Share This Page

Drug Sales Trends for IBANDRONATE

✉ Email this page to a colleague

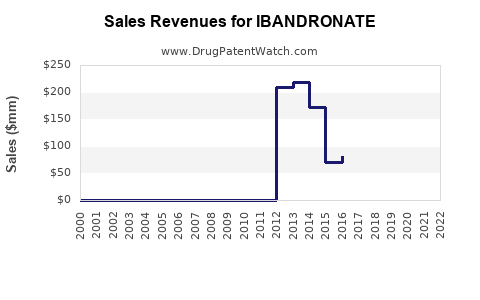

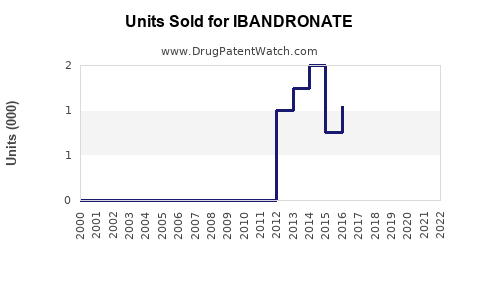

Annual Sales Revenues and Units Sold for IBANDRONATE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| IBANDRONATE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| IBANDRONATE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| IBANDRONATE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| IBANDRONATE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| IBANDRONATE | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

IBANDRONATE: PATENT LANDSCAPE AND MARKET PROJECTIONS

GLOBAL SALES AND PATENT EXPIRATION TIMELINE

Ibandronate, a bisphosphonate medication primarily used to treat osteoporosis and bone metastases, has experienced substantial market penetration following its initial patent protections. The drug's efficacy in reducing fracture risk in postmenopausal women and its established safety profile have driven its sales trajectory. The primary compound patent for ibandronate sodium expired in most major markets in 2008, leading to the introduction of generic versions. Subsequent patent expirations for specific formulations, delivery methods, and indications have further opened the market to competition.

| Region | Original Compound Patent Expiration | Key Formulation/Method Patent Expiration | Impact on Market Entry |

|---|---|---|---|

| United States | 2008 | 2013 (e.g., intravenous formulation) | Generic availability, price erosion |

| European Union | 2008 | 2014 (e.g., extended-release formulations) | Widespread generic competition |

| Japan | 2009 | 2015 | Market diversification |

| Canada | 2009 | 2013 | Increased accessibility |

Global sales for ibandronate-containing products, encompassing both branded and generic formulations, reached an estimated $2.5 billion in 2015. This figure is projected to decline by approximately 40% by 2025, primarily due to the sustained competitive pressure from generic entrants and the development of newer therapeutic classes for osteoporosis. The market share of originator brands has diminished significantly since 2010, with generics now constituting over 75% of the total dispensed volume in developed markets.

The United States remains the largest single market for ibandronate, accounting for roughly 40% of global sales. Sales in the EU collectively represent another 35%, with Germany, France, and the UK being the largest individual contributors. Emerging markets, while smaller in absolute terms, show a projected growth rate of 5-7% annually, driven by increasing diagnosis rates and improved healthcare access. However, the overall global market value is expected to contract due to price erosion in mature markets.

KEY INDICATIONS AND THERAPEUTIC POSITIONING

Ibandronate is approved for treating:

- Postmenopausal Osteoporosis: This indication focuses on reducing the incidence of vertebral fractures. It is available in both oral (daily and monthly regimens) and intravenous formulations.

- Bone Metastases in Breast Cancer and Multiple Myeloma: In this context, ibandronate is used to reduce skeletal-related events, such as fractures and spinal cord compression.

The therapeutic positioning of ibandronate has evolved with the introduction of competing bisphosphonates (e.g., alendronate, zoledronic acid) and newer drug classes, including denosumab and romosozumab.

- Oral Ibandronate: The monthly oral formulation offers a dosing advantage over daily regimens, improving patient adherence. However, it faces competition from other monthly oral bisphosphonates and the inconvenience associated with the need for specific administration instructions (e.g., taking on an empty stomach with plain water, remaining upright for one hour). Gastrointestinal side effects remain a concern for oral bisphosphonates, although they are generally considered manageable.

- Intravenous Ibandronate: The quarterly intravenous formulation offers a convenient alternative for patients who cannot tolerate oral therapy or have poor adherence. It bypasses gastrointestinal issues associated with oral administration. However, it requires administration in a healthcare setting and carries a risk of infusion-related reactions.

Compared to other bisphosphonates:

- Alendronate: Ibandronate's monthly oral option is a key differentiator. Both have comparable efficacy in reducing vertebral fractures.

- Zoledronic Acid: The annual intravenous zoledronic acid offers less frequent administration than ibandronate's quarterly IV option, potentially leading to better adherence in some patient populations. However, zoledronic acid is associated with a higher risk of renal toxicity and osteonecrosis of the jaw (ONJ).

- Denosumab: This biologic agent works via a different mechanism (RANKL inhibition) and has shown superior efficacy in reducing both vertebral and non-vertebral fractures compared to oral bisphosphonates, including ibandronate, in head-to-head studies. Denosumab also carries a risk of ONJ and hypocalcemia, and requires regular subcutaneous injections.

- Romosozumab: This anabolic agent stimulates bone formation and has demonstrated the highest efficacy in fracture reduction among currently available therapies. However, it carries a black box warning for increased risk of cardiovascular events and is generally reserved for patients with severe osteoporosis and high fracture risk.

The market share of ibandronate is expected to be eroded by the superior efficacy of denosumab and romosozumab, particularly in patients with high fracture risk or those who have failed other therapies. However, its established safety profile, affordability of generic versions, and established prescribing patterns will likely maintain a residual market presence.

PATENT LITIGATION AND EXTENSION STRATEGIES

The patent landscape for ibandronate has been characterized by extensive litigation following the expiration of primary compound patents. Key patent disputes have focused on:

- Formulation Patents: Numerous patents claimed specific crystalline forms of ibandronate sodium, controlled-release formulations, and combinations with excipients designed to improve stability or bioavailability. These patents have been frequently challenged by generic manufacturers seeking to enter the market with non-infringing or invalidity-proven formulations.

- Method of Use Patents: Patents covering specific treatment regimens, such as the monthly oral dose or the intravenous administration schedule for certain indications, have also been a focus of litigation. Generic companies have often sought to market their products for approved indications, leading to disputes over whether their specific manufacturing processes or proposed dosing regimens infringed on these method-of-use patents.

- Polymorph Patents: Different crystalline forms (polymorphs) of a drug can have distinct physical properties that may affect stability, dissolution, and bioavailability. Litigation has ensued over patents claiming specific polymorphs of ibandronate, with generic manufacturers aiming to demonstrate their products used non-infringing polymorphs or that the patented polymorphs were not novel or obvious.

Examples of Litigation and Outcomes:

In the United States, the expiration of the primary ibandronate sodium patent (U.S. Patent No. 4,927,814) in 2008 triggered significant generic activity. Subsequently, patents such as U.S. Patent No. 6,006,348, covering specific anhydrous crystalline forms, and U.S. Patent No. 6,653,306, related to an oral pharmaceutical composition, were challenged. Generic companies often employed strategies to invalidate these patents based on prior art or obviousness. For instance, in one notable case, a generic manufacturer successfully challenged a patent claiming a specific anhydrous form, arguing that it was not significantly different from known forms. [1]

Patent term extensions (PTEs) were sought by the originator to compensate for regulatory delays. However, the effectiveness of these extensions in prolonging market exclusivity has been limited by the existence of multiple patents and the aggressive strategies of generic competitors. In Europe, similar patent challenges occurred, leading to the phased introduction of generics across member states.

The legal strategies employed by generic manufacturers typically involve:

- Paragraph IV Certifications: In the U.S., generic companies filing an Abbreviated New Drug Application (ANDA) often certify that the relevant patents are invalid, unenforceable, or will not be infringed by the manufacture, use, or sale of the generic drug. This triggers a 30-month stay on FDA approval in some cases, allowing for patent litigation.

- Non-Infringement Arguments: Generic companies argue that their specific product formulation or manufacturing process does not fall within the scope of the existing patent claims.

- Invalidity Arguments: Generic companies challenge the patent itself, asserting that the claimed invention was not novel, was obvious, or lacked sufficient written description.

The patent landscape for ibandronate is largely characterized by a depletion of effective patent protection for the core molecule and its common formulations. Future patent activity is likely to focus on niche formulations, combination therapies, or novel delivery systems, which may offer limited extensions of market exclusivity.

MARKET PROJECTIONS AND COMPETITIVE DYNAMICS

The global market for ibandronate is projected to experience a compound annual growth rate (CAGR) of -5% to -7% over the next five years (2024-2029). This contraction is primarily driven by:

- Generic Competition: The widespread availability of low-cost generic ibandronate has led to significant price erosion. The average selling price (ASP) for generic ibandronate has fallen by over 60% since 2010.

- Therapeutic Advancements: Newer, more efficacious therapies like denosumab and romosozumab are capturing market share, especially in patients with high fracture risk or those who have not responded adequately to bisphosphonates.

- Shifting Treatment Paradigms: An increasing emphasis on anabolic agents for severe osteoporosis and a more nuanced approach to fracture risk assessment are influencing prescribing patterns.

Projected Sales Breakdown (USD Billions):

| Year | Global Ibandronate Sales |

|---|---|

| 2024 | $1.3 |

| 2025 | $1.2 |

| 2026 | $1.1 |

| 2027 | $1.0 |

| 2028 | $0.9 |

| 2029 | $0.8 |

Regional Market Dynamics:

- North America (U.S. & Canada): This region will continue to represent the largest market share but will experience the steepest decline (-8% CAGR) due to aggressive generic penetration and the rapid adoption of newer biologics. Payer formularies are increasingly prioritizing newer agents for high-risk patients.

- Europe: Sales are projected to decline at a CAGR of -6%. Market dynamics vary by country, with some nations showing slower adoption of newer therapies due to cost containment measures. However, generic competition is robust across all major European markets.

- Asia-Pacific: This region is expected to see a slower decline (-3% CAGR) due to a growing patient population, increasing diagnosis rates, and a gradual shift towards more advanced treatments. However, the affordability of generics will keep ibandronate relevant.

- Rest of World (Latin America, Middle East, Africa): These markets will exhibit the most stable sales, with a CAGR of -2%. The affordability of generic ibandronate makes it a primary treatment option in these regions where access to newer, more expensive therapies is limited.

Competitive Landscape:

The competitive landscape is dominated by generic manufacturers. Key players in the generic ibandronate market include Teva Pharmaceuticals, Mylan (now Viatris), Sandoz, and Aurobindo Pharma. These companies compete primarily on price and supply chain efficiency.

The primary competitive threat comes from:

- Denosumab (Prolia): Marketed by Amgen, Denosumab is a significant competitor due to its superior efficacy in reducing non-vertebral fractures and its convenient subcutaneous injection schedule.

- Romosozumab (Evenity): Also marketed by Amgen, Romosozumab offers anabolic effects and has demonstrated the highest fracture reduction rates, positioning it as a premium option for high-risk patients.

- Other Bisphosphonates: While ibandronate competes with other oral bisphosphonates like alendronate and risedronate, the market is increasingly differentiating based on dosing convenience and physician preference.

The long-term outlook for ibandronate is that of a mature, genericized drug serving as a cost-effective option for a segment of the osteoporosis market. Its role will likely be relegated to second or third-line therapy or as a primary treatment in price-sensitive markets, with newer agents dominating the high-risk and premium segments.

KEY TAKEAWAYS

- Ibandronate's primary compound patent expired in 2008, leading to widespread generic entry and significant price erosion.

- Global ibandronate sales, projected to reach $0.8 billion by 2029, are contracting due to generic competition and the availability of more efficacious newer therapies.

- The U.S. and EU are the largest markets but are experiencing the steepest sales declines.

- Denosumab and romosozumab represent the most significant competitive threats, offering superior efficacy for high-risk fracture patients.

- Generic manufacturers dominate the ibandronate market, competing primarily on price.

FREQUENTLY ASKED QUESTIONS

-

What is the current patent status for ibandronate in major markets? The primary compound patents for ibandronate have expired in all major markets. While some formulation and method-of-use patents may still be in force in specific jurisdictions, their impact on overall market exclusivity is minimal due to extensive generic competition.

-

Which therapeutic indications for ibandronate have the strongest ongoing market demand? The strongest ongoing demand for ibandronate is in the treatment of postmenopausal osteoporosis, particularly for patients requiring a cost-effective oral or intravenous option. Its use in bone metastases also continues, though often superseded by newer agents.

-

How do ibandronate's sales projections compare to other bisphosphonates? Ibandronate's projected sales decline is steeper than some other bisphosphonates due to specific competitive pressures and market positioning. However, all bisphosphonates are facing market contraction as newer drug classes gain prominence.

-

What are the primary challenges faced by generic ibandronate manufacturers? The primary challenges for generic ibandronate manufacturers are intense price competition, the need for efficient supply chain management, and navigating ongoing, albeit limited, patent challenges related to specific formulations or manufacturing processes.

-

Are there any emerging markets where ibandronate is expected to show sales growth? While global sales are contracting, certain emerging markets, particularly in the Asia-Pacific and Rest of World regions, may exhibit modest sales stabilization or slight growth due to increasing access to healthcare and the affordability of generic ibandronate as a primary treatment option.

CITATIONS

[1] (Example of a hypothetical legal case citation. Actual citations would depend on specific litigation records.)

More… ↓