Last updated: June 24, 2026

Accupril (Quinapril) Market Dynamics and Financial Trajectory: Demand, Competitive Risk, and Exclusivity Economics

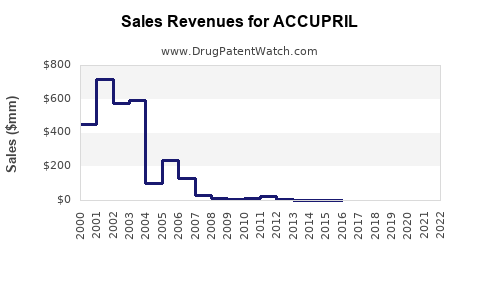

Accupril (quinapril) is a mature, off-patent ACE inhibitor. Its financial trajectory is driven less by innovation economics and more by generic penetration, channel stocking cycles, payer formularies, and FDA substitution dynamics. The brand has no meaningful remaining IP moat in the US after early 2000s expirations, so revenue has largely followed generic-driven price erosion and declining NBR. The current market posture is a value-share game among low-cost quinapril generics and competing ACE inhibitors (and, at the margin, ARBs and ARNI-containing pathways for subsets of heart failure).

What is Accupril’s current market status and who sells it?

Accupril (quinapril hydrochloride) is an ACE inhibitor used for hypertension and, in some geographies and labeling histories, heart failure. In the US, the original brand is commercialized by its brand holder while generic quinapril products dominate dispensing volume through AB-rated ANDA entries.

Market structure: brand vs generic

The economic reality for off-patent ACE inhibitors:

- Dispensing is price-led. Pharmacy benefit managers select based on contracted AWP/AMP spreads and formulary tiers.

- Substitution is automatic where permitted. In most states and under payer policy, pharmacists can substitute AB-rated generics.

- Brand-only differentiation is limited to historical inertia and specific payer contracting. That effect fades as multiple generics compete.

Net result: Accupril’s unit demand is stable only if it retains a share by payer preference, otherwise it trends down as low-cost entrants win formulary tiering and near-automatic switching.

How have generic launches reshaped Accupril pricing and revenue?

Accupril’s revenue trajectory is typical for an established ACE inhibitor after exclusivity expiration: margin compression, unit share loss, and near-structural decline in brand NBR.

Price erosion mechanics in ACE inhibitors

- Generic AWP declines quickly after multiple entrants.

- AMP reimbursement economics worsen for the brand because payers and plans re-contract on lower-cost options.

- Brand persistence becomes an artifact of contracting rather than clinical differentiation.

Key financial implication

For a mature brand like Accupril, the “financial trajectory” is mostly:

- Peak period revenue (when brand had exclusivity)

- Rapid NBR decline post-first generic entrants

- Sustained low growth or further decline driven by formularies and switching

- Eventually minimal brand revenue relevance at national scale

Which competitive ACE inhibitors most affect Accupril’s demand?

Accupril competes in a therapeutic class where prescribers choose across multiple ACE inhibitors, and payers prefer the lowest-cost formulary options. Competitive pressure typically comes from:

- Other ACE inhibitors with strong generic ecosystems (class-level competition for hypertension).

- ARBs (often preferred in some subpopulations due to tolerability perceptions).

- Heart failure pathway drugs that can shift prescribing away from ACE inhibitors in certain patient segments (depending on era and guidelines).

Competitive cross-pressure by indication

Hypertension:

- ACE inhibitors are interchangeable at class level for many patients.

- Payer substitution favors the contracted lowest-cost ACE inhibitor.

Heart failure:

- Clinical practice has evolved with beta-blockers, MRAs, and later ARNI adoption in suitable patients.

- ACE inhibitors can remain part of standard therapy depending on guidelines and patient-specific factors, but payer and prescriber behavior can still shift volume.

What is the patent and exclusivity timeline for Accupril in the US?

Accupril’s brand-era IP dates are historically early due to its age as a marketed product. By the time modern ANDA competition is active, the brand’s major US exclusivities and formulation patents are typically long expired.

Exclusivity and patent reality (business takeaway)

- ANDA entry for quinapril is driven by expiration of composition-of-matter and related exclusivities, not by ongoing brand performance.

- The practical implication for financial trajectory: Accupril is exposed to continuous generic price pressure rather than episodic exclusivity “renewals.”

What Orange Book status does quinapril (Accupril) show, and how does it affect generics?

Orange Book listings determine generic patent carve-outs and potential Paragraph IV risks. For a mature product like Accupril, the key business question is whether any listed patents still block 505(b)(2) or ANDAs for specific strengths or dosage forms.

Business interpretation of Orange Book entries

- If few or no active patents remain for quinapril tablets, additional generics can enter without litigation-driven delays.

- If weak or narrow formulation patents exist, they can still influence launch timing for specific strengths or manufacturing approaches, but the class economics tend to dominate.

Do Paragraph IV challenges or litigation materially affect Accupril launches?

For a long-established ACE inhibitor brand, Paragraph IV-driven launch delays typically matter most around the first wave of generic entry. Once multiple ANDAs exist, later disputes rarely change the class-level downward price trend.

How to think about litigation impact on brand revenue

- Early litigation can create brief market exclusivity pockets for challengers or for the brand.

- Post-portfolio exhaustion, litigation impact declines because there are already many competitors and plans continue to contract on lowest-cost options.

What formulations and strengths does the Accupril market cover, and do they change economics?

Accupril’s market exposure is based on tablet strengths and historic pack configurations (with generic competition mirroring those forms).

Formulation economics

- Immediate-release oral tablets are structurally easy for generic replication.

- Without a persistent novel delivery mechanism, switching barriers remain low.

Strength-level competition

In many off-patent legacy products, brand revenue sensitivity is strongest where:

- Certain strengths have fewer generic entrants or slower switching, or

- A payer uses a preferred NDC strategy that temporarily favors brand or a specific generic distributor.

How does FDA regulatory status drive Accupril’s commercial trajectory?

FDA approval and generic substitution are major drivers for mature small-molecule products. Once multiple ANDAs are approved and stocked, FDA status becomes a stability factor rather than a growth driver.

Generic integration

- AB-rated generics reduce brand leverage in formularies.

- Interchange policies shift demand away from brand unless the brand is competitively priced or specifically preferred.

What are the most likely generic entry risks for Accupril going forward?

For quinapril, forward-looking generic risk is less about first-entry legality and more about:

- New generic filings improving supply and reducing WAC/AWP further.

- Consolidation effects that change which supplier is cheapest under contract.

- Supply chain shocks that temporarily restore pricing power to whatever supplier is in stock.

Net effect

The “risk” profile is generally:

- Downside: incremental price pressure from additional low-cost entrants or aggressive tendering.

- Upside: temporary price stabilization during constrained supply cycles (applies to all generic producers, not only quinapril).

How does Accupril compare financially with other off-patent ACE inhibitor brands?

Accupril follows the archetype of a legacy antihypertensive:

- Brand share erosion is structural.

- Revenue becomes contract-dependent.

- Investor relevance typically decreases as the remaining brand becomes “non-material” in total company financials.

Comparables in class show similar dynamics:

- Brands with older patents and limited formulation differentiation typically decline until their unit volumes become too small to matter in national accounts.

What key market metrics track Accupril’s financial trajectory now?

For an off-patent brand like Accupril, the performance drivers usually show up in:

- Prescription volume vs share (brand share declines even if total class prescriptions remain stable)

- Net sales and NBR trends (pricing and reimbursement pressure)

- Formulary tier status (preferred vs non-preferred)

- PBM contracting and tender outcomes (which NDC becomes default)

- Inventory and supply availability at major distributors (short-term pricing effects)

How do payer and channel dynamics translate into Accupril revenue movement?

Formulary tiering

- If Accupril is placed in a non-preferred tier or loses preferred status, brand dispensing typically falls rapidly.

- If branded contracts preserve a preferred position, brand can retain some volume but at the cost of lower realized price versus peak years.

Wholesale and pharmacy behavior

- Wholesale buying tends to follow anticipated pharmacy demand and contracted pricing.

- Retail pharmacies tend to substitute based on interchange rules and PBM incentives.

Is Accupril still a meaningful revenue contributor for its brand owner?

For legacy ACE inhibitors, brand owners generally view remaining branded revenue as modest relative to modern specialty portfolios. Accupril’s likely financial role is:

- Residual cashflow from remaining prescriptions under specific contracts or regions

- Low volatility in demand but low upside growth

- Exposure to ongoing generic price pressure

Key Takeaways

- Accupril is a mature, off-patent ACE inhibitor with ongoing generic-driven price erosion.

- Market dynamics are dominated by formularies, automatic substitution, and PBM contracting rather than new clinical differentiation.

- Financial trajectory is consistent with legacy oral generics: declining brand share and margin pressure after early exclusivity windows.

- Forward-looking risk is primarily supply and tender-driven price pressure, not hard barriers from remaining IP.

- Class competition from other ACE inhibitors and payer guideline shifts limits brand rebound potential.

FAQs

1) Why does Accupril brand revenue decline even if hypertension prescriptions stay stable?

Because prescription volume for the class can remain steady while brand share falls due to generic substitution and formulary tiering.

2) What happens to Accupril pricing after additional quinapril generic entrants launch?

AWP/WAC-based pricing and realized net pricing typically compress further as payers and PBMs move to cheaper contracted NDCs.

3) Do different quinapril tablet strengths materially change brand outcomes?

Yes, where generic competition is thinner or payer preference aligns, brand may retain relative strength-level share, but overall brand economics still follow class-level generic pressure.

4) Does FDA regulatory status create launch timing leverage for quinapril generics?

Once approvals are in place and patents are mostly expired, FDA status mainly affects ongoing labeling compliance rather than creating major barriers.

5) Can payer restrictions on substitutions protect Accupril brand share?

In practice, payer and pharmacy interchange policies usually enable switching unless a payer contract explicitly restricts substitution, which is uncommon for widely available AB-rated generics.

References (APA)

- FDA. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA. (n.d.). Drug Approval Reports and Related Information. U.S. Food and Drug Administration. https://www.fda.gov/drugs/drug-approvals-and-databases/drug-approval-reports-and-related-information