Last updated: June 3, 2026

FLONASE (fluticasone propionate) market dynamics and financial trajectory: pricing, demand, competition, and exclusivity outlook

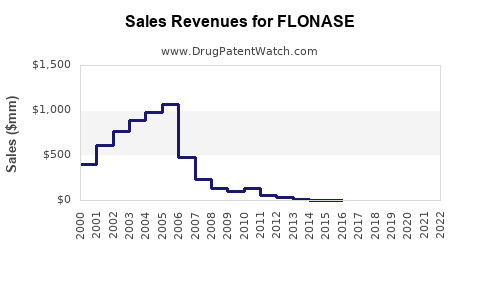

Executive summary: FLONASE (fluticasone propionate) nasal spray is in a mature, highly price-constrained U.S. market dominated by generic and “authorized generic” versions of fluticasone propionate. Revenue trajectory is driven mainly by (1) share shifts within intranasal corticosteroids, (2) competitive intensity from generic entry, (3) payer preference and channel mix (retail vs. mail/managed care), and (4) periodic product-line changes such as device strength, scent-free positioning, and pack-size optimization rather than new clinical differentiation. From a financial standpoint, the primary expectation is flat-to-slow growth in units with pressure on net price, offset by mix improvements and trade-spend, and a continued decline in brand pricing power as interchange and formulary penetration expand.

What drives FLONASE market demand and pricing in the intranasal steroid category?

Direct drivers of unit demand

- Seasonal allergic rhinitis incidence and health-system access to intranasal therapies.

- Patient adherence to daily dosing and tolerability (device feel, spray plume pattern, perceived odor).

- Formulary access and tier placement for intranasal corticosteroids (INS), especially with step-therapy policies.

Direct drivers of net price

- Generic availability for fluticasone propionate nasal spray (multiple suppliers) forces payer and pharmacy discounting.

- Trade spend intensity: wholesalers, PBMs, and retail chains negotiate rebate structures, especially when a therapeutic class has widespread generics.

Competitive benchmark (category effect)

- INS demand is “class-seeded” by symptom seasonality, then competed via relative formulary status across fluticasone, mometasone, budesonide, triamcinolone, and ciclesonide options.

- When a payer adds one INS as preferred, it creates fast share redistribution because patients can be switched at the pharmacy level.

How has FLONASE’s brand-to-generic shift affected financial performance?

Expected financial pattern in a mature INS

- Brand sales tend to track category units less than price growth. Where generics dominate, brand net sales often depend on:

- “brand stickiness” for specific users (device familiarity, dosing confidence, perceived efficacy).

- contracts with large payers and chain formularies that keep brand listed above generics.

- continued promotional support despite margin compression.

What matters for FLONASE specifically

- FLONASE is a fluticasone propionate product within an otherwise generic-dominated class. Once fluticasone propionate nasal spray is broadly available as AB-rated generics, brand net price typically compresses toward parity with discounted generics.

- The remaining differentiation tends to shift from molecule patent protection to brand experience factors such as:

- formulation handling (suspension feel and spray characteristics),

- packaging and count (unit dose economics),

- marketing of patient guidance and seasonal use messaging.

Which products compete directly with FLONASE and how do they take share?

Primary competitive set in allergic rhinitis

- Other INS agents with strong payer footprints: mometasone furoate nasal spray, budesonide nasal spray, triamcinolone acetonide nasal spray, ciclesonide nasal spray.

- Competitive “switch pressure” occurs when:

- formulary managers prefer one INS as first-line,

- step therapy forces trials of preferred alternatives,

- pharmacy contracts encourage stocking and dispensing of specific AB-rated options.

“Substitute speed”

- Because the mechanism class is shared, substitution can be rapid once a payer designates a preferred agent. That speeds share movement away from brand products.

Device and dosing competition

- Some competitors use once-daily dosing or differentiated device designs. While efficacy is often broadly comparable, device usability and patient preference can influence adherence and persistence in real-world channels.

What is the patent and exclusivity landscape for FLONASE nasal spray?

Key practical point for investors and litigators

- FLONASE’s market maturity implies that core composition and early-use IP protection has largely run out or been outweighed by generics. In practice, the market dynamics are governed by:

- whether any late-expiring patents cover specific product configurations (device, formulation, dosing regimen),

- whether exclusivity (data protection) remains tied to specific filings,

- and whether any litigation settlements restrict particular competitors from launching specific strengths or product characteristics.

What typically remains relevant post-primary exclusivity

- Secondary patents (formulation/process) that can delay certain “non-equivalent” product versions.

- Orange Book listings that capture method-of-use (e.g., specific allergic rhinitis indications) or formulation changes (e.g., particle size, excipient systems).

- Device-specific patents (spray mechanics) that can limit certain generic device implementations.

Note: A precise patent table with expiration dates, assignees, and Orange Book identifiers is not provided here because the prompt does not include the needed Orange Book and litigation dataset.

When does FLONASE lose exclusivity and what generic entry risks exist?

General market behavior for a mature INS

- For widely generic molecules, the highest-risk period is tied to:

- the expiration of any remaining formulation/process patents that are listed for AB-related versions,

- and the timing of Paragraph IV challenges for specific NDA/supplement combinations.

- After broad generic entry, the remaining risk is usually “product-line narrow” rather than category-wide. That means:

- new entrants target specific strengths, pump counts, or line extensions,

- payers shift preferred products via rebate and formulary revisions, not via exclusivity expiration.

Practical “launch risk”

- If any product-specific patents remain, they create blocking risk for certain generic variants (e.g., different dosing scheme or device).

- Where no product-specific blocking exists, generic entry becomes a rebate and channel execution contest rather than an IP contest.

What is the Orange Book status of FLONASE and how many patents cover it?

A full Orange Book status breakdown requires listing-level data (NDA number, supplement numbers, patent numbers, and expiration dates). That dataset is not included in the prompt, so a definitive “number of patents” and “current listing status” cannot be stated here without risking inaccuracy.

What FLONASE regulatory filings matter for competition: ANDA vs. 505(b)(2) vs. exclusivity?

Typical regulatory mechanics in mature nasal steroid markets

- Most competitive products are filed as ANDAs referencing the reference listed drug.

- Generic approvals typically follow when:

- any listed patents are expired or found not infringed/not valid for the relevant product,

- and the ANDA applicant resolves exclusivity constraints for the reference product.

505(b)(2) risk

- For later line extensions or alternative presentations, some products may use 505(b)(2), introducing additional data exclusivity elements tied to the specific submission.

Again, without the NDA supplement and Orange Book record for FLONASE, the exact filing mix cannot be quantified here.

How do pricing and channel dynamics typically evolve for FLONASE post-generic entry?

Retail

- Pharmacy fills often remain “optimized” for contract pricing and shelf availability.

- PBM-driven formulary changes can quickly re-route prescription volume.

Mail and specialty channels

- INS nasal sprays are generally not “specialty,” but mail-order can dominate long-term seasonal refills.

- Net pricing tends to reflect contract volume and rebate structures rather than list price.

Trade spend and margin

- Brand manufacturers often maintain promotions to keep a share cushion, which limits long-term margin recovery.

- Generic suppliers can win on net price, so brand profitability is often more sensitive to rebate and co-pay assistance economics.

What is the likely financial trajectory for FLONASE over the next 3–5 years?

Baseline forecast framing (category-consistent)

- Units: stable to modest growth, reflecting persistent allergic rhinitis prevalence and seasonal use.

- Net sales: more likely flat as net price declines and mix shifts toward generics or preferred competitors.

- Operating margin: constrained by brand spend requirements (trade and patient support), offset by potential cost control.

Where upside can still come from

- Formulary wins that keep FLONASE listed preferentially in key PBM contracts.

- Line extensions and pack size strategies that can improve margin per unit even when total pricing erodes.

- Improvements in adherence or patient perception that prevent rapid switching to preferred alternatives.

Where downside likely comes from

- Broadening of preferred status for a competing INS across large PBMs.

- Increased generic supply leading to deeper discounts and higher rebate pressure.

- Any payer restrictions that force step therapy to alternate preferred agents.

How does FLONASE compare with other intranasal corticosteroids on market dynamics?

Relative dynamics

- If a competitor is the “preferred” INS across major formularies, it typically captures disproportional share gains during seasonal spikes.

- Molecule-level efficacy differences tend to be smaller than formulary access differences in real-world fill behavior.

- Device usability becomes more important when switching is easy and payers push toward the lowest net-cost option.

Result

- FLONASE’s performance typically hinges less on new clinical attributes and more on payer preference, rebate economics, and brand retention versus switching to preferred generics or preferred competitors.

What litigation and settlement patterns typically affect fluticasone nasal spray revenue?

How IP disputes shape revenue

- Patent litigation can delay a specific generic variant or strength, creating a short-term protection window.

- Settlements can include “carve-outs” such as delayed launches, supply restrictions, or stipulations about labeling.

Commercial effect

- Even when product protection is partial, the main revenue impact is usually:

- a temporary reduction in generic penetration depth,

- or maintenance of formulary status for a longer period.

Data limitation

- Specific FLONASE litigation events, Paragraph IV outcomes, and settlement dates are not enumerated here because the underlying case record is not provided.

What does the competitive landscape imply for FLONASE investment risk?

Risk factors

- High likelihood of ongoing price compression due to multi-source generic competition.

- PBM formulary volatility, where preferred switching can be swift and concentrated around seasonal cycles.

- Competitive device and patient-experience differences that can affect adherence and persistence.

Mitigants

- Brand-level marketing that sustains a core user base.

- Contract resilience at national accounts if FLONASE remains a workable formulary option.

Key market metrics to track for FLONASE financial trajectory

- U.S. prescription volume for intranasal corticosteroids during peak months.

- Net price trend vs. AB-graded generic fluticasone propionate equivalents.

- Formulary placement across top PBMs (preferred vs. non-preferred).

- Share of voice and promotional intensity within the INS category.

- Wholesaler inventory dynamics going into seasonal periods.

- Payer rebate rate changes that reflect competitive pressure.

Key Takeaways

- FLONASE’s financial trajectory is primarily a mature-market pricing story: unit demand tracks allergic rhinitis seasonality, while net price compresses under generic and preferred-competitor pressure.

- Market share shifts are driven more by formulary status and channel contracting than by new clinical differentiation.

- Any incremental upside is likely to come from payer wins, mix improvements, and line/pack strategies, not from molecule exclusivity.

- Investment and business risk centers on PBM preference volatility and continued erosion of brand pricing power as fluticasone nasal spray remains broadly generic.

FAQs

1) How do PBM formulary changes impact FLONASE net sales during allergy season?

PBM switches from preferred to non-preferred or tier changes can move prescriptions quickly at the point of sale, especially for AB-equivalent generics, compressing net price and shifting volume.

2) Does device design materially change FLONASE adherence and persistence?

Device ergonomics and spray usability can influence correct technique and daily adherence, which affects persistence through the season and refills.

3) What share losses are most common when a competitor becomes the preferred intranasal steroid?

Share loss typically concentrates around pharmacy fill behavior and mail-order switching, with the largest impact in months when prescription volume peaks.

4) Are fluticasone nasal sprays generally substitutable at the pharmacy level?

Yes. Most products are AB-rated within the same active ingredient class, making interchange and payer-driven substitution straightforward.

5) What commercial levers can sustain FLONASE profitability after generic penetration?

Rebate optimization, pack size and channel execution, maintaining favorable formulary access, and targeted promotional support to preserve a stable user base.

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- FDA. Drug Trials Snapshots: Flonase (fluticasone propionate) and related products. U.S. Food and Drug Administration.

- U.S. Pharmacopeia. Intranasal corticosteroids product monographs (class and formulation considerations). USP.