Last updated: April 23, 2026

How big is the disulfiram market and where does demand come from?

Disulfiram is an older, off-patent medicine used primarily for alcohol-use disorder (AUD) and, in smaller channels, for other investigational or off-label indications. Commercial dynamics for disulfiram are shaped by (1) mature supply chains, (2) low pricing power, (3) generic competition, and (4) fluctuating reimbursement coverage tied to regional prescribing patterns.

Demand drivers

- AUD pharmacotherapy adoption: Disulfiram is used when patients and clinicians prefer a deterrent-based regimen and when monitoring is feasible.

- Regulatory and formulary placement: In many markets, continued prescribing depends on state-level and payer-specific formulary lists rather than on payer-specific outcomes performance.

- Generic penetration and patient access: The drug’s economics typically track generic availability, stability of supply, and national tendering outcomes.

What does the financial trajectory look like for a generic, off-patent drug like disulfiram?

Disulfiram’s financial trajectory generally follows a mature-product pattern: revenue is stable-to-declining in price terms, while unit volumes depend on persistence of AUD use and local prescribing inertia.

Economic pattern typical for disulfiram

- Net revenue pressure: Generic pricing compresses margins and limits upside.

- Volume resilience vs. price decline: Revenue can hold if prescribing volumes remain stable, but growth is usually constrained.

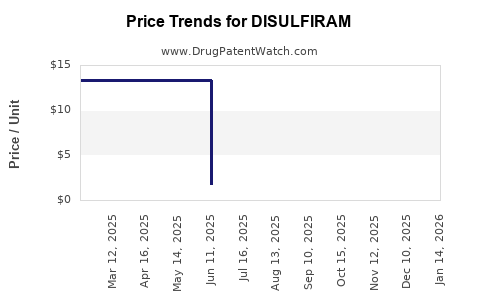

- Manufacturing and supply volatility: Periodic supply disruptions can create short-term price spikes and channel fill but rarely translate into sustained revenue growth.

Profit pool characteristics

- Low marketing leverage: With multiple competitors, prescriber pull is harder to monetize.

- Working-capital intensity: Wholesaler ordering cycles and tender schedules drive inventory swings.

- Low incremental R&D monetization: For most economics, value comes from existing supply, not from new exclusivity.

What are the key market dynamics shaping pricing and competition?

Disulfiram’s competitive set is dominated by generic manufacturers, plus originator legacy brands in some geographies. Pricing is determined less by therapeutic differentiation and more by supply availability, tender outcomes, and payer negotiations.

Market forces

- Generic substitution: Automatic substitution rules and physician switching accelerate price erosion.

- Tendering and national procurement: Public or payer-led procurement often selects lowest-cost sources and can shift share quickly.

- Formulation and packaging variants: Tablets are the dominant commercial form; pricing varies with pack size and distribution contracts more than pharmacologic differentiation.

Distribution mechanics

- Hospital vs. retail: In many systems, AUD prescribing is handled through outpatient channels, so retail reimbursement policies materially affect throughput.

- Wholesaler inventory management: Limited product diversity in certain regions can make supply constraints more impactful than in high-competition therapeutic areas.

What do recent regulatory and labeling dynamics mean for commercial prospects?

Disulfiram is regulated as a conventional small-molecule product with established safety and monitoring requirements. Commercial outlooks tend to track:

- Black box or strong warning relevance: Patient selection and adherence requirements can limit eligible prescribers.

- Interaction and toxicity monitoring: Clinician comfort affects prescribing rates.

- Support for approved indications: Where regulators or professional bodies emphasize AUD deterrent therapy, prescribing persists; where they shift practice patterns toward other AUD pharmacotherapies, disulfiram volumes can stagnate.

How do payer coverage and utilization patterns affect revenue?

Payer coverage is a primary determinant of transactional demand. For older, inexpensive therapies, payers often treat disulfiram as a cost-containment line item.

Typical coverage outcomes

- Broad formulary access: Many payers allow disulfiram without prior authorization.

- Copay and adherence friction: Even when coverage is broad, adherence and monitoring requirements can reduce effective utilization.

- Comparative therapy competition: Where payers steer to newer agents with outcomes evidence, disulfiram demand can face structural headwinds.

What is the financial trajectory under realistic supply and price scenarios?

Given the off-patent status, the most realistic “trajectory” is a combination of:

1) mild unit-volume changes,

2) pricing compression with periodic stabilization during supply constraints,

3) share shifts driven by manufacturer availability and tender wins.

Scenario map (directional)

- Base case: Flat-to-low single-digit revenue changes driven by volume stability and ongoing price pressure.

- Supply tightness: Temporary revenue acceleration from higher net prices and channel fill.

- Tender re-competition: Revenue declines when lowest-cost suppliers expand volume and prices reset downward.

What are the major competitor dynamics that matter commercially?

In AUD pharmacotherapy, disulfiram is often compared with other options (including agents with different mechanisms). Commercially, the competitive set is defined by:

- Clinical preference and guideline alignment

- Payer incentives for formulary hierarchy

- Safety profile tolerance and required monitoring

Competitive implications for disulfiram

- Mechanism competition: When clinicians prefer naltrexone or acamprosate-like approaches, disulfiram faces utilization displacement.

- Monitoring burden competition: Disulfiram requires adherence discipline and patient selection; that limits eligible population.

- Generic price competition: Within disulfiram itself, revenue capture is a function of contract execution and distribution scale.

Who captures value in the disulfiram ecosystem?

Value capture typically sits with manufacturers that have:

- consistent supply

- strong contracting in local tenders

- broad distribution reach

- low-cost manufacturing and packaging efficiencies

Publicly traded exposure

- In practice, disulfiram is generally not a standalone financial driver for major pharma; it is a small-line product for generic and specialty distributors unless a particular geography has concentrated supply or a shortage event.

What financial KPIs track disulfiram performance?

The most decision-relevant metrics for disulfiram commercial planning are:

- Net sales by geography: tracks tender and formulary coverage

- Share of supply in tender events: captures price and volume capture mechanics

- Gross margin by manufacturer: reflects input costs and competitive price reset cycles

- Channel inventory and days-on-hand: indicates stocking and replenishment risk

- Dispensed units: correlates directly with prescribing persistence

Is disulfiram being used in ways that could change market size?

Beyond AUD, disulfiram has long-standing interest in other therapeutic areas through repurposing research and onco-related investigational models. However, in a mature commercial product, such pipeline work rarely changes near-term revenue unless it produces a new regulatory approval and exclusivity.

Near-term commercialization reality

- Without a new approved indication, disulfiram’s commercial trajectory remains dominated by AUD utilization.

- Repurposing work can influence scientific and prescribing perception, but it typically does not reprice the market unless it reaches an approved, reimbursed therapy category.

Key Takeaways

- Disulfiram is a mature, largely off-patent generic product, so market outcomes are driven by tender outcomes, supply continuity, and formulary placement rather than differentiation.

- The financial trajectory typically shows price compression offset by volume stability; upside occurs mainly during supply constraints or favorable local contracting.

- Competitive dynamics come from generic substitution within disulfiram and from therapeutic displacement in AUD from other pharmacotherapies.

- Value capture goes to manufacturers with stable supply, contracting execution, and low-cost packaging/manufacturing.

FAQs

-

Is disulfiram still sold widely as an AUD treatment?

Yes. It remains available in multiple markets as an established deterrent therapy for alcohol-use disorder.

-

What drives disulfiram pricing the most?

Generic substitution and procurement/tender price resets are the dominant drivers, with supply constraints able to cause short-term price spikes.

-

Can new research on disulfiram increase revenue without new approvals?

In practice, not materially. Revenue change usually requires a new labeled indication with reimbursement support.

-

How does disulfiram compete against other AUD medications?

It competes on patient selection and monitoring feasibility; when prescribers and payers prefer other mechanisms, disulfiram utilization can decline.

-

What KPI best indicates disulfiram commercial health?

Disclosed best-practice KPI is dispensed units (or prescriptions) by geography, paired with tender/contract share to explain price and volume swings.

References

[1] World Health Organization. WHO Model List of Essential Medicines. WHO. (Accessed via WHOLIS repository). https://list.essentialmedicines.org/

[2] U.S. National Library of Medicine. Disulfiram Drug Information (Drug Labeling/Monographs). MedlinePlus. https://medlineplus.gov/

[3] Drugs@FDA. Disulfiram approvals and labeling archive. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

[4] U.S. National Library of Medicine. DailyMed: Disulfiram labeling for marketed products. https://dailymed.nlm.nih.gov/