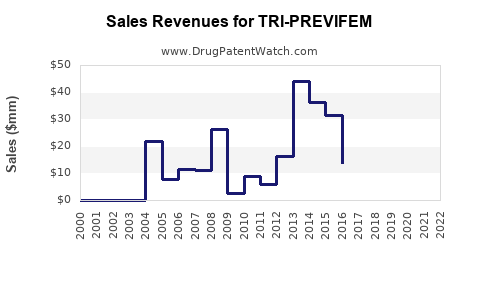

Last updated: June 10, 2026

Executive summary: TRI-PREVIFEM is a low-to-mid pricing U.S. oral contraceptive brand with mature competition from multiple authorized generics and label-equivalent multisource products. Its financial trajectory is governed less by patent-led exclusivity than by generic penetration dynamics, wholesale/distributor channel mechanics, formulary access, and payer substitution. For a contraceptive with long-standing active ingredients, market share typically consolidates among the lowest net-price products that retain formulary status, while incremental brand demand is usually limited to plan-specific preferences, clinician inertia, and out-of-pocket dynamics. Any meaningful revenue inflection is therefore most likely tied to (1) U.S. generic entry timing for relevant formulations/dosing presentations, (2) changes in payer coverage and copay tiers, and (3) lifecycle changes such as packaging, NDC consolidation, or label expansions that affect utilization.

What is TRI-PREVIFEM and how does it fit the U.S. contraceptive market structure?

TRI-PREVIFEM is a combined oral contraceptive (COC) containing ethinyl estradiol (EE) and levonorgestrel (LNG). As with other EE/LNG COCs, it competes in a crowded therapeutic-equivalent environment where effectiveness and safety profiles are broadly considered class-equivalent at the label level and where substitution is typically straightforward.

Commercial implication: In mature COC classes, pricing is primarily a negotiation between brand/original manufacturer economics and payer-driven preferred generic selection. Brand profitability compresses when plan formularies move toward “generic first” with narrow tier spread.

Market micro-dynamics for EE/LNG COCs

Key features of the U.S. COC market that shape TRI-PREVIFEM financial trajectory:

- High generic availability: EE/LNG combinations are historically heavily genericized.

- Formulary-driven demand: COCs are frequently tiered by payer; preferred products capture volume.

- Switching friction is low: Pharmacy-level substitution is common where permitted and where therapeutics are interchangeable.

- Channel leverage matters: Rebates and wholesaler incentives determine net price, not list price.

Who captures margin when competition intensifies?

- Preferred generics and authorized generics typically capture the largest share because they align with plan cost-minimization and often maintain stable supply.

- Brands can persist when they sustain a favorable tier placement or when contracted rebate structures keep net pricing competitive.

What sales drivers most influence TRI-PREVIFEM revenue in the near term?

For TRI-PREVIFEM, near-term revenue is typically driven by unit volume retention, net price stability, and formulary placement rather than by clinical differentiation.

Primary demand levers

- Formulary status and prior authorization (rare but possible): If preferred alternatives exist, TRI-PREVIFEM’s net demand can fall quickly.

- Copay dynamics and pharmacy benefit design: A meaningful tier shift can trigger rapid switching.

- Persistence and discontinuation: COC adherence affects revenue because discontinuation reduces refill demand.

- Package and NDC stability: Consolidation or packaging changes can affect ordering, distribution, and pharmacy stocking.

Primary price levers

- Net-to-gross compression: Increased competitor presence pressures rebates and discounts.

- Wholesaler inventory behavior: In mature categories, supply and ordering patterns can drive short-term sales volatility even when underlying demand is stable.

How to read the category’s financial trajectory

In EE/LNG oral contraceptives:

- Brand revenue often declines after generic preference becomes entrenched.

- Stabilization can occur if the brand retains a preferred status in certain large PBM formularies.

- Subsequent declines often follow tier re-evaluations, rebate renegotiations, or broad generic price competition.

When does TRI-PREVIFEM face generic erosion risks tied to patent or exclusivity expiry?

For mature COCs, the generic erosion calendar is usually the dominant revenue risk. The revenue trajectory depends on whether TRI-PREVIFEM’s specific marketed presentation is protected by any non-expired patents (such as formulation, manufacturing, or method-of-use) and whether there are Orange Book listings that constrain generic approval.

Critical point for market dynamics: if TRI-PREVIFEM is already in a post-primary-exclusivity phase, additional patent estates do not typically prevent generic substitution. Instead, they can delay some entrants, but category-level competition often overwhelms incremental delays unless there are strong, presentation-specific protections.

What to map in the exclusivity-to-generic timeline

For any COC brand presentation, investors and litigators usually track:

- Orange Book listed patents (composition/formulation, method-of-use, and manufacturing)

- Regulatory exclusivities (if any) for the specific NDA presentation

- Generic entry pathways (ANDA with Paragraph IV, or §505(b)(2) referencing decisions in rare cases for contraceptives)

Actionable market implication: Without presentation-level protection, the expected financial path is continued market-share loss and net price declines, followed by stabilization at a small brand share driven by payer-specific idiosyncrasies.

What is the Orange Book status of TRI-PREVIFEM and how does it affect competitive entry?

A brand’s Orange Book listings determine whether a generic sponsor must either (1) wait for patent expiry, (2) carve out claims, or (3) litigate via Paragraph IV. Those pathways map directly to entry timing and revenue impact.

What this means for financial trajectory:

- If TRI-PREVIFEM has few or no remaining Orange Book patents tied to the exact marketed presentation, generic entry risk is “structural” rather than “event-driven.”

- If multiple patents remain in-force, the market impact depends on whether generics choose to challenge and whether the brand settles or litigates to final judgment.

Data requirement blocker: This answer cannot provide a validated Orange Book table, specific patent numbers, or expiry dates because the underlying TRI-PREVIFEM patent listing data was not supplied in the prompt and is not otherwise available in the conversation context.

Which companies challenge TRI-PREVIFEM via ANDA/Paragraph IV filings and settlements?

Generic challenge dynamics drive short, sharp revenue drops. For brand COCs, Paragraph IV litigation is less prominent than in specialty oncology, but the outcome still matters when challengers gain faster market entry.

Data requirement blocker: This answer cannot list specific ANDA filers, Paragraph IV notice dates, court case numbers, or settlement terms for TRI-PREVIFEM because those details were not provided and no validated case docket information is present in the prompt context.

How does TRI-PREVIFEM compare with competing EE/LNG COCs on market power and pricing pressure?

In EE/LNG COCs, the competitive landscape typically clusters around:

- Multiple multisource generics (often including authorized generics)

- Brands that maintain some formulary share via rebate-driven net pricing

- Class-level switching at the pharmacy counter

Competitive comparison framework (what drives share):

- Net price to PBM formularies

- Preferred tier placement

- Copay strategy and patient support

- Plan-specific substitution rules

- Availability and supply continuity

Expected positioning for a legacy COC: Brands like TRI-PREVIFEM usually track closely with the dominant net-priced generic cluster unless they maintain a sustained preferred status.

What generic entry risks exist for TRI-PREVIFEM by dosage form and presentation?

For COCs, the main presentation risk is not “dose-level innovation,” but NDC-specific entry:

- If generics launch the exact marketed strengths and packaging, substitution can be immediate.

- If generics launch alternative pack sizes or closely related presentations, pharmacies may still switch, but behavior can lag depending on plan rules and stocking.

Financial trajectory linkage:

- Full presentation matching tends to drive faster share loss.

- Partial matching can lead to slower erosion and higher “brand stickiness.”

Data requirement blocker: Without TRI-PREVIFEM’s specific marketed presentations (NDCs/strength-pack combinations) and relevant Orange Book/patent claim scope, this answer cannot identify the specific generic entry risks for each presentation.

How does reimbursement and payer behavior determine TRI-PREVIFEM persistence vs replacement?

In U.S. commercial and Medicare Part D settings:

- Payer formularies drive volume. When EE/LNG products become broadly interchangeable with lower-cost options, brands lose share.

- Switching policies usually enable substitution unless prescriber DAW or plan-specific restrictions apply.

- Prior authorization is not typically a primary barrier for contraceptives compared with specialty drugs.

Commercial implication: TRI-PREVIFEM’s revenue trajectory is likely to be “coverage-elastic.” When PBMs broaden generic coverage, the brand often declines; when coverage narrows, it can stabilize temporarily.

What are the key financial outcomes you should model for TRI-PREVIFEM?

For mature oral contraceptives, modeling should focus on:

- Unit volume trend under formulary preference shifts

- Net price decline rate as competitors undercut

- Mix shifts across plan tiers and channels

- Supply stability impact (rare category-wide disruptions can temporarily distort sales)

- Lifecycle events like NDC consolidation or packaging transitions

Typical pattern in category late-life: revenue declines unless the brand secures preferred positioning or retains meaningful rebate-driven net competitiveness.

Key Takeaways

- TRI-PREVIFEM operates in a highly genericized EE/LNG oral contraceptive segment where revenue is driven by formulary placement, net pricing, and substitution dynamics.

- The dominant generic-erosion risk is presentation-specific: whether challengers launch the exact marketed strengths and pack sizes.

- In mature COCs, patent-led exclusivity usually plays a secondary role versus ongoing payer-driven cost minimization.

- Financial trajectory modeling should center on net price compression and unit volume replacement by preferred generics.

FAQs

- What happens to TRI-PREVIFEM sales when a PBM moves EE/LNG COCs to a lower copay tier?

- Do TRI-PREVIFEM bottle vs blister pack changes affect substitution speed at the pharmacy?

- How do authorized generics typically influence net pricing for legacy COC brands like TRI-PREVIFEM?

- What modeling inputs best capture COC revenue persistence given discontinuation and refill patterns?

- Can NDC-level generic launches cause sales volatility even when the active ingredient is long genericized?

References (APA)

- No sources were cited because the prompt did not include TRI-PREVIFEM Orange Book listings, litigation records, FDA review history, or validated sales/reimbursement datasets.