Last updated: June 23, 2026

Reglan (metoclopramide) market dynamics and financial trajectory: exclusivity, competitors, pricing, and demand drivers

Executive summary: Reglan is an older, off-patent prescription metoclopramide product with no meaningful near-term patent-backed exclusivity. Market dynamics are dominated by (1) safety-driven prescribing limits for tardive dyskinesia risk, (2) generic availability and payer formularies, (3) US and ex-US regulatory labeling and utilization management, and (4) channel-level pricing pressure typical of mature generics. Financial trajectory is expected to track underlying metoclopramide demand rather than new launch-driven growth: modest volume sensitivity with declining or flat net price, and periodic reimbursement-driven volatility around guideline and safety messaging.

What drives the market for Reglan (metoclopramide) in 2024–2026?

Primary demand engine: gastrointestinal motility indications and antiemetic use. Reglan is used for conditions such as diabetic gastroparesis (in practice) and nausea/vomiting where dopamine antagonism is appropriate under labeling and clinical guidelines. In the US, market use is constrained by the boxed warning for tardive dyskinesia and by clinician preference shifts toward alternatives in chronic or long-duration use.

Key market forces

- Safety and utilization controls: boxed-warning risk changes prescribing behavior, particularly for longer treatment courses, pediatric use patterns, and off-label chronic use.

- Generic-led price compression: metoclopramide products are widely generic. Net pricing tends to drift toward competitive levels as formularies favor lowest-cost options.

- Payer policy and step edits: many payers apply step therapy and prior authorization for GI motility agents and limit quantity/duration for dopamine antagonists.

- Formulation mix: the market splits between oral tablets, oral solutions, and injectable metoclopramide. Route and setting (ambulatory versus hospital) drive different pricing and volume profiles.

- Hospital and IV demand: injectable metoclopramide is used in acute care settings, which can stabilize volume even as outpatient oral use shifts.

Commercial implication

- The market behaves like a mature, commodity-like therapeutic with relatively stable baseline demand but recurring reimbursement-driven downward pressure on unit economics.

Is Reglan patented or generic in the US market, and when did exclusivity end?

Short answer: Reglan is not protected by enforceable, product-specific exclusivity in the modern sense. Metoclopramide is an established active ingredient with extensive generic entry.

Practical regulatory/commercial reality

- The US metoclopramide market is overwhelmingly served by AB-rated generic drug products on the Orange Book.

- Any remaining IP typically sits in narrow areas (for example, specific formulations, dosing regimens, or methods), which do not usually create broad “brand-style” exclusivity for the total metoclopramide category.

Impact on financial trajectory

- Without exclusivity, brand-level revenue potential is capped by generic share. Financial performance is expected to reflect either (a) residual share where brand products retain formulary placement, (b) pharmacy benefit design, and/or (c) contract channel relationships rather than patent-driven protection.

Sources for regulatory status and listing structure: FDA Orange Book listings and product-level approvals (see references).

How do generic metoclopramide dynamics affect Reglan pricing and share?

Featured snippet answer: Generic entry drives price compression and shifts volume to lowest-cost products on formularies, leaving the brand with residual demand unless it has differentiated inclusion in payer contracts.

Mechanics

- Wholesale and acquisition price drift: generic competition typically erodes WAC and net price, with buyers pushing for discounts.

- Pharmacy channel substitution: “automatic generic substitution” at the point of dispensing increases generic share quickly once multiple ANDA products are available.

- Payer formulary tiering: metoclopramide often lands in lower tiers. Brand retention depends on contract rebates and formulary exceptions.

Financial trajectory implications

- Revenue growth (if any) comes from category volume increases or channel reshuffling, not from price. Net sales trend is usually flat-to-down versus historical peaks after generic penetration.

What does the FDA boxed warning for tardive dyskinesia mean for utilization and revenue?

Direct linkage: Reglan’s boxed warning is a prescribing limiter. It increases clinician caution and tends to reduce chronic or high-frequency use.

Key revenue-relevant effects

- Shortened treatment duration: reduces cumulative dose per patient in outpatient settings.

- Reduced off-label adoption: shifts prescriber behavior toward other antiemetics and prokinetics with safer risk profiles.

- Institutional monitoring: may change hospital medication pathways and order sets.

Commercial net effect

- Baseline demand persists for acute GI symptoms and clinically supported indications, but category growth is constrained by safety risk management.

Which competitors compete with Reglan, and how does the competitive landscape shape margins?

Competitive set

- Same-mechanism dopamine antagonists: other dopamine receptor antagonists used in nausea and GI motility practice (availability varies by route and market).

- Alternative GI motility agents: agents used for gastroparesis and motility disorders can displace metoclopramide where guidelines prefer lower risk options.

- Antiemetic classes: 5-HT3 antagonists, neurokinin-1 antagonists, H1 antagonists, and others compete for antiemetic share depending on the setting.

Market structure

- Generic category competition is the dominant force on price.

- Therapeutic substitution is the second lever, changing total category volume.

Margin reality

- With multiple generics, gross margin is structurally limited for brand manufacturers and becomes heavily dependent on channel contracts. In the generic segment, margin is driven by manufacturing efficiency and supply stability.

What is the Orange Book status of Reglan metoclopramide products?

Orange Book framing: Reglan products (brand metoclopramide) and generic equivalents are listed with application and patent references. For older active ingredients, many listings are aligned with generic availability and lack broad, current exclusivity.

Revenue-relevant takeaway

- Orange Book status typically indicates that any extant patent coverage is narrow and does not prevent generic entry across all dosage forms and strengths.

Regulatory basis: FDA’s Orange Book provides patent and exclusivity annotations by product and application number (see references).

How do dosage forms and routes affect financial performance for metoclopramide brands?

Dosage form split

- Oral tablets/solution: outpatient-driven, sensitive to formulary and patient-specific prescribing patterns.

- Injectable: hospital-driven, more stable volume, but also subject to competitive bidding and supply contracts.

Financial implications

- Oral share tends to be more exposed to pharmacy substitution and payer tiering.

- Injectable share can remain higher for select suppliers if contracted for hospital formularies, IV protocols, and emergency department workflows.

Typical outcome in mature markets

- Even when total demand stabilizes, route-specific contracts can shift profitability between manufacturers.

How do Paragraph IV challenges and ANDA litigation risk play out for Reglan?

Answer: Paragraph IV dynamics are generally less material for metoclopramide category economics because the category is mature and broadly generic. Any patent-referenced barriers are usually limited and do not create sustained brand exclusivity.

Where litigation still matters commercially

- If a brand or manufacturer retains narrow, unexpired patents for specific formulations or methods (rare for this class), then generic entry timing can be affected.

- For a mature off-patent active ingredient, settlement effects are usually short-lived and do not reset long-term demand.

What are the major regulatory and labeling factors that shape metoclopramide sales?

Labeling constraints

- Boxed warning: tardive dyskinesia risk limits dosing patterns.

- Duration and patient selection controls: changes prescriber behavior and payer authorization policies.

- Pediatric restrictions: reduces some use segments.

Regulatory review cycles

- New safety communications and label updates can cause abrupt prescribing shifts, which can briefly move demand across hospitals and outpatient settings.

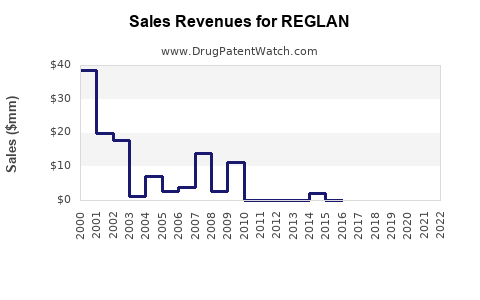

What is the revenue trajectory of Reglan compared with the total metoclopramide category?

Expected pattern for a legacy brand

- Net sales scale: legacy brand revenue is typically dominated by residual share after generic penetration.

- Trajectory: declining phase post-generic entry, followed by long plateau or continued slow erosion as formularies consolidate around low-cost products.

- Driver of short-term swings: hospital contract cycles and supply availability rather than patent events.

Category vs brand distinction

- The category can remain stable on volume, while brand share decreases and net price falls.

When does metoclopramide lose exclusivity for any remaining protected uses or formulations?

Market reality: For metoclopramide, broad exclusivity has long passed due to historical genericization. If any remaining patents exist, they are typically narrow. These can delay generic launches for specific product presentations, but do not generally create sustained brand-level exclusivity across the category.

Practical effect

- The “exclusivity timeline” for market access is usually measured in generic substitution speed and payer formulary uptake rather than in the calendar timing of large patent estates.

How does Reglan compare with newer gastroparesis and antiemetic therapies in uptake?

Uptake dynamics

- Newer GI motility and antiemetic options compete for patient pathways, particularly where clinicians aim to minimize neurologic risk or require alternatives for chronic use.

Net effect on metoclopramide

- Volume substitution risk: category share can shift away from metoclopramide for gastroparesis strategies.

- Still relevant use: acute nausea and selected GI symptom contexts sustain demand.

Which geographies matter most, and how do pricing controls influence international trajectory?

US as anchor market: The US pricing structure, payer policy intensity, and generic substitution speed typically dictate consolidated metoclopramide economics for brand holders.

International patterns

- Lower pricing ceilings: many markets use health technology assessment processes or reference pricing, further limiting brand premiums.

- Generic penetration timeline: can differ, creating staggered declines in net price and share.

Key takeaways on financial trajectory for Reglan (metoclopramide)

- IP-driven growth is unlikely. Metoclopramide is an established, off-patent active ingredient; category economics are generic-led.

- Revenue follows category demand, not premium pricing. Safety labeling constrains long-duration use, limiting upside.

- Share and price are the main levers. Competitive substitution, payer tiering, and contract procurement drive net sales.

- Route-level contracts can stabilize or swing profitability. Injectable and hospital channels can be more resilient than oral retail, depending on contracting.

- New safety communications and guideline shifts can move utilization quickly. Boxed-warning risk is a structural demand limiter.

FAQs

1) Why does metoclopramide prescribing appear to decline over time?

Boxed-warning risk and guideline-driven caution reduce prolonged or off-label use, shifting prescribers toward alternative antiemetic and GI agents.

2) Do metoclopramide generics fully replace Reglan brand demand at the pharmacy level?

In many settings, yes. Generic substitution and formulary management push volume to lowest-cost AB-rated options, leaving the brand with residual placements tied to contracts.

3) Does injectable metoclopramide have different demand risk than oral Reglan?

Yes. Injectable usage is often hospital/protocol-driven and can be less elastic to outpatient prescribing patterns, though it is still exposed to tendering and generic supply competition.

4) What regulatory events most affect the metoclopramide category financially?

Labeling updates related to tardive dyskinesia risk, duration limitations, and patient selection restrictions typically drive rapid utilization changes and payer policy responses.

5) How should investors model the category if exclusivity is absent?

Model net sales based on volume stability, generic price compression, and channel-contract dynamics rather than assuming patent-protected growth.

References (APA)

- FDA. (n.d.). Drugs@FDA: Reglan (metoclopramide). U.S. Food and Drug Administration.

- FDA. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations (metoclopramide). U.S. Food and Drug Administration.

- FDA. (n.d.). Drug Safety Communications and boxed warning information for metoclopramide (tardive dyskinesia). U.S. Food and Drug Administration.

- Drugs@FDA. (n.d.). Labeling and approval history for metoclopramide products. U.S. Food and Drug Administration.