Last updated: April 24, 2026

What is EMVERM’s market position and commercial structure?

EMVERM is a brand name for mebendazole (anti-helminthic), marketed in the U.S. and sold through standard prescription and wholesaler channels. Commercial performance is primarily driven by:

- Low-cost, off-patent status of the active ingredient (mebendazole), which compresses branded pricing and shifts market share toward lower net-price options.

- Limited label expansion typical of older parasitic indications, which keeps total addressable use relatively stable rather than growth-led.

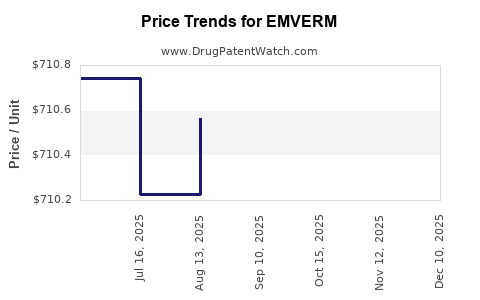

- Channel inventory dynamics that can create short-run revenue volatility, especially around supply continuity and wholesaler reorder timing.

Implication for financial trajectory: the product behaves more like a mature, price-sensitive commodity than a pipeline-like franchise. Revenue typically follows baseline demand and periodic pricing/contract changes rather than durable, product-specific growth.

How do pricing and competition shape EMVERM revenue?

For older anthelmintics where generics exist, branded performance hinges on net price after rebates and wholesaler discounts. The competitive pressure typically comes from:

- Generic mebendazole (multiple manufacturers in most mature markets).

- Therapeutic substitution within intestinal parasite treatment classes (patients and prescribers often shift based on availability, coverage, and formulary placement rather than clinical differentiation).

Market consequence:

- Branded share erosion tends to be structural. Even when EMVERM maintains a presence, the addressable “willingness to pay” declines as payers and formularies steer to generics.

- Revenue is more sensitive to contract terms (payer/wholesaler) than to demand growth.

Business read-through: long-term revenue durability is possible if EMVERM retains formulary access and consistent supply, but sustained growth is difficult under generic price competition.

What demand drivers matter for EMVERM?

EMVERM’s demand is tied to the epidemiology and treatment patterns of intestinal helminth infections and to guideline-based use. Key drivers include:

- Seasonality and outbreak cycles in certain regions, which can affect incident treatments.

- Public health and access programs that can influence which products are purchased and when.

- Formulary placement in pediatric and primary care settings, since dosing regimens and safety profiles support recurring prescribing in routine workflows.

Financial consequence: demand is typically stable-to-modest, with periodic fluctuations rather than sustained multi-year growth.

What regulatory and supply factors influence the financial path?

For mature oral anthelmintics, financial swings often track operational factors:

- Manufacturing continuity and product availability (temporary shortages can produce both lost sales and subsequent “catch-up” buying).

- Pack-size and distribution changes (case pack economics and wholesaler stocking).

- Quality and compliance events that can trigger distribution disruptions.

Financial consequence: revenue can show “lumpy” periods even when underlying disease burden is steady.

How does payer coverage affect profitability and net sales?

Net revenue for branded mature products is shaped by:

- Rebate/discount structure relative to generic benchmarks.

- Coverage tier placement within drug formularies.

- Switching behavior at the pharmacy counter when a lower-cost equivalent is preferred.

Financial consequence: even when gross list pricing holds, net sales and margin compress as payers push toward generics. EMVERM’s profitability profile therefore tends to be constrained by:

- Lower achievable net prices.

- Higher promotional and contract costs to preserve access.

What is the most likely revenue and cashflow trajectory for EMVERM?

Trajectory type: mature, contract-driven, price-constrained.

A typical pattern in this category is:

- High historical brand share that declines after generic entry.

- Revenue flattening after initial competitive shock.

- Periodic dips and recoveries tied to supply and wholesaler contracting.

- Ongoing margin pressure due to net price compression.

Financial expectation for EMVERM:

- Net sales are likely to grow slowly or decline slowly in nominal terms, unless EMVERM retains niche formulary position or avoids major supply disruption.

- Gross margin remains limited versus newer branded therapies because the benchmark price is set by generics.

- Cash generation is still usually positive because working capital needs and R&D are not the dominant drivers for an established, off-patent product, but earnings quality depends on contract stability.

What market metrics should be monitored to track EMVERM performance?

To actively manage a mature, off-patent brand under generic pressure, track:

- Net price vs. generic basket (quarterly by channel and pack).

- Wholesaler inventory levels and fill rates (to anticipate revenue timing).

- Formulary status by segment (commercial adult vs pediatric coverage patterns).

- Prescription counts and script-to-bill conversion at retail and specialty-like carve-outs (if applicable).

- Average net sales per unit (to separate volume from price effects).

These metrics map directly to the revenue mechanics in commodity-like pharma segments.

How does EMVERM’s therapeutic profile feed demand stability?

Mebendazole regimens for intestinal helminth infections are:

- Clinically established

- Often integrated into routine primary care prescribing workflows

- Supported by consistent efficacy and established safety monitoring norms

That said, the clinical similarity to other off-patent options means therapeutic advantage rarely translates into pricing power.

Financial consequence: steady baseline demand exists, but it does not usually drive brand premium economics.

What are the investment and R&D implications from EMVERM’s dynamics?

For investors and strategists, EMVERM’s market dynamics imply:

- Low upside from demand growth absent a major payer or supply catalyst.

- Material downside from net price deterioration if contracts reprice to generic levels.

- Value focus shifts to operational execution, contract renewals, and avoiding supply disruptions.

For R&D strategy, the broader lesson is:

- Older antiparasitics generally monetize through low-cost manufacturing, stable supply, and channel management, not through margin expansion.

Key Takeaways

- EMVERM’s commercial trajectory is mature and price-constrained, with revenue driven more by contracting, net pricing, and supply continuity than by growth-led demand.

- Generic mebendazole competition structurally limits branded net price and compresses margin.

- Financial performance tends to show flattening trends with periodic volatility from channel and operational factors.

- The strongest indicators of near-term results are net price vs generic basket, wholesaler inventory and availability, and formulary access by segment.

FAQs

1) Is EMVERM expected to grow faster than generic competitors?

No. Brand economics in off-patent mebendazole typically lag generic basket outcomes because net price converges toward lower-cost equivalents.

2) What usually causes short-term revenue swings for established anthelmintics?

Supply continuity, wholesaler stocking cycles, and contract repricing timing are common causes; underlying infection incidence changes are usually slower and less directly tied to quarter-to-quarter revenue.

3) Does EMVERM have durable payer leverage?

Durability depends on formulary status and contract terms, but payer steering toward generics typically reduces long-run leverage for branded versions.

4) What operational metrics best predict profitability for EMVERM?

Average net sales per unit, rebate levels, gross margin after chargebacks, and fill-rate/availability metrics are the most predictive.

5) What is the most realistic long-term financial profile for EMVERM?

A stable-to-slow decline revenue profile with margin pressure, unless the company maintains a niche channel position or avoids competitive contract deterioration.

References

[1] FDA. “EMVERM (mebendazole) prescribing information.” U.S. Food and Drug Administration.

[2] DailyMed. “EMVERM (mebendazole) label.” National Library of Medicine.

[3] WHO. “Soil-transmitted helminth infections.” World Health Organization.

[4] CMS. “Medicare Part D Drug Spending and Utilization (dataset and methodology documentation).” Centers for Medicare & Medicaid Services.