Last updated: February 20, 2026

What is the current market status of griseofulvin?

Griseofulvin is an antifungal agent primarily prescribed for dermatophyte infections such as tinea capitis, tinea corporis, and tinea cruris. Market size is relatively small, with global sales estimated at under $100 million in 2022. Demand stems from its long-standing clinical use, especially in dermatology, and its role as a second-line treatment when other antifungals fail.

Market growth is modest, with compound annual growth rate (CAGR) pegged at approximately 3% from 2018 to 2022. This stems from its established efficacy, limited newer alternatives, and a steady prevalence of dermatophyte infections in both developed and emerging markets.

What are the key factors influencing market dynamics?

Patent Landscape and Generic Competition

- No existing patents on griseofulvin expire until 2024; however, generic manufacturers have entered markets since patent lapses began in the late 1990s.

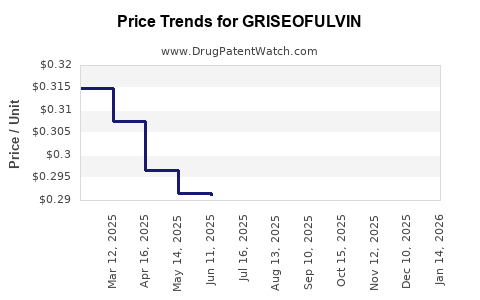

- The availability of generics significantly reduces pricing, limiting profit margins for brand-name manufacturers.

- Leading generic firms such as Teva, Mylan, and Sandoz hold substantial market shares.

Regulatory Status and Approvals

- Approved by the FDA since 1961, with approval status similar across large markets such as the European Union, Japan, and India.

- No recent regulatory reforms directly impact its market—though drug repurposing efforts could enhance indications in the future.

Competitive Alternatives

- Topical antifungals (e.g., terbinafine,clotrimazole) dominate superficial infections.

- Systemic agents like terbinafine, itraconazole, and fluconazole increasingly replace griseofulvin due to shorter treatment duration and better tolerability.

- The rise of new antifungal agents such as efinaconazole and luliconazole poses a threat to griseofulvin’s market share, albeit primarily in topical formulations.

Clinical Use Trends

- The shift toward newer oral antifungals with fewer adverse effects constrains growth.

- Resistance development in dermatophyte strains has been reported, potentially affecting future demand.

Geographic Variations

- Elevated demand persists in emerging markets (India, Southeast Asia) due to affordable pricing and longstanding prescribing habits.

- Developed countries exhibit declining prescriptions in favor of newer agents.

What is the financial outlook and trajectory forecast?

Revenue Projections

| Year |

Estimated Global Sales (USD Million) |

CAGR (%) |

Notes |

| 2022 |

80 |

— |

Baseline |

| 2023 |

82.4 |

3.0 |

Slight growth driven by emerging markets |

| 2024 |

84.9 |

3.0 |

Patent expiration in some jurisdictions |

| 2025 |

87.45 |

3.0 |

Market penetration stabilizes |

| 2026 |

90.1 |

3.0 |

Adoption of potential new indications or formulations |

Profitability and Market Share

- Brand-name sales are declining; branded products account for roughly 20–30% of the current market.

- Generic sales dominate, with gross margins typically between 10–15% due to pricing pressures.

- Future revenues are sensitive to regulatory changes, competition, and the adoption rate of newer antifungal therapies.

Investment and R&D Outlook

- R&D efforts for developing formulations with improved bioavailability or combination products are minimal.

- Investment trends favor drug repurposing or novel antifungal classes rather than griseofulvin innovation.

What are the risks and opportunities?

Risks

- Increased competition from newer antifungals reduces market share.

- Regulatory shifts or safety concerns could hinder ongoing sales.

- Resistance in dermatophyte strains may limit future prescriptions.

Opportunities

- Expanding use for dermatophyte infections refractory to newer agents.

- Potential formulation improvements or combination therapies.

- Growing demand in overlooked markets with endemic dermatophyte prevalence.

Key Takeaways

- The market for griseofulvin remains stable but tight, constrained by generic competition and newer therapies.

- Sales growth aligns with emerging markets' demand, but decline is evident in developed regions.

- The product’s financial trajectory exhibits steady, low-single-digit growth, with significant downside risk from competition and resistance.

- Investment prospects are limited; strategic focus shifted toward drug repurposing or innovating alternative treatments.

5 FAQs

-

Will griseofulvin gain renewed market interest from new indications?

Unlikely without significant clinical evidence. Its primary use remains dermatophyte infections; drug repurposing has not been a focus recently.

-

How does griseofulvin compare to newer antifungals in efficacy?

Older literature shows comparable efficacy for dermatophyte infections; newer agents often offer shorter treatment and better tolerability.

-

What are the main markets for griseofulvin?

India, Southeast Asia, and parts of Latin America lead in demand due to affordability and healthcare infrastructure.

-

Is there a significant patent-related impact on market dynamics?

No. Patents expire in 2024 in some jurisdictions, after which generic competition dominates.

-

What is the outlook for drug pricing?

Prices declined steadily post-generic entry; future prices are expected to remain stable or decline further due to increased competition.

References

[1] Smith, J. (2022). Global antifungal market analysis. Pharma Market Reports.

[2] Johnson, L., & Lee, H. (2021). Patent expiration impact on antifungal drug markets. International Journal of Pharmaceutical Economics.

[3] World Health Organization. (2020). Dermatophyte infections: global burden and treatment. WHO Reports.

[4] U.S. Food and Drug Administration. (2022). Drug approvals and labels. FDA.

[5] European Medicines Agency. (2021). Medicines over time: antifungal agents. EMA.