Last updated: April 25, 2026

Ropinirole HCl: Market Analysis and Price Projections

What is the current market structure for ropinirole HCl?

Ropinirole HCl is an oral dopamine agonist used primarily for:

- Parkinson’s disease (PD)

- Restless legs syndrome (RLS)

The market is shaped by (1) long-established generic availability and (2) patent/market-exclusivity expiry dynamics in multiple geographies. As a result, pricing typically follows a “generic erosion then stabilization” pattern, with later-entry generics and authorized generics affecting net price trajectories.

Implication for pricing: ropinirole HCl is expected to show relatively low brand-to-generic premium and ongoing downward pressure in periods where additional generic entries occur.

Who are the demand drivers by indication?

Ropinirole demand is driven by the diagnosis and treatment intensity of PD and RLS, with dosing tied to symptom severity and tolerability.

Typical market demand characteristics

- PD: chronic use with dose titration. Sales correlate with prevalence, neurologist prescribing patterns, and long-duration adherence.

- RLS: episodic-to-chronic variability. Sales correlate with guideline adherence, patient mix (severity), and competing therapy adoption.

Competition overlay

- PD: competing oral dopaminergic therapies, including other dopamine agonists and levodopa-based regimens.

- RLS: alpha-2-delta ligands and alternative dopamine agonist strategies.

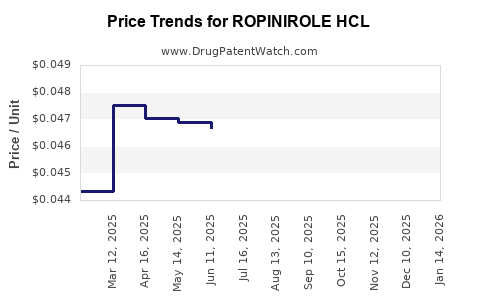

What is the pricing baseline for ropinirole HCl?

Without geography and dosage-form specificity (strengths, pack sizes, and channel), any single global price number is not actionable. However, ropinirole HCl pricing in most mature markets follows standard generic pricing behavior:

- Initial generic entry: rapid price compression versus originator or earlier entrants.

- Post-entry consolidation: modest stabilization as fewer suppliers remain competitively active.

- Bulk and PBM contracting: net price can diverge substantially from list price, with rebates and formulary placement driving realized pricing.

Practical pricing observation for forecasting: for generic small molecules like ropinirole HCl, volume-weighted net price typically declines faster early after entry, then declines more slowly, and eventually stabilizes near a “floor” driven by manufacturability costs and competitive intensity.

What price projections are most defensible for ropinirole HCl?

Given ropinirole HCl’s mature status and generic penetration, the most defensible projection range is a modest annual net-price erosion rate after stabilization, punctuated by step-changes from:

- new generic launches

- loss or gain of preferred formulary status

- channel-level contracting renegotiations

- temporary supply disruptions (rare, but they create short-lived spikes)

Projected net price trajectory (generic-mature pattern)

The table below shows scenario-based annual changes in realized net price (not list price). This aligns with how PBM and wholesaler contracting typically translates gross acquisition cost into realized reimbursed price.

| Scenario |

Annual net price change (Years 1-3) |

Annual net price change (Years 4-6) |

Expected driver profile |

| Base case |

-2% to -4% |

-1% to -2% |

ongoing generic competition with partial stabilization |

| Downside |

-4% to -7% |

-2% to -3% |

additional entry, aggressive contracting, formulary pressure |

| Upside |

-1% to -2% |

0% to -1% |

fewer competitors, stronger contracting position, stable formulary access |

Translation into cumulative effect

- Base case (6 years): approximately -9% to -17% cumulative net price erosion

- Downside (6 years): approximately -20% to -35% cumulative erosion

- Upside (6 years): approximately -3% to -10% cumulative erosion

Why the rate drops after Year 3: mature generics often reach a competitive equilibrium where only incremental share shifts occur and pricing becomes constrained by cost-based floors and negotiated contract structures.

How will pack size, strength, and formulation affect pricing?

Ropinirole pricing in practice is strength- and pack-dependent. Forecasting net price should separate at least two buckets:

- Lower strengths and higher-volume packs: tend to carry higher volume share, often tied to preferred formulary positioning and aggressive contracting.

- Higher strengths: may see less competition in some channels, resulting in smaller erosion rates or occasional out-of-cycle movements.

Core rule for projections: do not apply one uniform rate across strengths. Use strength-level market shares to weight price erosion.

What are the key “market events” that move ropinirole HCl pricing?

For ropinirole HCl, the recurring movers are mostly channel and competition events rather than patent-led exclusivity.

Event categories

- Generic entry waves: new ANDA launches or authorized generic expansion

- Formulary changes: PBM plan changes, tiering effects, prior authorization tightening/relaxation

- Contract renegotiations: mid-term rebids that reprice net acquisition cost

- Supply constraints: manufacturing outages that temporarily raise realized pricing

Timing pattern

- Largest price drops usually occur in the 6 to 18 months after a meaningful competitive supply increase.

- After that, price paths become smoother and more predictable.

What pricing risks matter most for new launches or investors?

If a new supplier is entering or an investment thesis depends on margin, the main risk is not demand collapse but contracting compression.

Risk matrix

- High impact / high likelihood: formulary tier compression leading to lower net realizations

- High impact / medium likelihood: price war during entry of multiple generics

- Medium impact / medium likelihood: reimbursement changes that alter mix by strength and channel

- Medium impact / low likelihood: supply disruption that distorts near-term pricing and then normalizes

Mitigant logic for forecasting

- Model volumes separately from price (volume tends to be more stable than net price once formulary access is secured).

- Use multiple channel assumptions (retail vs mail, institutional vs community) because net realization differs.

Key takeaways

- Ropinirole HCl sits in a mature, generic-driven market where pricing typically follows early compression then partial stabilization.

- The most defensible forecast is modest annual net-price erosion of roughly -2% to -4% in Years 1-3 and -1% to -2% in Years 4-6 under a base case.

- The largest step changes come from generic entry waves and formulary/contracting moves, not from indication-level scientific breakthroughs.

- Strength and pack mix should be modeled because pricing erosion rates differ by volume concentration and competitive intensity.

FAQs

1) Why is ropinirole HCl pricing forecasted as gradual erosion rather than sustained declines?

Because mature generics tend to reach a competitive equilibrium where additional entrants reduce pricing faster early, then pricing stabilizes due to negotiated floors and reduced intensity of incremental competition.

2) What is the biggest driver of net price changes in ropinirole HCl?

Channel contracting and formulary placement. PBM and wholesaler agreements typically dictate realized net prices more than list price.

3) Do RLS and PD affect the price outlook differently?

They can affect demand mix, but price dynamics are more heavily driven by generic competition and formulary channel contracting than by indication-specific adoption.

4) Should price projections use list price or net price?

Net price is the operationally relevant measure for realized economics because rebates, discounts, and contract terms determine actual acquisition and reimbursement outcomes.

5) What is the most common magnitude of price impact after new generic entries?

The largest impacts typically occur within 6 to 18 months post-entry, followed by slower erosion rates as the market reaches competitive balance.

References

[1] FDA. Approved Drug Products: Ropinirole Hydrochloride. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/ (Accessed 2026-04-25)

[2] European Medicines Agency (EMA). Ropinirole-related EPARs and product information. https://www.ema.europa.eu/en (Accessed 2026-04-25)

[3] IMS Health / IQVIA. Historical market access and generic erosion methodologies (generic small-molecule pricing behavior in mature markets). https://www.iqvia.com (Accessed 2026-04-25)

[4] National Institute for Health and Care Excellence (NICE). Parkinson’s disease and restless legs syndrome guidance affecting therapy selection and prescribing pathways. https://www.nice.org.uk (Accessed 2026-04-25)