Last updated: February 19, 2026

Ammonium lactate is a topical pharmaceutical agent utilized for its keratolytic and moisturizing properties, primarily in the treatment of dry skin conditions, ichthyosis, and certain dermatoses. Its market performance is driven by the prevalence of these dermatological conditions and the demand for effective, over-the-counter (OTC) and prescription-based treatments.

What is the Current Market Size and Projected Growth for Ammonium Lactate?

The global market for ammonium lactate is characterized by a steady, albeit modest, growth trajectory. While specific market size figures are not consistently reported as a distinct segment within broader dermatological markets, industry analyses of lactic acid-based skincare products provide proxy indicators. The global skincare market, encompassing therapeutic and cosmetic applications, was valued at approximately USD 150 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 4.5% to 6% through 2030 [1]. Ammonium lactate's share within this market is linked to its therapeutic applications for chronic dry skin conditions.

Factors influencing this growth include:

- Increasing Prevalence of Dermatological Conditions: Rising incidences of eczema, psoriasis, and ichthyosis contribute to sustained demand for effective treatments like ammonium lactate [2].

- Aging Population: Older demographics often experience drier skin, increasing the need for emollients and keratolytic agents [3].

- Growing Awareness of Skincare: Consumers are increasingly seeking solutions for specific skin concerns, including those addressed by ammonium lactate.

- OTC Accessibility: The availability of ammonium lactate formulations without a prescription in many regions broadens its market reach.

What are the Key Therapeutic Applications and Their Market Impact?

Ammonium lactate's primary therapeutic utility lies in its ability to soften and dissolve the stratum corneum, the outermost layer of the skin. This action addresses conditions characterized by thickened, dry, or scaly skin.

- Ichthyosis: Ammonium lactate is a first-line treatment for various forms of ichthyosis, a group of genetic disorders causing severe skin dryness and scaling. Its efficacy in reducing scale and improving skin hydration is well-established [4].

- Xerosis (Dry Skin): For general severe dry skin, especially in areas like the elbows and knees, ammonium lactate provides essential moisture and helps shed dead skin cells, improving texture and comfort.

- Eczema and Psoriasis: While not a primary treatment for the underlying inflammation of eczema or psoriasis, ammonium lactate can manage the associated dryness, scaling, and thickening of the skin, complementing other therapeutic regimens [5].

- Keratosis Pilaris: This common condition, causing small, rough bumps, can be improved by the exfoliating action of ammonium lactate.

The market impact of these applications is directly tied to the patient populations requiring these treatments. Chronic conditions like ichthyosis, though less prevalent than general xerosis, represent a consistent demand for specialized therapies. The broad applicability to common dry skin issues ensures a wider consumer base.

Who are the Major Manufacturers and What is Their Market Share?

The manufacturing landscape for ammonium lactate is characterized by a mix of large pharmaceutical companies and specialized dermatology product manufacturers. Market share is often not disclosed for individual active pharmaceutical ingredients (APIs) or specific formulations but can be inferred from product availability and brand prominence.

Key players in the topical dermatological segment, including those producing ammonium lactate formulations, include:

- Valeant Pharmaceuticals (now Bausch Health Companies): Known for its AmLactin® line of products, a widely recognized brand for therapeutic moisturizers containing ammonium lactate.

- Dermik Laboratories (a Sanofi-Aventis company): Has historically offered prescription-strength ammonium lactate products.

- Generic Pharmaceutical Manufacturers: A significant portion of the market is served by generic versions of ammonium lactate lotions and creams, increasing price competition and accessibility. Companies like Perrigo and Teva Pharmaceutical Industries are major players in the generic topical segment.

- Private Label Manufacturers: Numerous retailers and online distributors offer private-label ammonium lactate products, often produced by contract manufacturers.

Market share is distributed across branded prescription/OTC products and generic alternatives. Branded products often command higher margins due to established brand recognition and formulation specificity, while generics capture volume through price competitiveness.

What are the Patent Landscapes and Exclusivity Periods?

The patent landscape for ammonium lactate itself is largely historical, as the compound has been known and used therapeutically for decades. Key patents would pertain to specific formulations, delivery systems, or novel therapeutic uses.

- Composition of Matter Patents: Original patents on ammonium lactate as a therapeutic agent have long expired.

- Formulation Patents: Patents may exist for specific concentrations, pH ranges, emollient bases, or the inclusion of synergistic ingredients designed to enhance efficacy or patient compliance (e.g., improved texture, reduced irritation). These patents, if active, would protect specific branded products.

- Method of Use Patents: Patents covering new or improved methods of treating specific dermatological conditions with ammonium lactate formulations could also be relevant.

- Exclusivity Periods:

- New Chemical Entity (NCE) Exclusivity: Not applicable to ammonium lactate, as it is an established compound.

- Patent Term: For active formulation patents, the term typically extends 20 years from the filing date, subject to extensions.

- Market Exclusivity: For new indications or unique formulations approved by regulatory bodies (e.g., FDA), various market exclusivity periods can apply (e.g., 3 years for new clinical investigations).

- Generic Entry: Once primary formulation patents expire and regulatory exclusivity periods have elapsed, generic versions can enter the market, significantly impacting pricing and market share for the originator product.

A thorough patent landscape analysis would be required to identify currently active patents that might restrict market entry or necessitate licensing agreements for specific formulations or applications.

What are the Regulatory Considerations and Approvals?

Ammonium lactate is regulated as a drug product by health authorities globally, including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA).

- FDA Approval: Ammonium lactate products are available as both Over-The-Counter (OTC) and prescription drugs.

- OTC Monograph: Certain concentrations and indications for ammonium lactate may fall under OTC drug monographs, streamlining the approval process for manufacturers meeting established standards.

- New Drug Application (NDA): Prescription formulations or those with new indications require an NDA submission, involving extensive clinical data demonstrating safety and efficacy.

- European Medicines Agency (EMA): Similar regulatory pathways exist in the EU, involving marketing authorization applications.

- Labeling Requirements: Products must adhere to strict labeling requirements, including indications, contraindications, warnings, and directions for use.

- Manufacturing Standards: Manufacturers must comply with Current Good Manufacturing Practices (cGMP) to ensure product quality, safety, and efficacy.

- Adverse Event Reporting: Post-market surveillance and reporting of adverse events are mandatory.

The regulatory pathway can influence market entry timelines and costs. OTC availability accelerates market penetration for basic formulations, while prescription status requires more rigorous clinical validation.

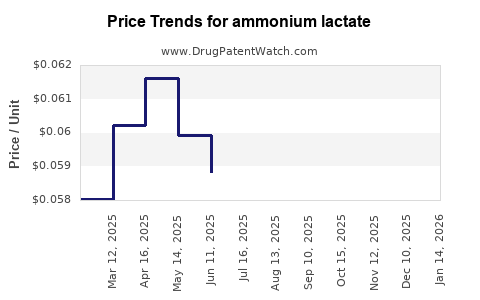

What is the Pricing Strategy and Reimbursement Landscape?

Pricing for ammonium lactate products varies significantly based on branding, formulation strength, volume, and distribution channel.

- Branded Products (e.g., AmLactin®): These typically command premium pricing, reflecting research and development, marketing, and perceived product superiority. Prices can range from USD 20 to USD 40 for standard lotions (e.g., 12% ammonium lactate).

- Generic Products: Generic ammonium lactate formulations are substantially less expensive, often retailing for USD 10 to USD 20 for comparable volumes.

- Prescription vs. OTC: Prescription versions, often at higher concentrations (e.g., 12%), can be priced higher than their OTC counterparts, with pricing influenced by insurance formularies.

- Reimbursement:

- OTC: Generally not covered by insurance.

- Prescription: Coverage varies by insurance provider and formulary. Conditions like ichthyosis or severe eczema may have better reimbursement prospects than general dry skin. Patient co-pays and deductibles are standard.

- Medicare/Medicaid: Coverage is typically limited to medically necessary prescription treatments, often requiring prior authorization for specific dermatological conditions.

The price sensitivity of consumers for general dry skin treatments, contrasted with the medical necessity driving prescription use for severe conditions, shapes the overall pricing strategy.

What are the Key Market Challenges and Opportunities?

Challenges:

- Competition: The topical skincare market is highly competitive, with numerous moisturizing and exfoliating agents available. Ammonium lactate competes with other alpha-hydroxy acids (AHAs), urea, salicylic acid, and petroleum-based emollients.

- Formulation Limitations: Some patients may experience stinging or irritation with higher concentrations of ammonium lactate, limiting its use or requiring specific formulations.

- Perception as a Commodity: Basic ammonium lactate lotions can be perceived as commodity products, particularly in the OTC market, leading to price erosion.

- Limited Differentiation: Unless unique delivery systems or synergistic ingredients are patented, differentiating branded products from generics can be difficult.

Opportunities:

- Underserved Niche Markets: Continued focus on severe dry skin conditions like ichthyosis and specific dermatoses can carve out stable market segments.

- Combination Therapies: Development of formulations combining ammonium lactate with other active ingredients (e.g., ceramides, hyaluronic acid, anti-inflammatories) could offer enhanced efficacy and new market niches.

- Improved Formulations: Research into less irritating, more cosmetically elegant formulations (e.g., lighter textures, faster absorption) can appeal to a broader patient base.

- Geographic Expansion: Expanding availability and market penetration in emerging economies where dermatological care is growing can drive incremental growth.

- Digital Health Integration: Leveraging telemedicine and direct-to-consumer platforms for prescription refills or OTC sales can streamline access and potentially reduce marketing costs.

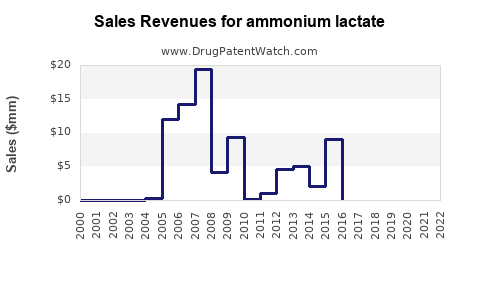

What is the Financial Trajectory and Investment Outlook?

The financial trajectory of ammonium lactate as a product category is expected to be one of stable, low-to-mid single-digit annual growth.

- Revenue Generation: Primarily driven by prescription sales for chronic conditions and steady OTC demand for general dry skin.

- Profitability: Branded, patented formulations offer higher profit margins. Generic competition exerts downward pressure on pricing and margins for non-patented products.

- R&D Investment: Investment is likely to focus on formulation improvements, novel delivery systems, and potential combination therapies rather than on the core API.

- Acquisition Targets: Companies holding proprietary ammonium lactate formulations or strong market positions in specific dermatological niches could be acquisition targets for larger pharmaceutical or consumer healthcare firms seeking to expand their portfolios.

- Investment Outlook: For generic manufacturers, the outlook is stable but dependent on high-volume sales and cost-efficient production. For companies with innovative formulations or patents, the outlook is more promising, offering potential for sustained revenue and premium pricing. Overall, ammonium lactate is not a high-growth, disruptive technology but a reliable component of the dermatological market.

Key Takeaways

Ammonium lactate is a well-established topical pharmaceutical agent with a stable market driven by its efficacy in treating dry skin conditions and dermatoses like ichthyosis. The market is characterized by steady, modest growth, influenced by an aging population and increasing awareness of dermatological health. Competition exists from both branded and generic manufacturers, with pricing reflecting these market dynamics. While the core API's patent landscape is expired, opportunities exist in novel formulations and combination therapies. Regulatory approval pathways, primarily through OTC monographs and NDAs, shape market access. The financial trajectory is stable, with profitability higher for innovative, patented products.

FAQs

-

Is ammonium lactate effective for treating all types of dry skin?

Ammonium lactate is most effective for severe dry skin (xerosis) and conditions involving skin thickening and scaling, such as ichthyosis and keratosis pilaris. For mild dry skin, other emollients may suffice.

-

What is the difference between prescription and OTC ammonium lactate?

Prescription versions typically contain higher concentrations of ammonium lactate (e.g., 12%) and are indicated for more severe skin conditions. OTC versions are generally at lower concentrations (e.g., 5-10%) and are used for milder forms of dry skin.

-

Can ammonium lactate be used on the face?

While formulations exist for facial use, ammonium lactate can cause stinging or irritation, especially on sensitive facial skin. It is advisable to use it cautiously and as directed by a healthcare professional or product labeling, often starting with a lower concentration or applying less frequently.

-

What are the main side effects of ammonium lactate?

Common side effects include transient stinging, burning, or itching upon application, particularly on broken or inflamed skin. Redness and peeling can also occur.

-

How does ammonium lactate compare to other alpha-hydroxy acids (AHAs) like glycolic acid?

Ammonium lactate is an AHA, but its efficacy and tolerability can differ. It is generally considered less irritating than some other AHAs, making it a preferred choice for sensitive or compromised skin. Glycolic acid can offer stronger exfoliation but may also be more irritating.

Citations

[1] Grand View Research. (2023). Skincare Market Size, Share & Trends Analysis Report.

[2] National Eczema Association. (n.d.). Facts about Eczema.

[3] World Health Organization. (2022). Global population ageing 2022.

[4] Williams, M. L., & Elias, P. M. (1983). Ichthyosis and dry skin: a comparison of therapeutic agents. Archives of Dermatology, 119(7), 518-521.

[5] American Academy of Dermatology Association. (n.d.). Psoriasis: Diagnosis and treatment.