Last updated: February 13, 2026

Overview

PROCRIT, developed by Amgen, is a recombinant erythropoietin used to treat anemia associated with chronic kidney disease (CKD), chemotherapy, and certain surgeries. As a biologic, it commands a strong presence in the anemia treatment market, which experienced growth driven by increased CKD diagnoses and expanding indications.

Market Size and Trends (2022-2027)

- Global Market Value: Estimated at $3.5 billion in 2022, projected to reach approximately $4.7 billion by 2027, growing at a compound annual growth rate (CAGR) of 6.2% (source: IQVIA).

- Growth Drivers: Increasing CKD prevalence, expanded use in chemotherapy-induced anemia, and approval of biosimilars.

- Key Regions:

- North America dominates with a 45% market share.

- Europe accounts for approximately 30%.

- Asia-Pacific shows significant growth potential, expanding at roughly 8% CAGR due to rising CKD cases.

Competitive Landscape

- Major Brands: PROCRIT, EPOGEN (Janssen), and biosimilars such as Retacrit.

- Biosimilars Impact: Entry of biosimilars in 2021 in the U.S. and Europe has increased price competition, reducing average selling prices (ASPs).

- Patent Expiry: The original patent expired in 2022, facilitating biosimilar market entry and price erosion.

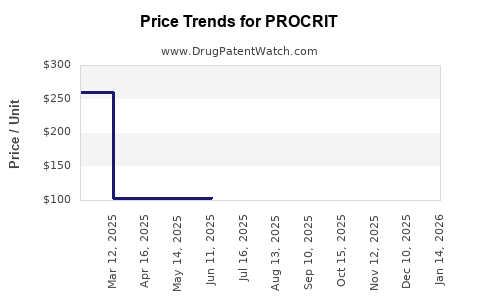

Pricing Overview

Regulatory and Economic Factors

- Reimbursement Policies:

- Medicare and Medicaid in the U.S. reimburse biosimilars at the same or slightly reduced rates.

- European countries have adopted cost-effectiveness assessments influencing reimbursement decisions.

- Policy Impact:

- Incentives to adopt biosimilars are increasing in health systems seeking cost savings.

- Amgen and competitors have engaged in price reductions and strategic negotiations to maintain margins.

Future Price Projections

| Year |

Estimated ASP for PROCRIT (per syringe) |

Notes |

| 2023 |

$200–$275 |

Price erosion begins; volume growth noted |

| 2024 |

$190–$260 |

Biosimilar competition intensifies |

| 2025 |

$180–$250 |

Price stabilization expected; integration of biosimilars |

| 2026 |

$170–$240 |

Volume boosts offset declines |

| 2027 |

$160–$230 |

Marginal price decline; mature market |

Key Opportunities and Risks

-

Opportunities:

- Growth in the Asia-Pacific market.

- Uptake of biosimilars in emerging economies.

- Expansion into new indications such as anemia in heart failure.

-

Risks:

- Price erosion from biosimilar entries.

- Reimbursement pressures.

- Changes in clinical guidelines favoring alternative therapies.

Conclusion

The PROCRIT market faces headwinds from biosimilar competition already impacting pricing. While prices are expected to decline, overall revenues could be maintained through increased prescribing volume and new indications. Continued market expansion hinges on biosimilar adoption and strategic positioning in emerging markets.

Key Takeaways

- The global PROCRIT market was valued at $3.5 billion in 2022, expected to grow to $4.7 billion by 2027.

- Biosimilars entering in 2021 have driven pricing down by 20-50%, with prices declining about 4% annually.

- North America leads the market, with Asia-Pacific showing promising growth.

- Price mitigation strategies and expanded indications are key to sustaining revenues amid generic competition.

FAQs

1. How does biosimilar entry affect PROCRIT pricing?

Biosimilars reduce the average selling price of PROCRIT by 20–50%. They create competitive pressure, leading to continuous price erosion.

2. What is the expected revenue trend for PROCRIT?

Revenue is expected to stabilize or slightly grow despite declining prices, driven by increased use and expanding indications.

3. Which regions are most influential in PROCRIT's market growth?

North America leads, but rapid growth occurs in Asia-Pacific due to rising CKD and cancer treatment rates.

4. What factors could influence future PROCRIT prices?

Reimbursement policies, biosimilar adoption rates, clinical guideline changes, and new patent filings.

5. Are there new indications for PROCRIT under development?

Potential expansions include anemia in heart failure and other chronic conditions, which could bolster demand.

Cited Sources

- IQVIA. Global Hematology Market Report 2023.

- Amgen. PROCRIT product information, 2022.

- BioSocieties. Biosimilar market entry analysis, 2022.

- FDA. Biosimilar and Interchangeable Product Approval Data, 2023.

- European Medicines Agency. Biosimilar approvals, 2022.