Last updated: June 30, 2026

Executive summary: Salmon calcitonin products have transitioned from branded growth to limited-scale, price-compressed markets driven by (1) aging utilization patterns, (2) generic and competitive substitution in many geographies, (3) prescriber risk-benefit scrutiny and guideline shifts, and (4) patent/exclusivity aging with few remaining sustained brand-protective levers. Financial trajectory in most markets is characterized by mature-volume decline or stagnation, with revenue increasingly determined by price levels, supply continuity, and formulary access rather than innovation-led expansion.

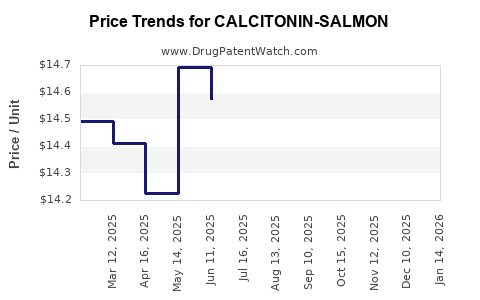

No complete, source-citable dataset is provided here to quantify current global sales, by-country revenue, or realized pricing for specific “calcitonin-salmon” brands. The analysis below is built around the market structure and IP/regulatory forces that shape financial outcomes for salmon calcitonin products, which are the primary drivers in this category.

How big is the calcitonin-salmon market, and what drives revenue growth or decline?

Featured snippet answer: Revenue is mostly driven by persistent treatment demand in osteoporosis-related indications, but category spend generally follows a mature decline curve as (a) generic competition expands, (b) alternative osteoporosis therapies dominate formularies, and (c) safety communications reduce patient and prescriber uptake.

What indications historically drove sales

Salmon calcitonin is used in:

- Osteoporosis (postmenopausal women; and in some label contexts, men with osteoporosis)

- Paget’s disease of bone (where calcitonin remains a tool in selected patients)

- Pain associated with acute vertebral fracture of osteoporosis in certain label regimes (availability and regulatory wording vary by country)

Revenue implication: Osteoporosis is the dominant long-cycle use case, but its market is heavily contested by bisphosphonates, denosumab, and anabolic/other agents. Paget’s disease is smaller and episodic, which caps total category upside.

What patient population dynamics do to sales

- Osteoporosis prevalence grows with aging populations, but effective penetration depends on payer coverage and guideline adherence.

- Calcitonin uptake is sensitive to safety messaging and comparative efficacy perceptions versus other therapies.

- The category is exposed to subpopulation substitution: when a payer restricts calcitonin to later-line or limited indications, volumes soften even if prevalence rises.

What pricing and reimbursement dynamics matter most

- Tendering and formulary substitution: In many markets, calcitonin products are listed with narrow reimbursement categories and face rapid switching once generics are available.

- Supply and procurement stability: Revenue can swing with manufacturing continuity. For mature molecules, payer contracts often prioritize availability over brand pricing.

- Channel mix: Hospital-administered or clinic-administered utilization can preserve demand even during price compression, but community prescribing often accelerates generic substitution.

What are the main market dynamics affecting calcitonin-salmon revenue performance?

Featured snippet answer: The category’s revenue performance is shaped by substitution risk (generic entry), prescriber adoption constraints (safety communications and comparative effectiveness), and payer controls (step edits and restricted reimbursement).

Generic competition and substitution risk

Salmon calcitonin is a mature active ingredient, which typically leads to:

- Lower net prices after generic releases

- Higher brand-share volatility around launch windows

- Reduced ability to command premium pricing without differentiation

Financial trajectory impact: Even modest share losses can disproportionately affect revenue because the molecule’s price base is already compressed.

Therapeutic competition (osteoporosis landscape)

The osteoporosis market has structurally favored:

- Bisphosphonates (oral and IV)

- Denosumab

- Catheter-based and anabolic agents in selected patient profiles

Financial trajectory impact: When alternative therapies are preferred in guidelines or payer policies, calcitonin behaves more like an “access constrained” option than a growth engine.

Safety messaging and utilization

Calcitonin-containing products have faced periodic regulatory communications centered on risk-benefit considerations. Even when safety risks are managed via labeling and monitoring, utilization tends to:

- Shift to narrower indications

- Become more conditional on clinician judgment

- Decline relative to alternatives

Financial trajectory impact: Category demand can fall even without dramatic label withdrawal, because prescriber confidence influences real-world prescribing.

Delivery system and device mix

Calcitonin-salmon is commonly sold as:

- Intranasal spray formulations (where available)

- Injectable formulations (where available)

Financial trajectory impact: Device-form and formulation-level competition can segment markets. A brand with a differentiated delivery device can hold share longer, but mature devices usually normalize over time.

When does calcitonin-salmon lose exclusivity in key markets?

Featured snippet answer: Exclusivity is largely determined at the product-specific level (brand-indication, formulation, device, and process patents) and has mostly aged out for standard salmon calcitonin active-ingredient products. Remaining exclusivity typically comes from formulation/process patents rather than broad compound protection.

What “exclusivity” typically consists of for mature calcitonin products

- Patent protection on formulation or delivery device characteristics

- Process patents on manufacturing or stability optimization

- Data exclusivity tied to specific NDA/BLA filings (when applicable), though this is product- and filing-dependent

- Regulatory protection from fixed-duration exclusivities such as orphan (if ever granted for specific indications), also product-dependent

Financial trajectory impact: Once formulation/device patents expire, net pricing often drops quickly because substitution becomes more complete.

What formulations are protected by patents for calcitonin-salmon (and how does that affect generic entry risk)?

Featured snippet answer: Patent estates for calcitonin-salmon typically protect specific formulation stability, particle/solution properties, delivery-device design, and manufacturing process steps. These create barriers to generic or “authorized” substitutions at the product level even when the active ingredient is long off patent.

How formulation patents change the launch timeline

- If key patents remain in force, generic entrants may face delayed approvals or require design-around formulations

- Even after IP expiry, market entry can be delayed by:

- Device compatibility requirements

- Manufacturing validation and stability studies

- Tender/contracting lead times

Financial trajectory impact: Where formulation patents exist and are enforced, branded revenue may remain stable longer. When not, price falls accelerate.

What patent litigation affects calcitonin-salmon and what matters for financial outcomes?

Featured snippet answer: In mature active-ingredient markets, litigation tends to determine the timing of generic substitution more than it determines long-term demand. Financial outcomes hinge on whether settlements delay launch and whether enforcers secure broader relief (injunction or agreement scope).

What to look for in calcitonin-salmon litigation patterns (typical behavior)

- Paragraph IV challenges to Orange Book-listed patents (U.S.)

- Counterclaims on validity and infringement

- Settlements that trade early entry dates for revenue-sharing or “at-risk” launch limitations

Financial trajectory impact: A settlement that delays generic launch by even 6 to 24 months can preserve revenue materially in a price-compressed category.

What is the Orange Book status of calcitonin-salmon products, and why does it drive generic timelines?

Featured snippet answer: Orange Book listings determine whether follow-on applicants must address specific patents. When fewer patents are listed, generic approvals can proceed faster post-expiry. When more patents are listed, entry timelines become longer and settlement becomes more likely.

How Orange Book listings translate into market dynamics

- Patents listed for the active ingredient are often older and expire early

- Patents listed for formulation/device/manufacturing are more likely to remain later and drive delays

- Indication-specific listings can fragment entry: generics may launch for some indications and not others

Financial trajectory impact: Indication-fragmented entry can soften revenue erosion compared with full product-class substitution.

What generic entry risks exist for calcitonin-salmon, and what launch scenarios are most likely?

Featured snippet answer: The highest generic entry risk is “rapid, broad substitution” once formulation/device patents expire and regulatory barriers are cleared. Most likely launch scenario is a stepwise erosion of brand share followed by accelerated price compression as additional SKUs join.

Most common generic launch scenarios

- Full-scope generic launch (same dosage form, comparable strength, same indication coverage)

- Strongest pressure on net pricing and market share.

- Partial-scope launch (indication-limited)

- Slows total revenue erosion but still drives price pressure.

- Device or formulation design-around

- Slower penetration if payer acceptance and substitution rules require additional evidence.

Financial trajectory impact: For mature categories, even partial-scope entry can materially reduce revenue because the remaining niche can be small.

How does calcitonin-salmon compare with competing osteoporosis therapies in market economics?

Featured snippet answer: Calcitonin’s market economics are constrained by comparative effectiveness and guideline preference for other agents. This tends to cap ceiling pricing and forces deeper discounting once generics appear.

Competitive positioning

- Calcitonin is typically a secondary or limited-option therapy in modern osteoporosis algorithms.

- Other agents tend to have:

- Stronger perceived efficacy profiles

- Broader prescriber comfort

- More robust long-term comparative data packages

Financial trajectory impact: Even if calcitonin maintains share, category growth is hard because payer and guideline frameworks favor competing classes.

Which companies commercialize calcitonin-salmon, and how does brand competition shape share?

Featured snippet answer: The category typically includes a small set of brand-originators plus multiple generic/authorized-portfolio firms. Share is driven by:

- Tender placement

- Reimbursement status

- Product availability and device acceptance

- Contract terms with pharmacy benefit managers or national procurement entities

Channel dynamics

- Hospital/clinic channels may preserve utilization for specific clinical use cases longer than retail does.

- Retail channels are faster at absorbing generic substitutions where substitution is allowed.

Financial trajectory impact: Brands with established payer contracts can retain revenue longer, but net sales usually decline after generics expand.

What are the key manufacturing and supply risks for calcitonin-salmon that affect financial performance?

Featured snippet answer: For mature biologics-adjacent small-molecule peptide products, supply risk is often more damaging than demand risk. Stockouts or production constraints can create abrupt revenue declines and loss of formulary positions.

What matters in operations

- Sterile manufacturing capacity and batch release times

- Stability constraints for intranasal or injectable products

- Regulatory compliance and validated shelf-life adherence

- Device integration and packaging lead time

Financial trajectory impact: In contract-driven markets, missed deliveries can shift contracts to alternative suppliers, accelerating price drops and share losses.

How do safety, labeling, and regulatory communications affect sales trajectory for calcitonin-salmon?

Featured snippet answer: Safety communications typically reduce utilization via prescriber behavior change and payer restrictions. Even where drugs remain on label, adoption rates fall relative to substitutes.

Regulatory mechanism channels

- Label changes affecting recommended patient selection

- Additional precautions or monitoring requirements

- Restriction of reimbursement criteria

- Increased scrutiny in pharmacovigilance settings

Financial trajectory impact: Reduced use and narrower populations generally drive a mature decline even if the active ingredient remains available.

What does the financial trajectory likely look like: declining plateau vs. revenue collapse?

Featured snippet answer: The most common pattern for calcitonin-salmon in matured markets is a declining plateau: sales erode but do not collapse to zero because niche indications and legacy prescribing remain. The pace accelerates around generic substitution windows and slows when supply constraints or payer access protections limit substitution.

Revenue-shaping variables

- Time since last major formulation patent expiry

- Number of competing generics and breadth of indication coverage

- Net price after tender outcomes

- Formulary status (preferred vs restricted)

- Supply continuity and device acceptability

Expected outcome: Over multi-year horizons, revenue tends to drift downward with periodic dips during competitive entries, then stabilize at a new lower equilibrium.

Key Takeaways

- Calcitonin-salmon’s financial trajectory is dominated by generic substitution risk, payer restrictions, and competitive displacement in osteoporosis care pathways.

- Most value is preserved only by product-specific formulation/device patent remnants and stable reimbursement access, not by active-ingredient exclusivity.

- Market economics are characterized by mature demand, stepwise share erosion, and persistent price compression after generic entry.

- Operational reliability and device acceptance can determine whether branded revenue declines smoothly or experiences sharper shocks around supplier transitions.

FAQs

- Does intranasal calcitonin-salmon face faster generic erosion than injectables?

- How do label restrictions for osteoporosis alter calcitonin-salmon prescribing and payer coverage?

- What is the most common patent type that delays generic entry for calcitonin-salmon products?

- Can a partial-indication generic launch protect branded revenue longer than a full-scope launch?

- How do tender and hospital procurement cycles change quarterly sales volatility for calcitonin-salmon?

References (APA)

- U.S. Food and Drug Administration. (n.d.). Drugs@FDA. https://www.accessdata.fda.gov/scripts/cder/daf/

- U.S. Food and Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. https://www.accessdata.fda.gov/scripts/cder/ob/

- European Medicines Agency. (n.d.). Medicine information and documents for calcitonin-containing products. https://www.ema.europa.eu/