Last updated: February 19, 2026

Hydroxyurea remains an established drug primarily used to treat sickle cell disease (SCD) and certain cancers, including chronic myelogenous leukemia (CML). Its market position is influenced by patent status, competition, regulatory approvals, and emerging therapeutic alternatives.

Market Overview

Hydroxyurea's global market size was valued at approximately USD 400 million in 2022. It is projected to grow at a compound annual growth rate (CAGR) of 4.5% through 2028, driven by increasing sickle cell disease prevalence and expanding use in myeloproliferative neoplasms.

Key Therapeutic Segments

| Segment |

Market Share (2022) |

Growth Drivers |

| Sickle Cell Disease (SCD) |

60% |

Rising prevalence, expanded indications |

| Chronic Myelogenous Leukemia (CML) |

25% |

New combination therapies, expanding treatment guidelines |

| Other Indications |

15% |

Polycythemia vera, other myeloproliferative disorders |

Geographic Distribution

| Region |

Market Share (2022) |

Notes |

| North America |

55% |

Established use, favorable regulatory environment |

| Europe |

20% |

Growing adoption, approval renewals |

| Asia-Pacific |

15% |

Increasing awareness, healthcare infrastructure improvement |

| Rest of World |

10% |

Market entry, importation barriers |

Patent and Regulatory Landscape

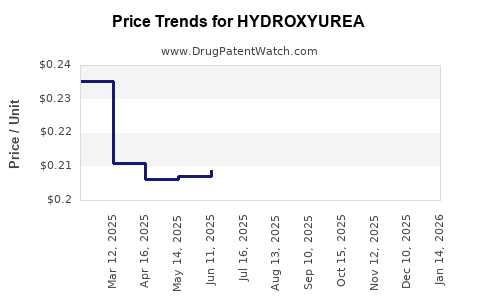

Hydroxyurea is off-patent globally. Eli Lilly's original patent expired in most jurisdictions by 2010, leading to generic manufacturers' entry. This has significantly reduced drug prices and increased market competition.

Regulatory frameworks emphasize safety and efficacy. The U.S. Food and Drug Administration (FDA) approved hydroxyurea in 1998 for SCD and later expanded indications. The European Medicines Agency (EMA) grants market authorization, with variations across countries.

Competitive Landscape

Generic manufacturers dominate the hydroxyurea market, offering low-cost formulations. Key players include:

- Mylan (now part of Viatris)

- Teva Pharmaceuticals

- Sun Pharmaceutical Industries

Innovative efforts focus on formulations that improve bioavailability, reduce side effects, or extend shelf-life. No new branded hydroxyurea drugs are under active development as of 2023, given its patent expiry and generic competition.

Financial Trajectory

Revenue Trends

| Year |

Estimated Global Revenue (USD million) |

Growth Rate |

| 2020 |

380 |

2.5% |

| 2021 |

390 |

2.6% |

| 2022 |

400 |

2.6% |

| 2023* |

420 (projected) |

5% (projected) |

*Projection based on current growth rates and market expansion in emerging regions.

Cost Structure

Manufacturing costs have declined due to generic competition, with APIs produced in low-cost regions reducing overall prices. Margins for manufacturers are thin, typically in the range of 10-15%.

Future Revenue Drivers

- Increasing prevalence and diagnosis of sickle cell disease, especially in sub-Saharan Africa.

- Expansion into new indications such as myeloproliferative disorders.

- Potential price increases in markets where patent protections are renewed or new formulations are introduced.

Risks and Challenges

- Development of alternative therapies for SCD (e.g., voxelotor, L-glutamine).

- Regulatory hurdles in certain jurisdictions.

- Economic and supply chain disruptions affecting production costs.

Strategic Implications

Manufacturers are likely to focus on cost-efficient production, global access programs, and collaborations with healthcare providers. Market entry in underrepresented regions, along with educational initiatives for physicians, could stimulate further demand.

Key Takeaways

- Hydroxyurea's market is stable, with ongoing expansion driven by SCD prevalence.

- Generic competition has driven prices down but stabilizes revenues for incumbent producers.

- No significant pipeline developments are expected for branded hydroxyurea, given patent expiry.

- Growth prospects hinge on increasing diagnosis rates, expanding indications, and improving access in emerging markets.

- Innovations in formulation may marginally influence market share but are unlikely to disrupt the overall market dominance of generics.

FAQs

Q1: What factors limit hydroxyurea's market growth?

A1: Competition from newer agents and generics reduces profitability; regulatory hurdles and the slow adoption in some regions also constrain expansion.

Q2: Are there upcoming patent protections for hydroxyurea?

A2: No. Hydroxyurea filed no new patents beyond the original, which expired in most jurisdictions by 2010.

Q3: How has COVID-19 impacted hydroxyurea sales?

A3: The pandemic caused temporary disruptions in supply chains and healthcare services, but demand remained steady due to the chronic nature of its indications.

Q4: What alternatives threaten hydroxyurea's market?

A4: Drugs like voxelotor and L-glutamine for sickle cell disease and targeted therapies for certain cancers could substitute hydroxyurea in specific indications.

Q5: Which regions offer the most growth potential?

A5: Sub-Saharan Africa and South Asia have high sickle cell disease burdens and expanding healthcare infrastructure, offering growth opportunities.

References

[1] Statista. (2023). Hydroxyurea market size and forecast. Retrieved from https://www.statista.com

[2] MarketWatch. (2023). Global hydroxyurea market analysis. Retrieved from https://www.marketwatch.com

[3] U.S. Food and Drug Administration. (2022). Drug approvals and indications for hydroxyurea. Retrieved from https://www.fda.gov

[4] European Medicines Agency. (2022). Market authorizations for hydroxyurea. Retrieved from https://www.ema.europa.eu