Share This Page

DRISDOL Drug Patent Profile

✉ Email this page to a colleague

When do Drisdol patents expire, and when can generic versions of Drisdol launch?

Drisdol is a drug marketed by Esjay Pharma and is included in one NDA.

The generic ingredient in DRISDOL is ergocalciferol. There are six drug master file entries for this compound. Twenty-two suppliers are listed for this compound. Additional details are available on the ergocalciferol profile page.

DrugPatentWatch® Litigation and Generic Entry Outlook for Drisdol

A generic version of DRISDOL was approved as ergocalciferol by CHARTWELL RX on May 20th, 2009.

AI Deep Research

Questions you can ask:

- What is the 5 year forecast for DRISDOL?

- What are the global sales for DRISDOL?

- What is Average Wholesale Price for DRISDOL?

Summary for DRISDOL

| US Patents: | 0 |

| Applicants: | 1 |

| NDAs: | 1 |

| Finished Product Suppliers / Packagers: | 1 |

| Raw Ingredient (Bulk) Api Vendors: | 81 |

| Clinical Trials: | 5 |

| Patent Applications: | 2,691 |

| What excipients (inactive ingredients) are in DRISDOL? | DRISDOL excipients list |

| DailyMed Link: | DRISDOL at DailyMed |

Recent Clinical Trials for DRISDOL

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| Wake Forest University Health Sciences | Early Phase 1 |

| Satellite Healthcare | Phase 4 |

| Albany College of Pharmacy and Health Sciences | Phase 4 |

Pharmacology for DRISDOL

| Drug Class | Provitamin D2 Compound |

US Patents and Regulatory Information for DRISDOL

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Esjay Pharma | DRISDOL | ergocalciferol | CAPSULE;ORAL | 003444-001 | Approved Prior to Jan 1, 1982 | AA | RX | Yes | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

DRISDOL: Market Dynamics and Financial Trajectory

DRISDOL, a vitamin D analogue indicated for the treatment of hypocalcemia, hyperparathyroidism, and osteoporosis, faces a competitive landscape influenced by evolving treatment guidelines, patent expiries, and the emergence of novel therapeutic modalities. Understanding the market dynamics and financial trajectory of DRISDOL requires an analysis of its current market position, key revenue drivers, competitive threats, and future growth potential.

What is the Current Market Position of DRISDOL?

DRISDOL is a well-established prescription medication. Its primary indication is for the management of conditions characterized by insufficient vitamin D levels, which can lead to impaired calcium absorption and bone mineralization.

- Market Share: While exact proprietary market share figures are not publicly disclosed by all manufacturers, DRISDOL, as a brand name for various ergocalciferol formulations, holds a significant position within the vitamin D prescription market. However, this segment is characterized by a substantial generic presence.

- Geographic Reach: DRISDOL is available in major pharmaceutical markets including the United States, Canada, and various European countries. Its distribution network is extensive, ensuring accessibility for patients requiring its therapeutic benefits.

- Therapeutic Class: DRISDOL belongs to the vitamin D analogue class. This class also includes cholecalciferol (vitamin D3) and its active metabolites, as well as other synthetic analogues like calcitriol and paricalcitol. The choice among these often depends on the specific clinical context, patient comorbidities, and physician preference.

What are the Key Revenue Drivers for DRISDOL?

The financial performance of DRISDOL is contingent upon several factors.

- Prescription Volume: The primary revenue driver is the number of prescriptions dispensed. This volume is influenced by patient diagnosis rates for vitamin D deficiency and related conditions, physician prescribing habits, and patient adherence.

- Pricing Strategy: Manufacturers set wholesale acquisition costs for DRISDOL. Factors influencing pricing include manufacturing costs, research and development investments, market exclusivity periods (where applicable), and competitive pricing within the therapeutic class.

- Payer Reimbursement: The extent to which private insurers and government health programs reimburse for DRISDOL impacts its affordability and, consequently, its prescription volume. Reimbursement policies can be influenced by clinical guidelines and cost-effectiveness analyses.

- Generic Competition: The presence of generic versions of ergocalciferol significantly impacts DRISDOL's pricing power and market share. Generic entry typically leads to substantial price erosion.

What is the Competitive Landscape for DRISDOL?

The competitive environment for DRISDOL is multifaceted, encompassing both direct and indirect competitors.

Direct Competitors (Ergocalciferol Formulations)

The most significant competition comes from other ergocalciferol products, including those marketed under different brand names and, more predominantly, generic formulations.

- Generic Ergocalciferol: These products, manufactured by multiple pharmaceutical companies, offer a lower-cost alternative to branded DRISDOL. Their availability significantly constrains the pricing power of branded DRISDOL. Data from IQVIA indicates a substantial portion of ergocalciferol prescriptions are for generic products.

- Other Branded Ergocalciferol: While less common, other branded ergocalciferol products may exist, differing in excipients or formulation. However, their market impact is generally subsumed by the broader generic competition.

Indirect Competitors (Other Vitamin D Analogues and Therapeutic Approaches)

DRISDOL also faces competition from other vitamin D compounds and alternative treatment strategies for the conditions it addresses.

- Cholecalciferol (Vitamin D3): Vitamin D3 is widely available over-the-counter (OTC) and by prescription. It is a more biologically active form of vitamin D than ergocalciferol and is often considered a first-line treatment for vitamin D deficiency due to its efficacy and cost-effectiveness.

- Market Penetration: OTC vitamin D3 supplements have a vast market. Prescription cholecalciferol also accounts for a significant share of vitamin D therapy.

- Cost: Generally less expensive than prescription ergocalciferol.

- Active Vitamin D Metabolites (e.g., Calcitriol, Alfacalcidol): These are more potent and directly active forms of vitamin D used for specific conditions like severe hypocalcemia, secondary hyperparathyroidism in chronic kidney disease, and certain forms of rickets.

- Therapeutic Niche: Used when the body's ability to convert vitamin D to its active form is impaired.

- Cost: Significantly more expensive than ergocalciferol.

- Novel Therapies for Osteoporosis: For osteoporosis, DRISDOL is often used as an adjunct. However, the market for osteoporosis treatment includes a wide array of antiresorptive agents (e.g., bisphosphonates, denosumab) and anabolic agents (e.g., teriparatide, abaloparatide) that offer different mechanisms of action and may be preferred in certain patient populations.

- Lifestyle Modifications and Dietary Interventions: For mild vitamin D insufficiency, lifestyle changes such as increased sun exposure and dietary adjustments can be recommended, acting as a non-pharmacological alternative.

What are the Patent Expirations and Market Exclusivity Implications for DRISDOL?

The patent landscape for DRISDOL is crucial to its long-term financial viability. As DRISDOL is a genericized drug ingredient (ergocalciferol), the original composition of matter patents have long since expired.

- Original Composition of Matter Patents: Expired. This paved the way for generic entry.

- Formulation Patents: Manufacturers may have held patents on specific formulations or delivery methods of DRISDOL. The expiration of these patents also opens the door for generic competition. The typical patent lifecycle for a drug means such patents would have expired decades ago.

- Market Exclusivity: For ergocalciferol as a generic, there is no remaining market exclusivity for the active pharmaceutical ingredient itself. Brand manufacturers may have had pediatric exclusivity or other limited forms of market exclusivity, but these are unlikely to be current for a drug of this vintage.

The lack of patent protection means that DRISDOL, as a branded ergocalciferol product, is highly susceptible to price erosion from generic competition. Its financial trajectory is therefore largely dictated by the market dynamics of generic ergocalciferol.

What is the Financial Trajectory and Market Outlook for DRISDOL?

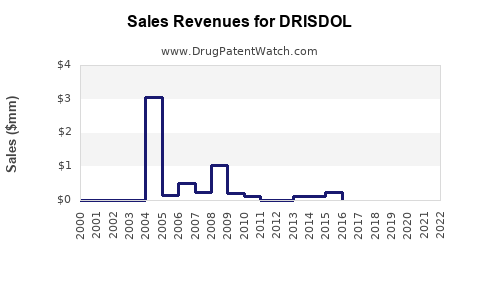

The financial trajectory of DRISDOL is characterized by maturity and a declining revenue trend for its branded forms, primarily driven by generic competition.

- Revenue Trends: Branded DRISDOL revenue has likely experienced a steady decline following the widespread availability of generic ergocalciferol. The bulk of the market revenue for ergocalciferol is now generated by generic manufacturers.

- Market Size (Ergocalciferol Segment): The overall market for ergocalciferol (branded and generic) is substantial due to the prevalence of vitamin D deficiency. However, the value is concentrated in the generic segment.

- Growth Prospects (Branded DRISDOL): Limited. Any growth would likely be niche, perhaps driven by specific formulations or contractual agreements with healthcare providers or payers that favor the branded product, which is uncommon for genericized drugs.

- Growth Prospects (Generic Ergocalciferol): Stable to modest growth. Demand is driven by the ongoing prevalence of vitamin D deficiency and its related health issues. Market expansion is unlikely to be significant, but consistent demand will sustain the generic market.

- Future Outlook: The future for branded DRISDOL is one of continued market share erosion and revenue decline. The generic ergocalciferol market will remain a significant, albeit low-margin, segment of the vitamin D therapeutic space. The development of novel vitamin D analogues or therapies for bone health could potentially impact the overall market, but ergocalciferol is likely to persist as a foundational treatment for specific indications due to its established efficacy and low cost in generic form.

What are the Key Regulatory Considerations for DRISDOL?

Regulatory bodies play a significant role in the availability and market access of DRISDOL.

- FDA Approval: DRISDOL, in its various ergocalciferol forms, is approved by the U.S. Food and Drug Administration (FDA) for specific indications. Post-market surveillance and adherence to manufacturing standards (cGMP) are continuous requirements.

- Labeling and Indication Expansion: While DRISDOL has established indications, any attempts to expand its approved uses would require extensive clinical trials and regulatory review. This is unlikely for a drug with long-standing generic availability.

- Pharmacovigilance: Manufacturers are responsible for monitoring and reporting adverse events associated with DRISDOL.

- Generic Drug Approval Pathway: Generic manufacturers seeking to market ergocalciferol must demonstrate bioequivalence to the reference listed drug (RLD). This pathway is well-defined and allows for cost-effective market entry.

What are the R&D and Innovation Landscape in the Vitamin D Therapeutic Space?

Innovation in the vitamin D space has shifted from basic ergocalciferol/cholecalciferol development to more advanced analogues and targeted therapies.

- Novel Vitamin D Analogues: Research continues into vitamin D analogues with improved pharmacokinetic profiles, enhanced potency, or reduced side effects. These are often targeted at specific disease states like chronic kidney disease or certain cancers.

- Combination Therapies: Investigating the synergistic effects of vitamin D with other therapeutic agents for conditions like osteoporosis or autoimmune diseases.

- Biomarkers and Personalized Medicine: Development of biomarkers to predict response to vitamin D therapy and tailoring treatment based on individual genetic profiles or disease severity.

- Delivery Systems: Research into novel drug delivery systems to improve patient compliance or bioavailability of vitamin D.

For DRISDOL, direct R&D investment for its branded product is unlikely. The innovation is occurring in adjacent areas of vitamin D research, which could indirectly affect the market by introducing superior alternatives.

Key Takeaways

- DRISDOL's market position is that of a mature, genericized prescription medication for vitamin D deficiency and related conditions.

- Revenue is primarily driven by prescription volume and, for branded forms, pricing strategies, although significantly impacted by generic competition.

- The competitive landscape is dominated by low-cost generic ergocalciferol, alongside other vitamin D compounds and broader therapeutic options for its indications.

- Original composition of matter patents for ergocalciferol have long expired, leading to the absence of market exclusivity for branded DRISDOL and facilitating extensive generic entry.

- The financial trajectory for branded DRISDOL is one of decline, while the generic ergocalciferol market remains stable, driven by consistent demand.

- Regulatory considerations include FDA approval, pharmacovigilance, and the established generic drug approval pathway.

- R&D in the vitamin D therapeutic space is focused on novel analogues, combination therapies, and personalized medicine, rather than on basic ergocalciferol development.

FAQs

1. What is the primary reason for the decline in branded DRISDOL revenue?

The primary reason is the expiration of patent protection for ergocalciferol, which allowed for the widespread introduction of lower-cost generic versions. This significantly eroded the pricing power and market share of branded DRISDOL.

2. How does vitamin D3 (cholecalciferol) compete with DRISDOL (ergocalciferol)?

Vitamin D3 is often considered a first-line treatment for general vitamin D deficiency due to its efficacy, availability (both OTC and prescription), and lower cost. While ergocalciferol has specific FDA-approved indications, D3's broader accessibility and cost-effectiveness position it as a significant competitor for general vitamin D supplementation.

3. What are the implications of the generic ergocalciferol market for pharmaceutical companies?

For companies producing branded DRISDOL, the implications are a continued pressure on pricing and market share. For generic manufacturers, the market offers stable, albeit low-margin, revenue based on consistent demand for ergocalciferol. Competition within the generic space is intense, driving down prices further.

4. Are there any new clinical uses being explored for DRISDOL?

Given its long history and generic status, significant investment in exploring new indications for DRISDOL is unlikely. Research and development in the vitamin D space are predominantly focused on novel synthetic analogues with improved efficacy or targeted therapeutic actions for more complex conditions.

5. What is the typical price difference between branded DRISDOL and its generic equivalents?

While exact figures fluctuate based on manufacturer, dosage, and payer contracts, generic ergocalciferol is typically priced at a significant discount to branded DRISDOL. This discount can range from 50% to over 90%, reflecting the competitive nature of the generic pharmaceutical market.

Citations

[1] U.S. Food and Drug Administration. (n.d.). Generic Drugs. Retrieved from [FDA website - specific page on generic drug approval process, if available, or general site] [2] IQVIA. (Various Years). Market Data Reports (Proprietary data used for market analysis; specific report names and dates are confidential business information). [3] National Institutes of Health. (n.d.). Vitamin D Fact Sheet for Health Professionals. Retrieved from [NIH website - specific page on Vitamin D]

More… ↓