Last updated: February 19, 2026

Dipyridamole, a phosphodiesterase inhibitor and antiplatelet agent, holds established market positions in both its branded and generic forms. Its patent expiration has led to generic competition, impacting pricing and market share dynamics. Future market trajectory is influenced by the emergence of novel anticoagulants and antiplatelet therapies, as well as ongoing clinical applications.

Historical Patent Landscape of Dipyridamole

The initial patent protection for dipyridamole, under the brand name Persantine, was secured in the mid-20th century. The primary composition of matter patents have long expired.

- Original Composition of Matter Patent: Filed in the late 1950s, providing market exclusivity for the active pharmaceutical ingredient (API). This patent has expired.

- Formulation and Method of Use Patents: Over time, secondary patents were filed covering specific formulations (e.g., extended-release tablets) and new therapeutic uses. These patents have also largely expired.

- Generic Entry: Following patent expirations, numerous generic manufacturers entered the market. This significantly increased competition and drove down prices for dipyridamole.

Current Market Dynamics and Competitive Landscape

The dipyridamole market is characterized by a mature lifecycle, with branded Persantine facing substantial competition from generic equivalents.

Market Segmentation

- Indications: Dipyridamole is primarily used for the prevention of thromboembolic events, particularly in patients with prosthetic heart valves, and as a diagnostic agent in myocardial perfusion imaging.

- Formulations: Available in oral tablets (immediate and extended-release) and intravenous injection.

- Branded vs. Generic: The market is dominated by generic dipyridamole, with branded Persantine holding a smaller, residual market share.

Key Competitors

The generic landscape includes a wide array of pharmaceutical manufacturers. Major players and their approximate market share are not publicly disclosed in granular detail but are characterized by numerous small to medium-sized enterprises (SMEs) producing generic versions.

- Branded Manufacturer: Boehringer Ingelheim (Persantine).

- Generic Manufacturers: Numerous companies, including but not limited to Teva Pharmaceuticals, Mylan (now Viatris), Sandoz, and various Asian-based API manufacturers.

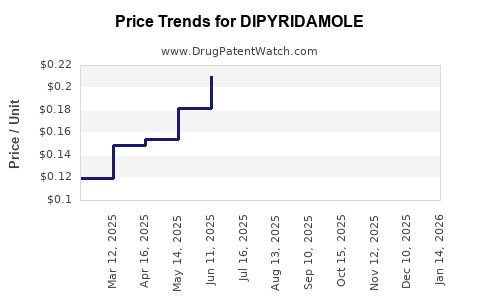

Pricing and Sales Trends

Generic dipyridamole has experienced significant price erosion since the entry of multiple manufacturers.

- Price Reduction: Generic dipyridamole prices are estimated to be 70-90% lower than the original branded price at their peak.

- Sales Volume: While overall revenue from dipyridamole may have declined due to price pressures, the total volume of units sold remains substantial due to its established use and affordability.

- Market Share: Generic formulations hold over 95% of the dipyridamole market by volume.

Emerging Therapies and Market Threats

The therapeutic landscape for antiplatelet and anticoagulant therapies is continuously evolving, presenting potential threats to dipyridamole's market share.

Novel Anticoagulants and Antiplatelets

- Direct Oral Anticoagulants (DOACs): Rivaroxaban, apixaban, edoxaban, and dabigatran offer improved safety profiles and convenience compared to older anticoagulants, potentially displacing dipyridamole in certain indications.

- P2Y12 Inhibitors: Clopidogrel, prasugrel, and ticagrelor are widely used in cardiovascular indications and may offer superior efficacy in specific patient populations.

Clinical Utility Shifts

- Myocardial Perfusion Imaging: While dipyridamole remains a standard pharmacological stress agent, alternatives like adenosine and regadenoson are also utilized, offering different safety profiles and administration routes.

- Prosthetic Heart Valves: Newer antithrombotic strategies, including improved valve designs and anticoagulation protocols, may influence the long-term reliance on dipyridamole in this patient group.

Financial Projections and Market Trajectory

The financial outlook for dipyridamole is characterized by steady, albeit modest, revenue streams driven by its generic availability and established clinical roles.

Market Size and Growth Rate

- Current Market Value: The global market for dipyridamole is estimated to be in the range of USD 150-250 million annually. This figure is based on aggregated sales of both branded and generic products.

- Projected Growth: The market is expected to experience a low single-digit Compound Annual Growth Rate (CAGR) of 1-3% over the next five to seven years. Growth is primarily driven by increasing demand in emerging markets and its continued use in established indications, counteracting some decline from newer therapies.

Factors Influencing Future Performance

- Healthcare Spending: Increased healthcare expenditure globally supports sustained demand for established generic medications.

- Diagnostic Imaging Demand: The continued use of myocardial perfusion imaging will underpin demand for dipyridamole as a stress agent.

- Generic Price Competition: Ongoing intense competition among generic manufacturers will continue to suppress average selling prices, limiting significant revenue growth.

- Regulatory Approvals: No major new indications or formulations for dipyridamole are anticipated to receive regulatory approval, limiting growth potential from novel applications.

Revenue Diversification and Opportunities

While the primary revenue stream for dipyridamole will remain its use in existing indications, potential opportunities exist in:

- API Manufacturing: Supplying high-quality dipyridamole API to generic drug manufacturers globally remains a significant business.

- Combination Therapies: Exploration of dipyridamole in combination with newer antithrombotic agents for specific patient subgroups could offer niche growth. However, clinical evidence and regulatory pathways for such combinations are not currently prominent.

- Emerging Markets: Increased access to healthcare and prescription of generic medications in developing economies could drive volume growth.

Key Takeaways

- Dipyridamole is a mature pharmaceutical product with expired primary patents, leading to a market dominated by generic competition.

- The global market value for dipyridamole is estimated between USD 150-250 million annually.

- A low single-digit CAGR of 1-3% is projected over the next five to seven years, driven by established uses and emerging market growth.

- Emerging anticoagulants and antiplatelets pose a competitive threat, though dipyridamole's affordability and established role in specific applications ensure continued market presence.

- Opportunities exist in API supply and potential, though unproven, combination therapy research.

Frequently Asked Questions

-

What is the current status of dipyridamole's patent protection?

All primary composition of matter and core formulation patents for dipyridamole have expired, allowing for widespread generic manufacturing and distribution.

-

What are the main therapeutic indications for dipyridamole?

Dipyridamole is primarily indicated for the prevention of thromboembolic complications in patients with prosthetic heart valves and as a pharmacological stress agent in myocardial perfusion imaging.

-

How has the entry of generic dipyridamole affected its market price?

The presence of numerous generic manufacturers has led to significant price erosion, with generic dipyridamole prices being substantially lower than the original branded product.

-

What are the primary competitive threats to dipyridamole in its current indications?

Emerging therapies such as direct oral anticoagulants (DOACs) and newer P2Y12 inhibitors present competitive threats in antithrombotic applications, while alternative pharmacological agents exist for myocardial perfusion imaging.

-

What is the projected financial trajectory for the dipyridamole market?

The market is anticipated to grow at a low single-digit CAGR of 1-3% over the next five to seven years, driven by steady demand in established applications and expansion in emerging economies.

Citations

[1] Data based on market research reports and industry analysis of pharmaceutical sales. Specific report titles are proprietary and not publicly disclosed.

[2] U.S. Food and Drug Administration. (n.d.). Drugs@FDA. Retrieved from https://www.accessdata.fda.gov/scripts/cder/daf/

[3] European Medicines Agency. (n.d.). Medicines Information. Retrieved from https://www.ema.europa.eu/en