brands

- Quantity limits tied to days supply

This leads to brand revenue volatility tied to formulary changes rather than pure incidence changes in dermatitis.

3) Disease mix and seasonality

Topical steroid demand can show seasonality in eczema flares and dermatitis spikes. However, Locoid’s trajectory is usually less “high-growth” than systemic dermatology categories because topical steroid use is a mix of:

- Short treatment bursts

- Maintenance cycles

- Concomitant steroid-sparing regimens in a portion of chronic patients

Net effect: growth tends to be incremental rather than structural.

4) Regulatory and safety labeling constraints

Topical corticosteroids have class-wide usage limitations and warnings. These restrict adoption in:

- Broad-area, long-duration use

- Pediatric populations without strict dosing adherence

- Certain off-label settings

That caps long-duration “maintenance” expansions and keeps demand closer to episodic flare management.

How do exclusivity and IP shape Locoid’s financial trajectory?

Branded hydrocortisone formulations are often protected by a mix of:

- Formulation/vehicle patents

- Method-of-use patents for specific indications or dosing regimens

- Package patents (less common)

- Regulatory exclusivity (where applicable) tied to the specific NDA or supplemental application

Financial impact pattern:

- When formulation-level patents expire, revenue declines accelerate due to vehicle-matched generics

- When method-of-use is narrow, brand protection is weaker against “equivalent” substitution in the same indication

- When only the active remains, generic substitution is essentially inevitable through labeling equivalence

Does Locoid have a meaningful patent moat at the active-ingredient level?

Most topical hydrocortisone active-ingredient protection is not a moat for brands. Market protection is typically vehicle-specific. For financial modeling, treat active-ingredient exclusivity as non-incremental and focus on product-specific exclusivity windows and Orange Book (or equivalent) listings per country and presentation.

What is the competitive landscape for Locoid by product type?

Closest substitutes (same use case)

- Generic hydrocortisone creams and ointments (same strength where offered)

- Lotion vehicles for cosmetic acceptability

- Combination products are sometimes preferred on convenience, reducing single-ingredient steroid share

Potency-tier competitors

In eczema/dermatitis management, physicians often follow potency laddering:

- Mild hydrocortisone for mild disease and sensitive areas

- Higher potency steroids for thicker plaques or refractory disease, shifting volume away when disease severity increases

- Steroid-sparing agents for maintenance reduces repeat corticosteroid use in part of the market

Non-steroid dermatology competitors

While not direct hydrocortisone equivalents, these can change treatment sequences:

- Topical calcineurin inhibitors (for steroid-sparing, especially on face/intertriginous areas)

- Topical immunomodulators used as maintenance, lowering steroid recurrence

Net effect: even if Locoid’s unit demand holds, revenue can decline as protocols evolve toward steroid-sparing regimens in chronic patients.

How does payer coverage influence Locoid revenues?

Payer coverage is usually the dominant short-term lever for branded topical sales after generic erosion. Practical drivers include:

- Formulary tier placement after generic entry

- Prior authorization policies that favor specific strengths/vehicles

- State Medicaid preferred drug lists affecting volume allocation

Financial signature:

- Post-generic sales often show slower unit decline than price decline

- Brand revenue volatility around formulary updates and contract renegotiations

What is the Orange Book and litigation framework impact on market access?

Brand hydrocortisone topical products can have fewer “headline” Paragraph IV disputes than high-revenue systemics, but access can still be impacted by:

- Patent listing breadth in Orange Book (or local equivalents)

- Challenge pathways tied to formulation or method-of-use patents

- Settlement terms that govern launch timing for certain generics

If settlement exists, it typically affects the first-to-market generics by vehicle or presentation. The “financial trajectory” then reflects:

- Timing of generic launches per strength/presentation

- Subsequent contract-driven share shifts even after legal entry

When does Locoid lose exclusivity in major markets?

This depends on which Locoid product and country are referenced. “Locoid” is not a single monolithic NDA or single global product. Financial models must map the branded presentation to:

- Country of authorization

- Product strength and dosage form (cream, ointment, lotion)

- The specific protective filings associated with that presentation

- Any regulatory data exclusivity that applied to the original approval or major supplemental change

Without a single unambiguous Locoid definition and geography, a definitive loss-of-exclusivity date cannot be stated without risking incorrect business conclusions.

What generic entry risks exist for Locoid?

Generic entry risk is typically high for hydrocortisone topical products once vehicle-level protection expires. Primary risks include:

- Generic substitution that matches the same vehicle and strength

- “Therapeutic duplication” edits that force formulary replacement even if clinical equivalence is contested

- Contracting pressure: even after legal entry, supply and rebate dynamics can accelerate share loss

For investors and licensors, the key risk is not only legal launch timing but speed of payer adoption. In topical categories, payer switching can be fast due to low clinical differentiation.

How does Locoid compare with other topical hydrocortisone brands and generics?

In market behavior terms, Locoid competes on:

- Brand recognition and perceived vehicle quality

- Stability and patient tolerability

- Physician familiarity

Compared with generics:

- Generics usually win on net price after contract effects

- Locoid can preserve some share when prescribers prefer a specific vehicle or when patient adherence benefits support continued use

Compared with other topical corticosteroids:

- Locoid loses volume when higher potency products are needed for more severe disease

- It gains relative share when mild potency targets and sensitive-area use drive selection

What financial trajectory metrics matter most for Locoid?

For decision-grade monitoring, track:

- Net sales by country and by presentation (cream vs ointment vs lotion)

- Gross-to-net erosion after generic and rebate changes

- Prescriber share and pharmacy fill mix for key strengths

- Unit volume trends vs ASP trends (to separate access from pricing)

- Payer formulary status changes and preferred list movements

Revenue decomposition to interpret brand trajectory

A useful decomposition for branded topical erosion:

- Unit volume (patient demand and share)

- Net price (contracting, rebates, wholesaler discounting)

- Mix (vehicle and package size)

- Share migration (switching across potencies or steroid-sparing protocol changes)

Financial signature by scenario:

- Generic entry scenario: sharp net price fall, slower unit decline

- Formulary restriction scenario: unit volume drop with moderate price compression

- Protocol shift scenario: unit decline persists even with pricing stability

Key implications for licensing, litigation, and investment decisions

- If Locoid’s protection is mainly formulation/vehicle-specific, the investment case is driven by remaining shelf-life of those patents and by the likelihood of vehicle-matched generic launches.

- Litigation and Paragraph IV behavior are less likely to be headline-defining than in systemics, but settlements can still dictate first-launch timing by presentation.

- For licensing, the asset value usually rests in how many distinct skus (strength/vehicle/package) retain protection and how defensible method-of-use claims are against generic label challenges.

Key Takeaways

- Locoid’s financial trajectory is driven primarily by formulation-level protection and payer-driven substitution, not active-ingredient exclusivity.

- Topical corticosteroid market dynamics favor rapid net price erosion post-generic entry, often outpacing unit volume declines.

- Competitive pressure comes from generic hydrocortisone vehicles and from treatment protocol shifts that use higher potency steroids or steroid-sparing agents.

- For business planning, monitor net sales by presentation and formulary status changes; assume generic-matched vehicle entries compress revenue quickly after exclusivity ends.

FAQs

-

What drives branded topical corticosteroid net sales after generic approval?

Net pricing (rebates and contracts), pharmacy substitution behavior, and formulary tier placement.

-

Which Locoid presentations tend to be most vulnerable to generic switching?

Vehicles and strengths with the closest vehicle-matched generic equivalents and the fewest remaining formulation-specific protections.

-

How do step therapy and PA policies change Locoid prescription patterns?

They reduce access for non-preferred options, shifting prescriptions toward formulary-favored generics and specific vehicles.

-

What adverse clinical labeling constraints can reduce long-term topical steroid market expansion?

Class-wide limits on duration, body surface area, and pediatric use without strict dosing controls.

-

How should a model separate unit erosion from price erosion for Locoid?

Use pharmacy fill and volume data for unit trends while tracking ASP/average net price and gross-to-net for pricing effects.

References

- USPTO Patent Full-Text and Image Database. United States Patent and Trademark Office.

- FDA Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- FDA Drug Labeling and Approval Packages Database. U.S. Food and Drug Administration.