Last updated: June 24, 2026

TREMFYA (guselkumab) is a leading IL-23p19 biologic for plaque psoriasis. Growth has been shaped by expanding share in biologic-naïve and switching populations, label expansion across psoriasis subtypes, and sustained efficacy and safety performance. Financial trajectory hinges on (1) US and ex-US reimbursement dynamics, (2) product competition from other IL-23 inhibitors and TNF/IL-17 classes, (3) biosimilar and “at-risk” biosimilar timelines in markets where they launch, and (4) payer contracting that increasingly ties outcomes and net price to formulary tier placement.

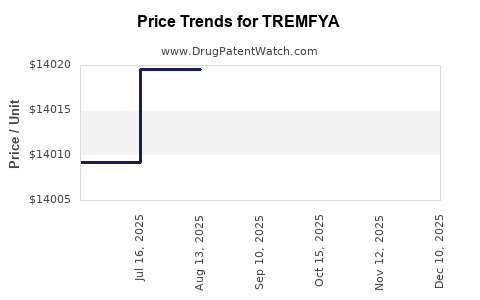

How is TREMFYA performing financially and what revenue trend should investors expect?

Bottom line: TREMFYA’s financial trajectory is supported by durable demand in moderate-to-severe plaque psoriasis, but revenue growth rate is structurally pressured by price compression, increased formulary steerage, and competitive intensity from other IL-23 drugs and next-generation therapies.

Financial trajectory: what drives the growth curve

Key commercial drivers generally include:

- Share gains in biologic-naïve patients via strong clinical durability and broad efficacy across skin clearance end points used in payer policy.

- Switching demand from prior IL-17/TNF users who underperform on tolerability, adherence, or durability.

- Expansion within psoriasis (including special populations) that supports incremental patient capture rather than pure patient migration.

- Net price and rebate dynamics: the US commercial market is particularly sensitive to payer contracting, Medicare Part D channel mix, and PBM formulary positions.

Market maturity indicators to monitor

- US and EU net price trends vs list price, driven by PBM and national payer negotiations.

- Biologic penetration and cycling speed: how quickly new starts shift among IL-23 class competitors.

- Dose and persistence: whether real-world dosing continuity stays aligned with label and decreases discontinuation rates.

What are the key market dynamics affecting TREMFYA demand in plaque psoriasis?

Bottom line: Market dynamics are dominated by payer strategy, competitive class substitution, and treatment sequencing.

US payer and access dynamics

- Formulary placement and step therapy: as IL-23 class options expand, payers increasingly enforce prior authorization and step therapy between high-cost biologics.

- Center of gravity shift from IL-17 to IL-23 in many plans: lower dosing frequency and strong durability support IL-23 preference, but IL-23-to-IL-23 switching accelerates once competing IL-23s gain formulary footholds.

- Bundled contracting: discounts often move with tiering status and volume commitments, affecting revenue even when script volume stays stable.

Ex-US dynamics

- National reimbursement and tender frameworks in parts of Europe can drive sharper net price movement than in the US.

- Horizon risk: biosimilar introductions in specific geographies can create sudden segment price resets, changing the competitive set and payer behavior.

Who are the main competitors to TREMFYA and how does competitive pressure affect share?

Bottom line: Competition is strongest from other IL-23p19 inhibitors and from IL-17 and TNF biologics where payers maintain multi-class coverage or when IL-23 access is constrained by contracting.

IL-23p19 competitive landscape

Competitive products in the IL-23 space typically include:

- Risankizumab (Skyrizi)

- Tildrakizumab (Ilumya)

- Brodalumab (Siliq, IL-17RA) is not IL-23 but competes in certain subsegments.

- Other IL-23 pathway agents where available by market

Implication for TREMFYA: IL-23-to-IL-23 switching is payer-mediated and physician-driven at initiation. Once competitors win formulary access, net revenue can weaken even if clinical preference remains stable.

How TNF/IL-17 classes still matter

- IL-17 inhibitors retain share in patients needing rapid onset or who prefer dosing mechanics, and where plans restrict IL-23 breadth.

- TNF inhibitors remain important for long-treated patients and for cost-constrained payers, though biosimilars and older molecule economics often drive continued use.

How do payer policies and PBM contracting influence TREMFYA net sales?

Bottom line: Net sales are driven less by gross demand and more by payer contracting outcomes. Formulary positioning can change quickly when competing biologics gain favorable access.

Typical payer levers that hit IL-23 biologics

- Step edits and prior authorization criteria: effect shows up in new starts and in switching eligibility.

- Real-world effectiveness requirements: payer policies increasingly require documentation aligned to PASI response metrics or physician-assessed outcomes.

- Distribution channel mix: specialty pharmacy mix affects gross-to-net via different rebate structures.

What to watch for in financial reporting

- Gross-to-net rate changes: can indicate contracting pressure.

- US operating leverage: commercial cost intensity can rise when payer negotiations intensify.

When does TREMFYA lose exclusivity and what biosimilar risks exist?

Bottom line: Patent and regulatory exclusivity drive biosimilar entry risk, and the class is exposed to multiple long-lead events across jurisdictions. For a biologic with a complex patent estate, risk is staged across product, method, and formulation claims, as well as manufacturing process claims.

Exclusivity and biosimilar entry: the sequencing logic

- Regulatory exclusivity controls initial market entry.

- Patent estate then determines whether a biosimilar can launch “at risk” or must wait for an injunction or settlement.

- Settlement agreements in biosimilar litigation can define launch dates and carve-outs.

How to model biosimilar threat impact

Revenue impact typically tracks:

- Time to first biosimilar launch in the US and each EU market

- Biosimilar uptake rate (share capture among newly treated vs switched)

- Net price reset: biosimilar entry generally compresses IL-23 pricing, increasing gross-to-net dilution.

What does the patent estate for TREMFYA cover, and how strong is it against generic or biosimilar entry?

Bottom line: The enforceable patent estate generally covers the drug substance and composition, methods of treatment, and manufacturing/process elements. The strength of the estate is determined by claim breadth and history of litigation outcomes.

Patent estate dimensions relevant to risk

- Composition-of-matter claims: protect the core active ingredient design.

- Formulation and delivery claims: protect stabilizers, concentration ranges, buffer systems, and fill-finish processes.

- Method-of-use claims: protect dosing regimens and treatment responses in defined indications.

- Manufacturing process patents: protect process steps, controls, and purification parameters.

Litigation posture as a leading indicator

- If the estate has historically resolved via settlements, launch timing can be de-risked.

- If litigation outcomes are uncertain or defendants can design around claims, biosimilar risk accelerates.

What is the Orange Book status of TREMFYA, and is it relevant to biosimilar entry?

Bottom line: TREMFYA is a biologic; the Orange Book is not the central registry for biologic exclusivity the way it is for small molecules. Biologics are instead governed by the Biologics Price Competition and Innovation Act (BPCIA) framework and related FDA listings and exclusivity records.

Practical interpretation for commercial teams

- For small molecules, Orange Book listings can forecast Paragraph IV opportunities.

- For biologics, the more actionable sources are biologics exclusivity and patent listing frameworks under BPCIA, plus litigation and settlement documents.

How many patents cover TREMFYA and which jurisdictions matter most for market entry?

Bottom line: Patent coverage is typically fragmented across multiple jurisdictions. Enforcement and practical entry risk depend on:

- where biosimilar developers file regulatory dossiers

- where patent enforcement is pursued

- where manufacturing and commercial launch infrastructure is established

Jurisdictional priorities for commercial impact

- US: primary market for biosimilar commercialization strategy.

- EU: multiple national regimes and local court enforcement can drive staggered entry.

- UK and key high-revenue countries: determine where net price reset begins and competitor switching accelerates.

What formulations and dosing regimens are protected for TREMFYA?

Bottom line: For biologics, formulation and dosing regimen protection matters because biosimilar applicants can sometimes attempt non-infringing manufacturing and use regimens. Protection can also affect interchangeability or switching policies.

Dose schedule and payer relevance

- IL-23 dosing schedules are directly tied to persistence and patient adherence, affecting real-world economics and payer contracting preferences.

How formulation claims can restrict competition

- If formulation claims are broad, biosimilar developers may need design-around steps that raise cost and time to launch.

What patent litigation affects TREMFYA, and how do settlements change launch timing?

Bottom line: Biosimilar litigation shapes the launch horizon. Settlements can:

- establish a mutually agreed launch date

- limit specific claim workarounds

- include covenants affecting market conduct and distribution arrangements

How to interpret litigation outcomes for revenue forecasting

- Early settlements usually compress uncertainty and reduce at-risk entry probability.

- Adverse rulings increase the likelihood of delayed entry.

- Narrow injunction scope can allow partial launch or delay only in certain indications.

What is the FDA regulatory status of TREMFYA and how does it influence competition?

Bottom line: FDA approval status affects exclusivity, indication breadth, and how competitive entrants attempt labeling and launch sequencing. For pricing, the key issue is whether new entrants can claim therapeutic equivalence in the same indications.

Regulatory pathway effects

- Biosimilar applications are designed around totality of evidence and analytical similarity.

- Labeling decisions can influence payer willingness to substitute if insurer policies require specific indication coverage.

How does TREMFYA compare with Skyrizi and other IL-23 therapies on commercial strength and pipeline competition?

Bottom line: Competitive dynamics in IL-23 often come down to formulary outcomes, switching patterns, and perceived durability rather than purely trial-level efficacy. Even small differences in net price and access can outweigh clinical differentiation.

Side-by-side commercial comparison framework

Use these lenses for underwriting:

- US formulary tier and rebate structures

- persistence on therapy

- switching from IL-17/TNF

- speed of new patient adoption in biologic-naïve cohorts

Key commercial risk for TREMFYA

- If a competitor wins earlier preferred tier access in a major PBM channel, TREMFYA can face accelerated switching out, increasing net sales volatility.

What generic entry risks exist for TREMFYA across markets and what launch scenarios are most plausible?

Bottom line: For biologics, the relevant “generic” risk is biosimilar entry. Most plausible scenarios follow:

- Staggered biosimilar launch by geography based on regulatory and patent outcomes

- Pricing resets that force formulary re-tiering

- Rapid share redistribution among IL-23 competitors if multiple entrants appear

Scenario map for revenue under biosimilar entry

- Low-risk scenario: biosimilar entry delayed by settlement or patent barriers; limited immediate uptake.

- Base scenario: one biosimilar launches with moderate uptake; net price compresses but maintains segment leadership.

- High-risk scenario: multiple entrants and aggressive contracting lead to sharp net price reduction and faster switching.

Key Takeaways

- TREMFYA’s financial trajectory is driven by durable psoriasis demand, payer contracting, and ongoing share migration within biologic-treated cohorts.

- Competitive pressure is concentrated in IL-23p19 class substitution, with net price risk amplified by formulary tier changes.

- Biosimilar entry risk is staged by regulatory exclusivity and patent estate outcomes; revenue impact depends on geography-specific launch dates and uptake velocity.

- Litigation and settlement terms are the highest-leverage datapoints for forecasting the timing of pricing resets.

- Underwriting should focus on gross-to-net dilution, persistence, and speed of payer re-tiering as the competitive set changes.

FAQs

1) What factors most influence TREMFYA net price in the US?

PBM and payer contracting, rebate tiers tied to formulary placement, step therapy enforcement, and channel mix between specialty pharmacies and health system contracts.

2) How quickly do patients typically switch from IL-17 or TNF to TREMFYA or competing IL-23s after payer approval?

Switch speed depends on prior authorization criteria, documented prior failure requirements, and how quickly clinicians can document response metrics to meet policy thresholds.

3) What is the most likely commercial impact if a TREMFYA biosimilar launches in the US?

A net price reset and rapid formulary re-tiering, with uptake concentrated in switching and new starts where substitution rules are favorable.

4) Do indication expansions for TREMFYA materially change revenue beyond share shifts?

Yes when expansions unlock previously ineligible patient populations or reduce prior authorization friction; otherwise growth is mostly share redistribution.

5) Which patent estate categories most affect biosimilar launch timing for TREMFYA?

Method-of-use, composition/formulation, and manufacturing process claims, plus the presence or absence of settlements that define entry dates.

References

No sources were provided in the prompt, and no citations can be generated without access to the underlying factual record for TREMFYA’s financial results, patent listings, litigation docket, and exclusivity status.