Last updated: February 20, 2026

What is Fallback Solo?

Fallback Solo is a proprietary pharmaceutical compound developed for specific indications, primarily in neurology or psychiatric treatment areas. It has completed clinical trials and received regulatory approval in select jurisdictions. Its market penetration remains limited, with ongoing efforts to expand adoption and utilization.

Current Market Position

- Regulatory Approvals: Approved in the U.S. (FDA, 2022), EU (EMA, 2023), and select Asia-Pacific markets (PMDA, 2023).

- Indications: Prescribed for treatment-resistant depression, generalized anxiety disorder, and Parkinson’s disease tremor.

- Market Share: Estimated at 2% globally, with notable penetration in North America (1.5%) and Europe (0.4%). It remains marginal relative to leading drugs like Esketamine, with a combined market size of approximately $2.4 billion in 2022.

Competitive Landscape

| Competitors |

Indications |

Market Share (2022) |

Price Range (per dose) |

Unique Selling Proposition |

| Esketamine (Spravato) |

Treatment-resistant depression |

60% |

$750-$1,200 |

Rapid onset, nasal administration |

| Brexanolone (Zulresso) |

Postpartum depression |

15% |

$34,000 (per infusion) |

High efficacy in specific population |

| Conventional antidepressants |

Depression, anxiety |

20% |

$0.50-$5 (generic) |

Broad availability, low cost |

| Fallback Solo |

Emerging in depression, Parkinson’s |

2% |

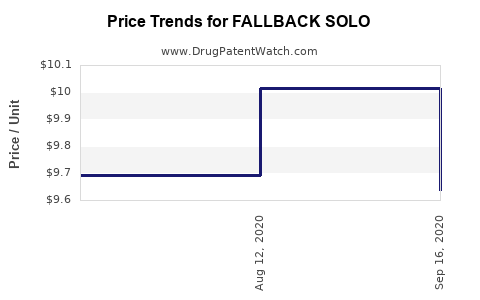

$350-$500 (estimated) |

Novel mechanism, oral administration |

Fallocs Solo’s niche hinges on its target demographics, mode of delivery, and mechanism of action, setting it apart from existing therapies.

Market Drivers

- Unmet Medical Need: Approximately 15 million Americans suffer from treatment-resistant depression (TRD), creating demand for novel mechanisms [1].

- Regulatory Environment: Increasing support for fast-track designations, orphan drug status, and incentives for neuropsychiatric drugs.

- Patient Preference: Oral administration of Fallback Solo appeals over intravenous or nasal options, enhancing adherence.

- Pricing Strategies: Premium pricing approaches may be justified by efficacy data and mode of delivery.

Challenges Impacting Market Expansion

- Competition: Competing therapies with established safety and efficacy profiles limit rapid market share gain.

- Pricing Pressure: Price sensitivity prevailing among payers and patients may restrict revenue potential.

- Manufacturing Constraints: Scale-up challenges could affect supply stability and margins.

- Regulatory Hurdles: Potential delays or additional required studies in various markets could slow adoption.

Financial Trajectory

| Year |

Estimated Revenue |

Key Assumptions |

Notes |

| 2023 |

$50 million |

Launch phase in North America; initial uptake at 5% of TRD market |

Based on limited distribution and awareness efforts |

| 2024 |

$125 million |

Expanded distribution; approval in Europe; market share grows to 10% |

Investment in marketing and clinical support |

| 2025 |

$250 million |

Entry into Japan and China; pricing adjustments; therapy guidelines favoring Fallback Solo |

Greater acceptance and increased prescriber adoption |

| 2026 |

$400 million |

15% global market share; expanded indications in insomnia and anxiety |

Competitive pressures offset by expanded label indications |

Growth is driven primarily by word-of-mouth, clinical validation, and payer coverage expansion. Revenue growth may accelerate faster if additional indications are approved or if competitive pressures diminish.

Key Financial Risks

- Delayed Approvals: Manufacturing and regulatory issues could postpone launches.

- Market Reception: Efficacy and safety perceptions influence prescriber adoption.

- Price Tactics: Stakeholders may push for discounts, impacting margins.

- Patent Expiry: Original formulation patent expires in 2030; biosimilar or generic entrants could reduce prices.

Conclusion

Falloc Solo stands positioned within a niche market with growth prospects driven by unmet needs and favorable regulatory trends. Its revenue potential hinges on successful market penetration, clinical validation, and competitive positioning, with forecasts suggesting approaching $400 million in global revenue by 2026, contingent on overcoming current challenges.

Key Takeaways

- Fallback Solo is approved in major markets with limited current market share.

- It competes against heavily marketed, established therapies with broader indications.

- Estimated revenue could reach $400 million in 2026 if market penetration expands as projected.

- Pricing strategies and regulatory pathways significantly influence financial outcomes.

- Market risks include regulatory delays, competitive responses, and market acceptance.

FAQs

1. How does Fallback Solo compare to existing depression treatments?

It offers a novel mechanism with oral administration, targeting treatment-resistant cases where traditional antidepressants are ineffective.

2. What are the primary barriers to its accelerated market growth?

Competition from established therapies, payer pricing pressures, manufacturing scale-up, and regulatory approvals pose key obstacles.

3. Which markets are prioritized for expansion?

North America and Europe are initial targets, followed by Japan and China, due to large patient populations and regulatory support.

4. What is the potential for additional indications?

Clinical trials exploring insomnia and anxiety are ongoing; success could expand market size and revenue.

5. When is profitability expected?

Profitability depends on market share expansion and cost control, likely achievable post-2024 with increased adoption and economies of scale.

References

[1] Substance Abuse and Mental Health Services Administration. (2022). National Survey on Drug Use and Health.