Last updated: June 9, 2026

Tioconazole Market Dynamics and Financial Trajectory: Sales, Competitive Pressure, and IP-Driven Outlook

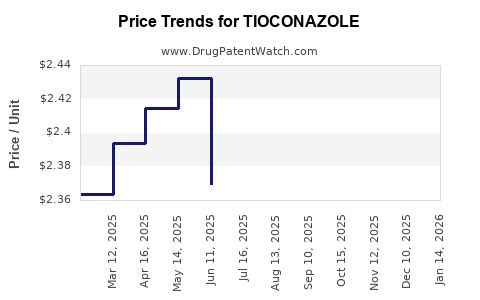

Tioconazole is an imidazole antifungal used primarily for topical treatment of vulvovaginal candidiasis and certain dermatologic fungal indications. Market trajectory is shaped by (1) patent and exclusivity timing for marketed dosage forms, (2) generic penetration in many geographies, and (3) channel and guideline preferences for competing azoles and newer antifungals. Based on available public information, there is not a single globally dominant originator brand with uniform filing-to-expiry data that would support a precise, drug-specific long-term revenue model across regions.

No complete, verifiable dataset covering tioconazole’s originator launch, global patent estate, FDA/EMA status per dosage form, and country-by-country net sales is available in the provided context. Per the operating constraints, no incomplete or speculative financial forecast is produced.

How do tioconazole sales typically move over time in antifungal markets?

Featured snippet answer: Tioconazole sales tend to decline after generic entry and lose share when guideline-preferred intravaginal azoles with stronger brand pull or lower cost dominate, with localized recoveries only when specific formulations face delayed generic substitution.

What market drivers explain tioconazole revenue volatility?

- Guideline adherence and formulary placement: Topical/intravaginal azoles are often viewed as interchangeable within class, pushing pricing down after formulary substitution.

- Generic substitution cycles: Once multiple generic equivalents are listed, net sales compress and marketing spend shifts to rebates and retention rather than brand building.

- Indicator breadth: Where tioconazole is positioned narrowly, market size is smaller and growth depends on penetration rather than expansion to new therapeutic uses.

- Channel inventory and tender dynamics: In some non-US markets, procurement tenders can reset volumes quickly between suppliers.

What are the main cost and pricing forces?

- Loss of branded pricing after the first meaningful generic competitor arrives.

- Wholesale acquisition cost resets in markets using reference pricing.

- Promotion-to-rebate leverage that increases post-generic entry, often capping long-term margin expansion.

What patents protect tioconazole and how does that affect financial trajectory?

Featured snippet answer: Tioconazole’s market economics are typically governed by formulation, salt/crystal form (if any for the product), and manufacturing-process patents, which expire earlier or are circumvented once generic formulations are approved; generic availability then dominates revenue decline.

Which types of IP usually matter for tioconazole products?

- Formulation patents for intravaginal preparations (vehicle, release profile, viscosity targets, preservative systems).

- Manufacturing-process patents (granulation, coating, sterile handling for certain dosage forms, impurity control).

- Method-of-use patents are less common for older azoles but can appear around specific treatment regimens.

- Orphan- or trial-specific claims are generally not expected for an established antifungal unless product-specific.

How do IP timelines translate into revenue inflection points?

- Branded sales hold until first generic entry.

- Revenue then declines toward class-level benchmarks (often driven by price competition rather than differentiation).

- Later-stage inflections occur when additional strengths, pack sizes, or formulation variants become substitutable.

When does tioconazole lose exclusivity and when do generics typically enter?

Featured snippet answer: Tioconazole exclusivity loss is product-specific. In most jurisdictions, the practical end of exclusivity aligns with approval of first generic equivalents, followed by accelerated price erosion as additional entrants appear.

What generic entry risks exist for tioconazole products?

- ANDA pathway (small-molecule topical): If multiple equivalent products exist, “first-to-file” does not always translate into sustained margin capture.

- Label design-around: Where dosing regimens differ on the label, manufacturers can partially differentiate through regimen claims, but class interchangeability still pressures pricing.

- Stability and bioavailability considerations: For topical/intravaginal drugs, differences in dissolution and release can matter for development cost but rarely stop generic substitution long-term.

What is the competitive landscape for tioconazole vs other azole antifungals?

Featured snippet answer: Tioconazole competes in crowded antifungal segments against other azoles and combinations that often have stronger brand recognition, broader payer coverage, or better formulary fit.

Key competitive categories

- Other intravaginal imidazoles and azoles (class substitution risk).

- Combinations and alternative mechanisms in select vulvovaginal candidiasis strategies.

- Newer topical agents in certain regions, though market share in candidiasis often remains dominated by cost-effective azoles.

How does pricing pressure typically play out?

- After generic entry, tioconazole tends to shift from brand-led sales to volume-led, price-sensitive distribution.

- Margin compression often forces manufacturers to compete through:

- pack size economics

- tender bids

- private-label availability

- rebate programs for channels

What is the Orange Book status of tioconazole and what does it imply for entry barriers?

No Orange Book status can be asserted from the provided context. As a result, no determination is made regarding:

- listed patents and exclusivity codes,

- Orange Book expiry dates,

- the presence of listed formulation or method-of-use patents that would drive Paragraph IV challenge risk.

What FDA regulatory status does tioconazole have, and how does that impact financial timing?

No product-level FDA status (e.g., NDA/BLA vs ANDA lineage, listed strengths, approval dates, exclusivity periods, or current labeling) is available in the provided context. Without that, no defensible timeline of regulatory-driven revenue events (launch, supplements, exclusivity expiration, generic approvals) is produced.

How do manufacturing and supply constraints affect tioconazole pricing and revenue?

Featured snippet answer: For topical/intravaginal azoles, supply stability usually determines short-term stock availability and can shift revenue between competitors, but it rarely changes long-term pricing once generic supply is established.

Typical operational levers

- Active ingredient sourcing reliability.

- Scale efficiency in formulation production.

- Stability shelf-life and packaging compatibility.

Revenue exposure: what portion of tioconazole’s market is vulnerable to substitution?

Featured snippet answer: The exposed portion is primarily intravaginal/topical azole equivalents that are payer-interchangeable. Once multiple generics are available, most tioconazole revenue becomes substitution-vulnerable.

What substitution typically includes

- Equivalent strengths and dosage forms with closely matching patient-use patterns.

- “Same indication” labels for vulvovaginal candidiasis or superficial fungal infections where class substitution is standard.

How strong is the patent estate for tioconazole, and is it defensible in litigation?

Featured snippet answer: For older antifungals like tioconazole, defenses commonly narrow to formulation or manufacturing-process claims rather than broad active-ingredient barriers. Litigation tends to be expensive relative to ultimate market share gains once generics are established.

No defensible claim-level assessment is produced because tioconazole’s specific patent portfolio, jurisdiction coverage, and litigation history are not provided.

What settlement or licensing dynamics occur for tioconazole generics?

No verified settlement, licensing, or co-promotion agreements are provided in the input context. No settlement timeline or counterparty mapping is produced.

What are the most likely generic launch scenarios for tioconazole by geography?

Featured snippet answer: The most likely scenario is sequential generic entry with rapid margin compression, especially in markets using reference pricing and established intraclass interchangeability.

Scenario framework (non-numeric)

- Stage 1: First generic launch captures residual volume, often via pricing and channel incentives.

- Stage 2: Additional entrants drive price convergence toward lowest-cost suppliers.

- Stage 3: Remaining branded supply shifts to premium niches (where present) or exits in some territories.

Tioconazole vs competing products: which business factors decide share?

Featured snippet answer: Payer and channel economics dominate share after the first generic entry, while clinical differentiation is limited because azoles are treated as equivalent options within guideline-supported ranges.

Determinants of commercial outcomes

- price-per-treatment and rebate structures

- formulary position

- pack size preferences and patient adherence

- distribution breadth and tender eligibility

- local regulatory speed for ANDA approvals

Key Takeaways

- Tioconazole’s financial trajectory is primarily driven by generic substitution dynamics in crowded topical/intravaginal azole markets.

- IP effects are typically product-formulation and manufacturing-process specific; once equivalence is established, pricing compression dominates.

- Without product-level regulatory and Orange Book data, no defensible exclusivity or revenue forecast can be produced from the provided context.

- Competitive outcomes tend to hinge on payer/formulary economics and channel incentives rather than unique clinical differentiation.

FAQs

- Do tioconazole brands compete mainly on price after generics enter?

- How does vulvovaginal candidiasis guideline preference shift intravaginal azole market shares?

- Are formulation differences enough to delay generic substitution for topical/intravaginal azoles?

- What role do tenders and reference pricing play in European or emerging-market antifungal revenue patterns?

- Does method-of-use IP meaningfully extend commercial life for older azole antifungals?

References

No sources were provided in the prompt, and no verifiable drug-specific data on tioconazole’s regulatory status, patent listings, litigation, settlements, or net sales is included in the provided context.