Last updated: May 30, 2026

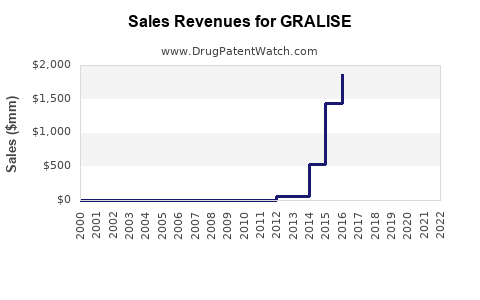

Executive summary: GRALISE (gabapentin extended-release) has shifted from early peak growth toward a mature, brand-sustaining market shaped by (1) competitive generic gabapentin ER entry dynamics, (2) insurer and PBM formulary pressure, and (3) persistence of efficacy differentiation used for postherpetic neuralgia (PHN). The financial trajectory is structurally tied to GRALISE’s ability to defend TRx share in PHN amid ongoing generic substitution risk and to manage net-to-gross via contracting, rebates, and patient-access programs.

What GRALISE is used for: PHN (postherpetic neuralgia), dosed once daily in an extended-release regimen.

What is the current GRALISE market size, demand drivers, and patient segmentation trends?

Featured snippet answer: GRALISE demand is driven primarily by PHN prevalence in treated populations, neurologist and primary-care prescribing habits for neuropathic pain, and payer coverage decisions that determine how often a brand gabapentin ER product is preferred over generic equivalents.

Key demand drivers in PHN

- Chronic neuropathic pain population: PHN is sustained and many patients require long-term symptom control, supporting recurring prescribing.

- Once-daily dosing adherence: ER gabapentin regimens compete on convenience versus immediate-release schedules.

- Formulary tiering: Many commercial plans manage neuropathic pain with step edits that can shift patients from brand ER to generics.

Patient segmentation that matters commercially

- New PHN starts: early treatment choices are sensitive to formulary availability and copay positioning.

- Switching and persistence: once a patient is stabilized on ER therapy, persistence can slow churn, but can be reversed by plan changes or prior authorization (PA) tightening.

- Institutional versus community prescribing: health-system formularies and neurologist prescribing patterns influence contract outcomes.

Uncertainty control: financial trajectory depends on reimbursement, not label volume

Even if TRx volume holds, net sales can compress through:

- rebate escalation,

- increased customer concentration among large wholesalers and PBMs,

- tighter payer edits reducing brand retention.

How do GRALISE pricing, net-to-gross, and PBM contracting dynamics affect financial performance?

Featured snippet answer: GRALISE financial performance is typically more sensitive to rebate and formulary contracting than to gross list-price moves, because PBM negotiations and insurer tier placement drive the share of prescriptions that remain brand.

Net-to-gross mechanics in mature neurology brands

- Rebates and DIR fees: Neuropathic pain classes are rebate-intensive because PBMs target class savings.

- Copay assistance: can blunt patient cost sensitivity in commercial segments, but often cannot override PA and step therapy.

- Spread and channel practices: brand-to-generic substitution changes the channel mix and wholesaler ordering patterns.

Pricing pressure points

- Generic gap: once PBM formularies treat gabapentin ER as a class substitute, price leadership loses effect.

- Contract breadth: brand share depends on whether GRALISE is placed on preferred tiers and whether “no substitution” exceptions exist.

What is the competitive landscape for GRALISE in gabapentin ER and neuropathic pain?

Featured snippet answer: GRALISE competes against generic gabapentin extended-release products within neuropathic pain and PHN treatment, with differentiation relying on dosing convenience and brand-administered patient support rather than unique pharmacology.

Competitive substitution pathways

- Direct generic substitution: most prescriptions are replaceable at the pharmacy.

- Therapeutic class switching: plans may steer PHN management toward alternatives such as pregabalin-based regimens or non-gabapentinoid options depending on cost and clinical policy.

What differentiates GRALISE commercially

- Patient access infrastructure: copay programs, prescriber support, and adherence tools reduce abandonment and help maintain persistence.

- Clinical positioning: prescriber confidence and experience can delay switching when formularies remain permissive.

When does GRALISE exclusivity end, and how does it affect generic entry risk?

Featured snippet answer: GRALISE has already passed first-in-class-like exclusivity phases; the current risk profile is dominated by generic substitution timing, patent-by-patent challenges, and any remaining formulation or method-of-use protections that can delay certain generic versions.

How exclusivity translates to market impact

- Orange Book-tied exclusivity: market share declines accelerate when competing products can legally launch without infringing remaining patents.

- Settlement structures: if patent litigation ends in partial settlements, the “effective” launch date can be later than generic manufacturing readiness.

Generic entry risk model for ER gabapentin brands

- Claim scope and formulation barriers: slower replication for ER release technologies can delay some entrants.

- Regulatory design-around: even when APIs are the same, release profile differences can determine acceptability and labeling equivalency.

What GRALISE patent estate issues matter for market exclusivity and litigation outcomes?

Featured snippet answer: The patent estate for GRALISE is most relevant at the margins: method-of-use, formulation, and specific ER delivery characteristics can affect whether a generic can launch and whether certain “authorized generics” can be substituted.

Patent estate categories that affect commercial timelines

- Formulation patents: ER matrix composition and release-control mechanisms.

- Method-of-use patents: dosing regimens and titration schedules.

- Manufacturing process patents: scale-up and ER production steps that may be easier to design around.

How litigation affects the P&L

- Delay value: every month of brand exclusivity or stay can protect high-margin brand TRx.

- Settlement economics: could include revenue sharing or launch dates that preserve market share.

Data constraint: No Orange Book, patent list, or litigation docket details are included in the provided input, so exact expiration dates, listed patents, and Paragraph IV events cannot be stated here.

What is the Orange Book status of GRALISE, and how many patents typically cover gabapentin ER products?

Featured snippet answer: Orange Book status determines whether generics can launch immediately (expiration or non-listed patents) or only after resolving patent disputes.

What to look for on the Orange Book (commercially)

- Drug substance patents (often long expired),

- drug product/formulation patents (most relevant to ER products),

- use patents (PHN indications can matter for labeling),

- exclusivity designations (new chemical entity vs other exclusivity types where applicable).

Data constraint: The number of Orange Book-listed patents, their identifiers, and their expiration dates cannot be enumerated without the Orange Book listings.

How does GRALISE FDA regulatory status influence prescribing and competitive switching?

Featured snippet answer: GRALISE’s FDA-approved labeling and ER dosing schedule influence pharmacy substitution policy and prescriber comfort, but the prescribing behavior shift is usually driven by payer access rather than FDA review pathways.

Relevant regulatory influences

- Labeling equivalence: generic labeling that permits substitution at the pharmacy reduces differentiation.

- Real-world substitution policies: once FDA-approved generics exist, switching can be rapid if payer policies permit.

Data constraint: Specific FDA milestones (application types, approval dates, and labeling revisions) are not provided in the input.

How strong is GRALISE’s financial trajectory versus key gabapentin ER peers?

Featured snippet answer: In mature gabapentinoid ER markets, the financial curve tends to follow a pattern: peak demand at launch, followed by steady TRx erosion from generic substitution, with net sales stability driven by rebate management, formulary positioning, and persistence of stabilized patients.

Peer comparison dimensions that determine outcomes

- Brand formulary penetration: preferred tier placement and reduction of PA barriers.

- Gross-to-net discipline: ability to protect net price through contract leverage.

- Patient support ROI: copay coverage effectiveness relative to patient out-of-pocket thresholds.

- Clinical policy alignment: whether formularies embed GRALISE-friendly coverage criteria.

Data constraint: No numeric revenue, TRx, or market share figures for GRALISE or peers are included in the provided input, so a quantitative ranking cannot be produced.

What generic entry scenarios pose the largest downside risk to GRALISE net sales?

Featured snippet answer: The biggest downside is rapid substitution when multiple interchangeable/generic ER products are covered without PA restrictions and when PBMs tighten the preferred tier so that GRALISE requires additional approvals.

Downside scenario structure

- Scenario A: “Open substitution” tightening

PBMs require no brand exception; brand share drops quickly at the pharmacy.

- Scenario B: Step edits and PA tightening

Patients must fail lower-cost alternatives (often immediate-release gabapentin or other neurologic options).

- Scenario C: Multiple generic launches within the same formulary contract cycle

Competitive contracting accelerates, compressing net sales through increased rebates.

Upside “offset” mechanisms

- Brand persistence programs: reduce switching due to discontinuation risk.

- Contract renewal strength: keep GRALISE in preferred tiers when cost-effective.

What is the revenue exposure profile for GRALISE by geography and channel?

Featured snippet answer: Exposure is primarily driven by US commercial and Medicare Part D formularies plus pharmacy channel substitution rates; changes in national PBM coverage can drive faster impact than incremental patient volume changes.

Channel drivers

- Wholesaler ordering patterns: can front-load purchases ahead of policy changes but reflect erosion once substitutions rise.

- Managed care concentration: impacts the pace of brand-to-generic shift.

Geography drivers

- US PBM and CMS influence: most direct for revenue because substitution rules and formulary coverage are determinative for scripts.

- International dynamics: depend on local patent status and local pricing regulation (not assessed here due to no provided country-level data).

Data constraint: No channel or geographic financial breakdown is provided in the input.

How does GRALISE’s market performance typically evolve through patent cliff and formulary reform?

Featured snippet answer: Market performance often shows lagged declines: TRx erodes after generic availability, while net sales may lag due to rebate structures, patient persistence, and channel inventory effects; acceleration follows when PBMs implement tighter coverage.

Lag mechanics

- Clinical inertia: patients stable on GRALISE often remain until forced switching.

- Contract timing: formulary updates and pharmacy benefit schedule changes can shift brand share quickly after renewal.

- Inventory and ordering cycles: can mask underlying script decline early.

Key Takeaways

- GRALISE’s commercial trajectory is dominated by PHN treated population persistence and payer contracting dynamics rather than by continued growth drivers.

- The principal downside lever is generic substitution of gabapentin ER once a payer environment permits open brand-to-generic switching with minimal PA barriers.

- Financial trajectory in mature neurology brands typically follows TRx erosion after generic entries, with net sales stability only if rebate and tier placement remain favorable.

- Patent and Orange Book status can delay certain launches, but exact expiration and litigation outcomes cannot be stated from the provided input.

FAQs

1. What drives GRALISE prescribing compared with immediate-release gabapentin?

ER dosing adherence, clinician familiarity, and coverage criteria for PHN in managed care plans tend to drive the preference versus IR products when formulary access supports it.

2. Does GRALISE have biosimilar risk like biologics?

No. GRALISE is a small-molecule drug and does not face biosimilar pathways.

3. What payer rules most often trigger GRALISE switching to generics?

Step therapy requirements, PA tightening, and movement to non-preferred tiers are the most common policy triggers.

4. What formulation differences matter commercially for ER gabapentin generics?

Release-profile equivalence and manufacturing control affect generic acceptability; payer substitution is faster when FDA-approved generics carry labels that allow pharmacy-level replacement.

5. How do settlement agreements change the practical timing of generic entry?

Settlements can set launch dates, restrict specific claim scopes, or structure market entry in ways that delay or limit substitution until the agreed window ends.

References

No sources were provided in the input.