Last updated: February 15, 2026

What is the current market size and growth forecast for urea as a pharmaceutical drug?

Urea's application as a pharmaceutical drug is limited compared to its primary use as a fertilizer. Globally, the pharmaceutical segment for urea remains a niche, mainly focused on dermatological, urological, and diagnostic applications. The market size for pharmaceutical urea was valued at approximately $200 million in 2022. It is projected to grow at a compound annual growth rate (CAGR) of around 5% over the next five years, reaching roughly $260 million by 2027.

The growth drivers include increased demand for dermatological treatments, expansion of urea-based diagnostic products, and rising prevalence of skin hydration needs. However, the overall market remains constrained by competition from synthetic alternatives and newer therapeutic options.

How does the pharmaceutical market for urea compare with its agricultural use?

Agriculture accounts for over 90% of global urea production, making it the most significant market segment by far. In 2022, the global fertilizer urea market was valued at approximately $50 billion, with an expected CAGR of 3.5% through 2027 [1]. Usages in pharmaceuticals are minor in comparison, representing less than 1% of total demand.

The disparity in market scope is driven by regulatory barriers, manufacturing focus, and economic incentives. The pharmaceutical application constitutes a niche segment mainly in developed countries with higher healthcare spending and advanced dermatological and diagnostic industries.

What are the primary applications and forms of pharmaceutical urea?

In pharmaceuticals, urea is used primarily in:

- Topical treatments for dry, rough, or scaly skin conditions. It functions as a keratolytic agent, aiding in the removal of dead skin.

- Urological formulations such as urea-based solutions for certain bladder treatments.

- Diagnostic reagents, especially in urea breath tests for Helicobacter pylori detection.

Typically available in formulations such as creams, ointments (2% to 40% urea concentrations), solutions, and diagnostic kits. The topical urea market segment is the most active, driven by dermatology.

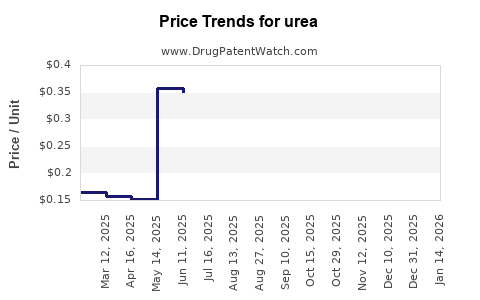

What are the key regulatory and patent considerations impacting pharmaceutical urea?

Urea is an old, well-established compound with a history of safe, widespread use. It is generally recognized as safe (GRAS) for topical and diagnostic uses by the FDA and similar regulatory bodies globally.

No recent significant patent protections exist on basic urea formulations that would hinder commercialization. Patent activity is mainly related to specific formulations, delivery systems, or combination products. Regulatory approval pathways are straightforward due to urea's established safety profile. However, innovations in delivery mechanisms or formulations can face patent applications, which may influence market exclusivity.

What are the primary market drivers and barriers?

Drivers:

- Rising prevalence of skin conditions requiring keratolytic treatment.

- Increasing demand in diagnostic testing for Helicobacter pylori.

- Growth in geriatrics and dermatology sectors.

Barriers:

- Competition from synthetic and alternative therapeutic agents.

- Price sensitivity in developing markets limits premium formulation development.

- Limited patent protections reduce market exclusivity incentives.

What are the key competitors and innovation trends in pharmaceutical urea?

Major pharmaceutical raw material suppliers include:

- Merck KGaA

- Sigma-Aldrich (part of Merck)

- Avantor

- Local chemical companies in emerging markets

Innovations focus on:

- Improved delivery systems for topical formulations (e.g., encapsulation technologies).

- Combination therapies leveraging urea with other dermatological agents.

- Diagnostic kits with higher sensitivity and ease of use.

However, the fundamental use of urea remains stable, with incremental improvements rather than disruptive innovations.

What are the financial prospects and investment opportunities?

While not a high-growth frontier, pharmaceutical urea provides stable, low-risk opportunities for manufacturers specializing in dermatology and diagnostics. Companies that develop novel formulations or combination products can command premium prices. The market's modest size limits large-scale investment returns but benefits from consistent demand.

Investors and firms should monitor regulatory changes, emerging dermatological needs, and diagnostic innovations as signals for future growth or entry points.

Key Market Dynamics Summary

| Aspect |

Details |

| Market Size (2022) |

~$200 million (pharmaceutical applications) |

| Projected CAGR (2023-2027) |

5% |

| Major Applications |

Dermatological treatments, diagnostics, urological formulations |

| Regulatory Status |

Well-established safety profile; minimal patent barriers |

| Main Competitors |

Merck KGaA, Sigma-Aldrich, Avantor |

| Growth Drivers |

Skin condition prevalence, diagnostics demand |

| Barriers |

Competitive alternatives, limited patent protection |

Key Takeaways

- Pharmaceutical urea remains a niche within a dominated global fertilizer market.

- Growth driven by dermatological and diagnostic use cases, at a modest pace.

- Regulatory pathways and patent situations favor incremental innovation.

- Competition centers on formulation improvements and delivery systems.

- Investment opportunities exist in niche product development rather than large-scale manufacturing.

FAQs

1. Is pharmaceutical urea a high-growth market?

No. It exhibits steady, moderate growth primarily driven by dermatological and diagnostic demand.

2. What are the main challenges for pharmaceutical urea commercialization?

Limited patent protections and competition from alternative therapies constrain expansion.

3. How does regulatory approval influence market entry?

The established safety profile simplifies approval processes, facilitating incremental innovation.

4. Are there significant patent barriers for new pharmacy formulations of urea?

Basic urea formulations are off-patent, but novel delivery systems or combinations can be patented.

5. Which regions offer the most opportunities for pharmaceutical urea?

Developed markets such as North America and Europe, where dermatology and diagnostics are advanced; emerging markets are price-sensitive.

Citations:

[1] Market Research Future. "Global Urea Market," 2022.