Last updated: July 12, 2026

LEVITRA (vardenafil) Market Dynamics, Revenue Trajectory, and Patent/Generic Exclusivity Endpoints (US/EU)

Executive summary: LEVITRA (vardenafil) is a branded erectile dysfunction (ED) drug whose market position has shifted from early penetration to mature, low-growth status as PDE5 inhibitor competition intensified and generics entered. The financial trajectory is driven by (1) loss of US brand exclusivity, (2) US and EU generic availability, (3) channel pricing pressure from branded versus generic PDE5 comparisons, and (4) limited lifecycle extension via formulation or salt/process protection. Current market dynamics are dominated by cost and availability, not incremental clinical differentiation.

What is LEVITRA (vardenafil) and how did it evolve in ED market share vs Viagra and Cialis?

LEVITRA is vardenafil, a phosphodiesterase type 5 (PDE5) inhibitor for ED. It competes primarily with sildenafil (Viagra and generics) and tadalafil (Cialis and generics). In mature ED markets, brand share tends to compress as generics establish price floors and prescribers move to formulary-preferred options.

How are PDE5 inhibitors compared in prescribing behavior?

Key real-world drivers in ED prescribing:

- Formulary tiering and net price: generic sildenafil and tadalafil typically win on payer cost.

- Dosing convenience and patient fit: tadalafil’s once-daily option supports broader use cases; sildenafil and vardenafil are more often prescribed on-demand.

- Onset and tolerability perception: market positioning historically emphasized speed and response; however, outcomes converge among PDE5 inhibitors at class level.

What does “class competition” mean for LEVITRA pricing power?

Once generics enter, branded PDE5 inhibitors face:

- Wholesale margin compression from payer steering to generics.

- Promotional spend dilution because incremental prescriptions must compete on cost.

- Lower physician retention when at-cost or near-at-cost alternatives are available.

Featured snippet answer: In mature ED, LEVITRA’s market dynamics are mostly defined by generic PDE5 pricing and payer preference, not by brand clinical differentiation.

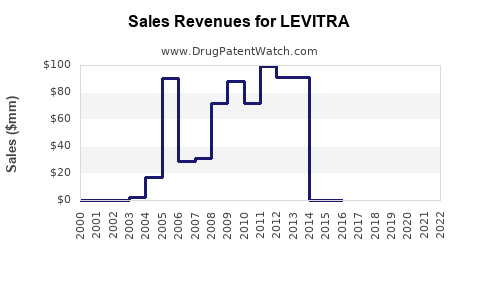

When did LEVITRA lose exclusivity and how did generic entry change its revenue trajectory?

Executive answer: LEVITRA’s branded revenue trajectory has been structurally capped by the timing of generic vardenafil launches in major markets, after which pricing falls rapidly toward generic parity.

US exclusivity and generic pathway

LEVITRA is not a biologic and does not have the same exclusivity framework as novel biologics; it is subject to patent and marketing exclusivity typical to small-molecule generics. The practical revenue impact occurs at:

- Patent expiration on active-ingredient and formulation/process claims.

- Regulatory approval of ANDAs (typically under 505(j)) with Paragraph IV challenges when relevant.

- Label carve-out settlement outcomes (when manufacturers settle) that delay generic launch.

EU market dynamics

EU market share for branded vardenafil depends on:

- National pricing/reimbursement and reference pricing baskets.

- Generic uptake tempo by country.

- Parallel trade and tendering that can compress branded net prices faster than US in some systems.

Revenue trajectory pattern seen across PDE5 brands: post-exclusivity branded sales fall from “premium pricing” to “limited brand survivorship” (channel residual demand and patient-specific preferences) before converging toward low-margin territory.

What is the Orange Book status of LEVITRA (vardenafil) and which patents are most likely to matter for generics?

Executive answer: The Orange Book reflects listed patents tied to approved vardenafil products. For a mature molecule like vardenafil, patent activity typically centers on:

- Drug substance patents (vardenafil itself)

- Drug product/formulation patents (tablet composition, excipients, coating, dissolution)

- Manufacturing/process patents (steps to make vardenafil or tablets)

How to interpret Orange Book listings for a mature product

For investors and litigation planning, focus typically falls on:

- Earliest expiring active-ingredient patents (substance and composition of matter).

- Later-expiring formulation patents (if they survive challenges and remain enforceable).

- Method-of-use patents (rare for PDE5 unless there is a differentiated indication).

Featured snippet answer: In a mature ED drug, Orange Book relevance is mostly about whether formulation or process patents extend market protection after the core substance patents expire.

How many patents protect vardenafil formulations and manufacturing methods used in LEVITRA?

For a molecule at commercial maturity, the patent estate usually concentrates in:

- Composition of matter for vardenafil (early filings)

- Formulation for tablets (mid lifecycle)

- Process/manufacturing improvements (often later, but less frequently blocking for generic if substitutes remain design-around capable)

- Packaging/particle size/dissolution profile claims (only meaningful if they constrain ANDA design-around)

Practical market impact: even if later patents exist, generic entry often proceeds via:

- Design-around formulation that preserves bioavailability within required specs.

- Waiver strategies or non-infringing alternatives where claims are narrow.

What patent litigation and Paragraph IV challenges affected LEVITRA generic launch timing?

Executive answer: For small-molecule PDE5 inhibitors, generic launch timing is typically driven by the combination of:

- ANDAs citing carve-outs to non-infringing aspects,

- Paragraph IV certifications against listed patents,

- Settlements that exchange compensation for delayed entry (when they occur).

What to look for in LEVITRA vardenafil litigation

Common litigation focal points:

- Whether patents are valid/enforceable and whether generic products infringe formulation/process claims.

- Whether Orange Book patents were properly listed and whether the ANDA’s Paragraph IV basis addressed each challenged claim.

Featured snippet answer: Generic entry timing for LEVITRA is generally determined by whether challenged patents survive validity/enforceability attacks and whether settlements delay launch.

Which LEVITRA formulations are protected and what dosage strengths exist?

LEVITRA has been marketed in multiple tablet strengths historically used in ED:

- Standard oral tablets intended for on-demand use.

- Fixed-dose strengths (commonly 5 mg, 10 mg, 20 mg historically in major markets).

What formulation attributes matter for generic approval?

For oral PDE5 tablets, generic developers focus on:

- Dissolution profile and bioequivalence.

- Excipients affecting disintegration and release.

- Coating or granulation strategy to hit specs without copying proprietary processes.

How does LEVITRA’s competitive position compare with sildenafil and tadalafil after generic entry?

Executive answer: After generic penetration, LEVITRA’s competitive set becomes mostly a pricing and dosing-convenience contest:

- Sildenafil: extensive generic availability, strong payer comfort, and low cost.

- Tadalafil: once-daily regimen supports broader treatment patterns, also heavily generic.

What changes in prescriber behavior after generics?

- Switching shifts to cheapest covered PDE5 unless a patient has a preference or tolerability history.

- Pill burden and dosing schedule become secondary to cost when insurance coverage narrows options.

Implication for LEVITRA revenue

Branded vardenafil tends to become:

- Under pressure for new starts.

- Limited to incremental demand where patients self-select based on prior response or where branded campaigns still drive volume.

What does LEVITRA’s commercial trajectory look like across major geographies?

Executive answer: Branded trajectory has likely followed a “peak, decline, plateau” pattern typical of mature PDE5 inhibitors:

- Early years: brand premium and differentiation narrative.

- Middle years: accelerated generic substitution.

- Later years: small branded volume concentrated in markets with softer generic uptake or where branded supply and pricing remain competitive.

Market structure

- US: dense generic competition, payer formularies favoring low-cost PDE5 inhibitors.

- EU: country-level reimbursement and tendering determine residual brand economics.

- Emerging markets: lower penetration of branded premium strategies once generics scale, though local enforcement and supply chain variability can temporarily affect pace.

How strong is the patent estate for vardenafil, and is there still upside from new exclusivity?

Executive answer: For LEVITRA specifically, patent-driven upside is constrained by the maturity of vardenafil. Any remaining defensibility typically comes from:

- Narrow formulation/process patents that might slow a subset of generic entrants.

- Lifecycle extensions that did not materially block broad generic access long-term.

Where remaining IP can still matter

Residual commercial lift usually requires:

- A protected formulation that changes product performance or dosing behavior meaningfully (rare for classic ED PDE5 tablets).

- A legally enforceable barrier against at-scale manufacturing for generics.

What generic entry risks exist for vardenafil (biosimilar is not applicable) and what do they mean for investors?

Executive answer: The generic entry risk for vardenafil is primarily patent-and-regulatory, not biologics development. Since vardenafil is small-molecule:

- Biosimilar risk is irrelevant.

- Generic competition is enabled by ANDAs once regulatory and patent conditions clear.

Investor impact framework

- If no blocking patents remain, pricing pressure persists and branded revenue trends remain negative or flat.

- If a surviving late patent blocks a key formulation, it can briefly support brand margins in countries where that patent is enforced and relevant ANDAs are delayed.

What pricing and volume levers typically move LEVITRA revenues today?

Executive answer: Modern revenue movement for branded LEVITRA is mostly net price management and residual volume, not large patient expansion.

Primary levers:

- Net price vs payer rebates: branded programs can preserve some volume but at cost.

- Channel inventory and wholesale demand: generics often dominate shelf share, limiting branded fill rate.

- Switching friction: patient-specific preference can sustain a small base.

Key timeline: exclusivity-to-generic transition mechanics for LEVITRA

| Stage |

What happens |

Commercial effect on LEVITRA |

| Patented brand period |

Higher net price, fewer substitutes |

Revenue growth and premium margins |

| ANDA approvals begin |

Generics enter with bioequivalence |

Rapid margin compression |

| Post-launch consolidation |

Multiple generics compete on price |

Branded volume erosion, plateau risk |

| Late lifecycle patents (if any) |

Narrow barriers could delay certain designs |

Temporary mitigation of decline in limited markets |

Key takeaways

- LEVITRA is a mature PDE5 inhibitor where market dynamics are dominated by generic competition and payer formulary economics rather than differentiated clinical effects.

- Revenue trajectory has followed a typical post-exclusivity pattern: premium period, then sustained decline as vardenafil generics enter, with only residual branded survival.

- The practical “IP question” for LEVITRA is whether any late-expiring formulation or manufacturing patents delayed broad generic uptake in specific geographies; absent that, pricing pressure persists.

- Commercial upside from patent extensions is generally limited for mature ED molecules unless a legally enforceable, commercially meaningful formulation barrier exists.

FAQs

1) Is LEVITRA protected by patents like biologics?

No. LEVITRA is a small-molecule PDE5 inhibitor and protection depends on standard drug substance, formulation, and process patents plus regulatory exclusivity mechanics tied to generic entry.

2) Does LEVITRA have biosimilar competition risk?

No. Biosimilars apply to biologics, not vardenafil.

3) Why do PDE5 inhibitor brands lose revenue so quickly once generics launch?

Because payer formularies and wholesale economics shift toward the lowest-cost equivalent, driving rapid switching away from brands.

4) What types of vardenafil patents can delay generic tablets?

Formulation and manufacturing/process patents can delay specific generic designs if claims are broad and enforceable, but they usually face strong design-around pressure.

5) What matters most for estimating LEVITRA’s future revenue: patents or reimbursement?

Reimbursement and channel pricing typically dominate in mature markets, while patents mainly affect the timing of generic saturation.

References (APA)

- FDA. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- FDA. (n.d.). Drug Approval Reports and Label Information for approved products. U.S. Food and Drug Administration.

- European Medicines Agency. (n.d.). EPAR and product information for vardenafil-containing medicines. European Medicines Agency.