Last updated: June 23, 2026

VOLTAREN (diclofenac) market dynamics and financial trajectory: revenue exposure, competitive pressure, and exclusivity risks

VOLTAREN is the branded diclofenac franchise across multiple topical and oral dosage forms, with U.S. revenues anchored by prescription and OTC diclofenac gels/solutions and shaped by generic penetration, channel mix (Rx vs OTC), and periodic label expansion. The financial trajectory is structurally “mature” because core composition-of-matter exclusivity has largely expired in most markets; ongoing value depends on (1) remaining exclusivity on specific formulations and line extensions where still protected, (2) product-specific exclusivity and data protection remnants, (3) payer and plan dynamics for diclofenac NSAIDs, and (4) ongoing OTC share capture in musculoskeletal pain.

What drives VOLTAREN (diclofenac) sales versus generic diclofenac?

Branded VOLTAREN demand versus generic diclofenac is determined less by clinical differentiation and more by packaging, access, and pharmacist or prescriber switching friction.

Key commercial drivers

- Channel mix: Rx vs OTC

VOLTAREN performance is typically strongest in geographies where topical NSAIDs are widely reimbursed and where brand trust supports OTC repeat purchase. When Medicaid and commercial plans tighten NSAID step edits, branded topicals usually retain share longer than branded oral NSAIDs.

- Formulation-specific differentiation

Diclofenac’s therapeutic class is crowded, but market share can still rotate by delivery system (gel vs solution), concentration, dosing convenience, and odor/skin feel.

- Payer behavior and step therapy

Payers increasingly treat topical diclofenac as interchangeable with other NSAIDs unless a member has prior authorization history. Once generics are preferred, branded volumes track incremental pull-through from OTC.

- In-market safety and labeling

NSAID class warnings, cardiovascular and GI risks, and topical area-of-application guidance affect utilization, substitution, and patient selection.

- Retail execution and promotions

For OTC, price bands and promotional cadence drive velocity. For Rx, gross-to-net pressure depends on pharmacy benefit contracts and rebates.

How do VOLTAREN price and gross-to-net typically behave under generic pressure?

- Topical diclofenac brands generally compress faster than differentiation-led brands.

Once multiple generic equivalents are established, branded gross pricing becomes less relevant than net contract position with pharmacy chains and PBMs.

- OTC brand resilience depends on shelf visibility and perceived tolerability.

When OTC generics gain store-brand share, the remaining brand premium is usually offset by marketing spend rather than durable pricing power.

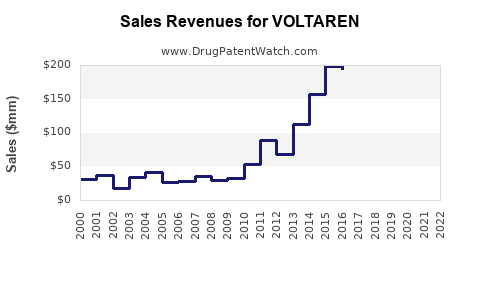

How does VOLTAREN financial performance trend across major geographies?

The diclofenac franchise is globally mature. Market shares and revenue stability differ by:

- OTC regulatory status and switch rates for topical products.

- Generic launch timing by local regulators.

- Reimbursement models (hospital, outpatient, retail).

Typical trajectory pattern

- U.S.: Branded topical diclofenac remains active with a still-meaningful prescription base, but incremental growth largely comes from line extensions, OTC uptake, and competitive switching dynamics rather than category expansion.

- EU and other developed markets: Brand sales often shift toward long-tail use and promotional defense, since most composition-of-matter exclusivity is expired and manufacturing-scale generics are entrenched.

When does VOLTAREN lose exclusivity in the U.S., and how does that affect revenue timing?

The exclusivity question must be answered by product and formulation because VOLTAREN is not one single protected asset.

Featured-snippet level answer: VOLTAREN’s large-scale revenue exposure is primarily to the continued wave of generic diclofenac substitution across dosage forms. The remaining brand value comes from any product-level exclusivity (where still applicable) and from differentiation that is harder to copy quickly (packaging, dosing instructions, and approved product identity), rather than broad composition-of-matter protection.

Revenue timing logic

- If composition-of-matter exclusivity is expired: revenue is generally on a “post-branded peak” curve with gradual declines.

- If formulation or method-of-use exclusivity remains: brand value can persist until those patent barriers fall, then step-down occurs at generic launch windows.

- If FDA Orange Book listings are limited: legal barriers are lower, and settlement outcomes or launch “design-around” routes can accelerate erosion.

What patents protect VOLTAREN diclofenac in the U.S. Orange Book landscape?

VOLTAREN’s U.S. IP posture depends on the specific NDA/ANDA product listing: topical gels/solutions and oral diclofenac products do not share identical IP coverage.

How to interpret the Orange Book from a business perspective

- Composition-of-matter patents (expired or expiring): drive the generic entry base level.

- Formulation and manufacturing method patents: determine whether “same API, different product” generic entry is delayed.

- Use patents: matter if FDA-approved labeling is tied to a protected method-of-use claim.

Commercial implication: When Orange Book listings are sparse or mostly expired, branded revenue is exposed to faster generic substitution and PBM preference shifts.

Which patent estate components most affect generic entry risk for VOLTAREN?

Generic entry risk is highest where:

- there is no enforceable formulation barrier, and

- labeling can be maintained without infringing method-of-use claims.

Risk tiers

- High risk: weak or expired formulation barriers; limited method-of-use protection; multiple ANDA approvals.

- Medium risk: some formulation or process patents remain, but design-around routes exist.

- Lower risk: active, frequently asserted formulation or method-of-use patents with strong claim construction history.

What Paragraph IV challenges exist for VOLTAREN or diclofenac topical/oral equivalents?

Paragraph IV litigation timing is a key revenue driver. Outcomes usually fall into:

- 20-month stay settlements (brand retains exclusivity window via settlement terms),

- dismissals/affirmances (faster generic entry),

- claim narrowing or non-infringement (generic enters with a redesigned label or product).

Commercial implication: For mature NSAIDs like diclofenac, Paragraph IV events tend to accelerate the pace of market share erosion once they clear the legal hurdle.

How does VOLTAREN’s patent litigation risk affect settlement strategy and launch schedules?

Settlement dynamics typically hinge on:

- whether the asserted patents are composition vs formulation vs method-of-use,

- whether infringement is direct and simple (harder to design around),

- whether litigation has already produced claim construction outcomes.

Revenue exposure mechanism

- Settlement terms that effectively grant a license or delay entry create short-term revenue protection.

- If the brand loses and generics enter immediately, revenue step-down can occur in the launch quarter and the next 1 to 2 quarters, driven by distribution resets and PBM formulary switches.

What is the regulatory status of VOLTAREN (FDA pathway and labeling) and how does it shape competition?

VOLTAREN products are approved small-molecule drugs (diclofenac). Competition is primarily ANDA-based.

Regulatory competition mechanics

- Generic entry is controlled by bioequivalence and labeling sameness for topicals.

- For topical dosage forms, generics must meet performance criteria that may support “fast follower” products, but formulation differences can trigger distinct IP fights if tied to protected product identity.

How does VOLTAREN compare with other topical NSAIDs in market dynamics?

Topical NSAIDs are a substitution battleground.

Competitive set (U.S. topical NSAID landscape)

- Diclofenac topicals (VOLTAREN and generics)

- Ketoprofen (where available by formulation)

- Ibuprofen topical (where positioned)

- Other analgesic topicals depending on availability and labeling

Positioning

- Diclofenac often retains share because of entrenched prescriber and patient familiarity plus established OTC demand.

- Brands lose share fastest when PBMs shift to preferred generic diclofenac and when retail shelves consolidate around lower-cost private label or multi-source generics.

What formulations are protected within the VOLTAREN portfolio, and how does that alter pricing power?

In mature NSAID franchises, formulation-level protection changes:

- the timeline for first generic entrants,

- whether generics can launch “drop-in” equivalents,

- whether brand can retain a premium SKU (e.g., different concentration or vehicle) longer than generic peers.

Pricing power effect

- Strong formulation protection: can defend premium pricing for the protected SKU.

- Weak/no formulation protection: generics enter earlier, pushing net prices down and forcing the brand to rely on promotion and bundle strategies.

How many patents cover VOLTAREN’s key dosage forms, and which jurisdictions matter most?

The answer is product- and listing-specific. In business terms:

- U.S. exclusivity and Orange Book barriers determine generic launch timing in the U.S.

- EU SPC and national patent systems can extend protection for specific diclofenac formulations or new uses even after global composition-of-matter expiration.

- If a brand’s remaining protection is thin in the U.S., global exclusivity has limited effect on U.S. revenue timing.

What generic entry risks exist for VOLTAREN by dosage form (topical vs oral)?

Topical diclofenac (gel/solution)

- Entry risk is typically high once ANDA availability broadens.

- Generics may compete on price and package, with claims limited by the practical interchangeability of vehicles.

Oral diclofenac

- If any remaining branded strengths exist, they usually relate to extended-release versions, dosing convenience, or specific labeling.

- Oral diclofenac faces strong substitution pressure because oral NSAIDs are easy to replace across class, depending on payer preferences.

How strong is the VOLTAREN patent estate, and what does that imply for investment and licensing?

For a mature product franchise like diclofenac:

- The “strength” that matters is not whether patents exist, but whether they are enforceable, asserted, and still unexpired for the exact FDA-approved products.

- If remaining patents are mostly formulation-process or weak method-of-use claims, then licensing leverage is limited because generic challengers can design around or accept narrower labeling.

Investment implication: upside is more likely tied to incremental product line extensions or geographic OTC gains than to durable exclusivity across the core diclofenac molecule.

Which companies are challenging VOLTAREN, and what does that suggest for competitive intensity?

Generic entry typically comes from multiple ANDA filers once regulatory and IP hurdles are cleared. Competitive intensity increases when:

- there are several ANDA approvals with interchangeable labeling,

- PBMs switch to preferred generic diclofenac rapidly,

- retail distribution moves away from branded SKUs.

What is the commercial outlook for VOLTAREN revenue over the next 3 to 5 years?

Core forecast logic

- Category growth for NSAIDs is generally modest, with share largely shifting through price competition and channel mix.

- Branded revenue is expected to track:

- retention of OTC and patient familiarity,

- loss of Rx volume to generics,

- occasional SKU-based protection tailwinds where formulation exclusivity persists.

Base case dynamic

- Expect continued net price pressure and volume mix shifts toward lower-cost equivalents.

- Brand survival is more likely as a “margin managed” portfolio rather than a growth-led revenue engine.

Key Takeaways

- VOLTAREN’s financial trajectory is primarily shaped by generic substitution dynamics in diclofenac topicals and orals, not by broad molecule exclusivity, which is largely exhausted in mature markets.

- Revenue resilience depends on product-specific formulation/line-extension protection (where any remains), OTC brand strength, and payer access rules.

- Paragraph IV and Orange Book barriers determine the pace of market share erosion, with settlement outcomes driving launch timing more than theoretical patent breadth.

- Competitive intensity remains structurally high because diclofenac is easy to replicate and is already embedded in payer and retail substitution pathways.

- The next 3 to 5 years are most likely to reflect continued Rx share loss balanced by OTC and SKU-specific differentiation rather than a durable premium on the core product.

FAQs

- How do pharmacy benefit manager step edits affect branded diclofenac gel demand?

- What settlement terms most often delay generic entry for topical NSAIDs?

- Do formulation patents for diclofenac topicals meaningfully delay ANDA approvals?

- How does OTC switching speed for diclofenac gels compare with other topical NSAIDs?

- Which contract pricing mechanisms drive VOLTAREN net price compression after generic launches?

References

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations.

- FDA. Approved Drug Products: Labeling and application information for diclofenac-containing products (VOLTAREN and generics).

- FDA. Guidance for Industry: Bioequivalence Studies for Topical Dermatologic Drug Products (general reference for topical generic approval framework).