ALYQ Drug Patent Profile

✉ Email this page to a colleague

Which patents cover Alyq, and what generic alternatives are available?

Alyq is a drug marketed by Teva Pharms Inc and Teva Pharms Usa and is included in two NDAs.

The generic ingredient in ALYQ is tadalafil. There are twenty-five drug master file entries for this compound. Fifty-one suppliers are listed for this compound. Additional details are available on the tadalafil profile page.

DrugPatentWatch® Litigation and Generic Entry Outlook for Alyq

A generic version of ALYQ was approved as tadalafil by TEVA PHARMS USA on May 22nd, 2018.

AI Deep Research

Questions you can ask:

- What is the 5 year forecast for ALYQ?

- What are the global sales for ALYQ?

- What is Average Wholesale Price for ALYQ?

Summary for ALYQ

| US Patents: | 0 |

| Applicants: | 2 |

| NDAs: | 2 |

| Finished Product Suppliers / Packagers: | 1 |

| Raw Ingredient (Bulk) Api Vendors: | 95 |

| Patent Applications: | 7,070 |

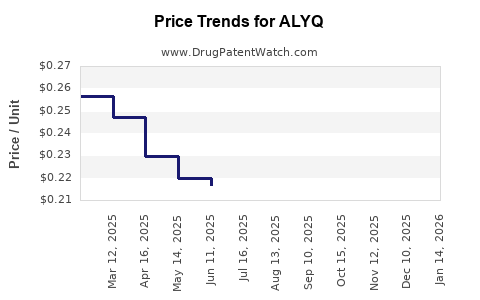

| Drug Prices: | Drug price information for ALYQ |

| DailyMed Link: | ALYQ at DailyMed |

Pharmacology for ALYQ

| Drug Class | Phosphodiesterase 5 Inhibitor |

| Mechanism of Action | Phosphodiesterase 5 Inhibitors |

US Patents and Regulatory Information for ALYQ

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Teva Pharms Inc | ALYQ | tadalafil | TABLET;ORAL | 216932-001 | Oct 12, 2022 | AB2 | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Teva Pharms Usa | ALYQ | tadalafil | TABLET;ORAL | 209942-001 | Feb 5, 2019 | AB2 | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

EU/EMA Drug Approvals for ALYQ

| Company | Drugname | Inn | Product Number / Indication | Status | Generic | Biosimilar | Orphan | Marketing Authorisation | Marketing Refusal |

|---|---|---|---|---|---|---|---|---|---|

| Viatris Limited | Talmanco (previously Tadalafil Generics) | tadalafil | EMEA/H/C/004297Talmanco is indicated in adults for the treatment of pulmonary arterial hypertension (PAH) classified as WHO functional class II and III, to improve exercise capacity. Efficacy has been shown in idiopathic PAH (IPAH) and in PAH related to collagen vascular disease. | Authorised | yes | no | no | 2017-01-09 | |

| Eli Lilly Nederland B.V. | Tadalafil Lilly | tadalafil | EMEA/H/C/004666Treatment of erectile dysfunction in adult males.In order for tadalafil to be effective, sexual stimulation is required.Tadalafil Lilly is not indicated for use by women.Treatment of the signs and symptoms of benign prostatic hyperplasia in adult males. | Authorised | no | no | no | 2017-03-22 | |

| Eli Lilly Nederland B.V. | Adcirca (previously Tadalafil Lilly) | tadalafil | EMEA/H/C/001021AdultsTreatment of pulmonary arterial hypertension (PAH) classified as WHO functional class II and III, to improve exercise capacity (see section 5.1).Efficacy has been shown in idiopathic PAH (IPAH) and in PAH related to collagen vascular disease.Paediatric populationTreatment of paediatric patients aged 2 years and above with pulmonary arterial hypertension (PAH) classified as WHO functional class II and III. | Authorised | no | no | no | 2008-10-01 | |

| Eli Lilly Nederland B.V. | Cialis | tadalafil | EMEA/H/C/000436Treatment of erectile dysfunction.In order for tadalafil to be effective, sexual stimulation is required.Cialis is not indicated for use by women. | Authorised | no | no | no | 2002-11-12 | |

| Mylan Pharmaceuticals Limited | Tadalafil Mylan | tadalafil | EMEA/H/C/003787Treatment of erectile dysfunction in adult males.In order for tadalafil to be effective, sexual stimulation is required.Tadalafil Mylan is not indicated for use by women. | Authorised | yes | no | no | 2014-11-21 | |

| >Company | >Drugname | >Inn | >Product Number / Indication | >Status | >Generic | >Biosimilar | >Orphan | >Marketing Authorisation | >Marketing Refusal |

Market Dynamics and Financial Trajectory for ALYQ

More… ↓