Last updated: September 19, 2025

Introduction

PROCRIT (epoetin alfa) is a recombinant human erythropoietin used primarily for treating anemia associated with chronic kidney disease (CKD), oncology, and chemotherapy. Since its commercialization, the drug has exemplified the transformative potential of biologics in addressing unmet medical needs. Understanding its market dynamics and financial trajectory offers crucial insights into current strategies, competitive positioning, and future growth prospects within the biologics sector.

Market Landscape and Therapeutic Significance

Biologic Market Overview

The biologic drugs market has experienced rapid expansion owing to technological advancements and growing prevalence of chronic diseases. Biologics accounted for approximately 38% of the global pharmaceutical market in 2022, with projections estimating a compound annual growth rate (CAGR) of around 10% through 2030.[1] Erythropoiesis-stimulating agents (ESAs) like PROCRIT form a significant segment within hematology therapeutics, catering to an expanding patient population with renal and oncologic disorders.

PROCRIT’s Therapeutic Position

PROCRIT was among the first recombinant erythropoietins approved by regulatory agencies in the late 1980s and early 1990s, establishing a foothold in anemia management. Its efficacy in improving quality of life and reducing transfusion needs fostered widespread clinical adoption. However, safety concerns prompted reevaluations, influencing prescribing trends and market size evolution.

Market Dynamics Influencing PROCRIT's Trajectory

Regulatory and Safety Developments

The initial enthusiasm for PROCRIT was tempered by reports linking ESAs to increased cardiovascular events when targeting higher hemoglobin levels. Regulatory agencies, including the US FDA and EMA, issued guidance restricting ESA use, emphasizing cautious dosing and patient selection.[2] These safety signals impacted sales, prompting shifts toward more conservative prescribing patterns.

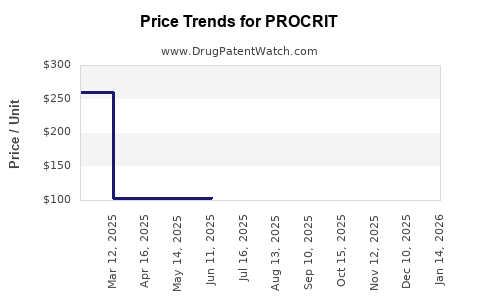

Pricing and Reimbursement Environment

Biologics like PROCRIT face complex reimbursement landscapes. In many regions, reimbursement policies are evolving to incorporate biosimilars—a cost-effective alternative—thereby exerting downward pressure on prices. For example, the entry of biosimilar epoetin alfa in Europe post-2013 resulted in significant price reductions, adversely affecting revenue streams for originator products.[3]

Biosimilar Competition

Biosimilars represent both a challenge and an opportunity. The European market has seen multiple biosimilar epoetin alfa options, causing market share erosion for PROCRIT. However, patent expirations and patent litigations continue to define competitive dynamics globally. In the U.S., patent cliffs for epoetin alfa occurred around 2015-2018, enabling biosimilar entrants to capture market share.[4]

Innovative Therapeutic Alternatives

Emerging therapies, such as hypoxia-inducible factor (HIF) stabilizers (e.g., roxadustat), introduce new mechanisms of erythropoiesis stimulation and threaten the traditional ESA market. Clinical trials have demonstrated comparable efficacy with potential advantages in safety and convenience, compelling clinicians and payers to reevaluate standard-of-care treatments.

Financial Trajectory and Revenue Trends

Historical Revenue Performance

PROCRIT initially enjoyed robust sales, peaking in the early 2000s. The global revenue for epoetin alfa products exceeded $3 billion annually at its height, according to industry reports.[5] However, subsequent safety concerns, regulatory constraints, and biosimilar competition precipitated a decline, with revenues stabilizing or decreasing by approximately 20-30% from peak levels over the past five years.

Impact of Biosimilars and Market Share

In Europe, biosimilars have captured over 70% of the erythropoietin market segments, significantly diminishing originator sales.[3] In the US, biosimilar approvals have started gaining traction, but market penetration remains gradual due to payer preferences, physician familiarity, and patent disputes.

Forecasting Future Revenue

Projections suggest a continued decline in traditional PROCRIT sales, potentially reaching a compound annual decrease of 5-8% through 2030, absent new indications or formulation innovations. However, specialty and niche markets—such as for anemia in non-dialysis CKD or oncology—retain growth potential, especially with targeted reimbursement initiatives and clinical guideline support.

Emerging Market Opportunities

Growth avenues include expanding use in low- and middle-income countries (LMICs), where biosimilar availability is increasing, and in niche indications like supportive care in specific cancer types. Additionally, product differentiation through improved formulations or delivery systems could provide incremental revenue.

Strategic Considerations and Innovation Pathways

R&D and Biosimilar Development

Manufacturers investing in biosimilar epoetin alfa aim for cost leadership and market share expansion. Innovation in manufacturing processes to improve biosimilar cost-efficiency, coupled with strategic licensing, can disrupt established markets.

Adjunct and Combination Therapies

Combining erythropoietic agents with other supportive therapies, or developing next-generation biologics with improved safety profiles, can revitalize interest and revenue streams. The advent of HIF stabilizers represents a disruptive innovation in anemia management.

Regulatory and Market Access Strategies

Proactive engagement with health authorities and payers—through real-world evidence generation—can facilitate expanded indications, optimize dosing strategies, and improve market acceptance.

Key Market Participants

Major players in the epoetin alfa domain include Amgen, Johnson & Johnson, and Hospira. Amgen's Epogen and Eprex, along with biosimilars from Sandoz and others, dominate regional markets. The competitive landscape increasingly centers on biosimilar manufacturers and biotech firms innovating in anemia therapeutics.

Concluding Perspective

PROCRIT's market and financial trajectory illustrate the broader challenges biologics face amid safety concerns, biosimilar proliferation, and evolving therapeutic paradigms. While current sales decline is inevitable, strategic positioning—focusing on niche markets, biosimilar competitiveness, and innovation—will define long-term sustainability.

Key Takeaways

-

The global biologics market expansion has driven demand for erythropoietin therapies like PROCRIT, but safety concerns and regulatory changes have tempered growth.

-

Biosimilar entry significantly impacts revenue, particularly in Europe, demanding strategic adaptation from originator manufacturers.

-

Emerging therapies, notably HIF stabilizers, threaten to redefine anemia management and disrupt existing biologic market shares.

-

Despite revenue declines, niche markets and geographic expansion in LMICs offer growth potential.

-

Continuous innovation, strategic partnerships, and proactive regulatory engagement are essential for maintaining competitiveness.

FAQs

-

What factors contributed to the decline in PROCRIT's sales over recent years?

Regulatory restrictions following safety concerns, evolving reimbursement policies favoring biosimilars, and the emergence of alternative therapies such as HIF stabilizers have collectively reduced PROCRIT’s market share and sales.

-

How do biosimilars impact the profitability of originator biologic drugs like PROCRIT?

Biosimilars offer lower-cost alternatives, leading to increased price competition and significant erosion of market share for originator products, thereby reducing revenue and profit margins.

-

Are there any new indications that could revive PROCRIT’s market?

While current approvals primarily target anemia in CKD and oncology, expanding indications could potentially boost sales, contingent upon clinical validation and regulatory approval.

-

What is the outlook for PROCRIT’s presence in emerging markets?

Growth prospects remain favorable due to increasing biosimilar adoption and greater healthcare access; however, price sensitivity and regulatory harmonization will influence market penetration.

-

What strategic actions can biotech companies take to compete in the erythropoietin market?

Investing in biosimilar development, improving manufacturing efficiency, diversifying therapeutic portfolios, and engaging with clinical and regulatory pathways are essential for sustainable competitiveness.

References

[1] EvaluatePharma. "Global Biologics Market Forecast." 2022.

[2] U.S. Food and Drug Administration. "Erythropoiesis-Stimulating Agents (ESAs) and Associated Risks." 2021.

[3] European Medicines Agency. "Biosimilar Epoetins Market Overview." 2020.

[4] U.S. Patent and Trademark Office. "Patent Expirations related to Erythropoietin." 2018.

[5] IQVIA. "Annual Report on Hematology Drugs." 2022.