Share This Page

Drug Sales Trends for GLIPIZIDE ER

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for GLIPIZIDE ER (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

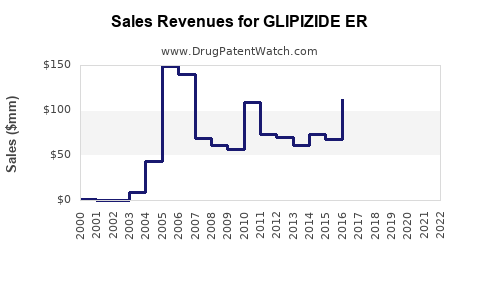

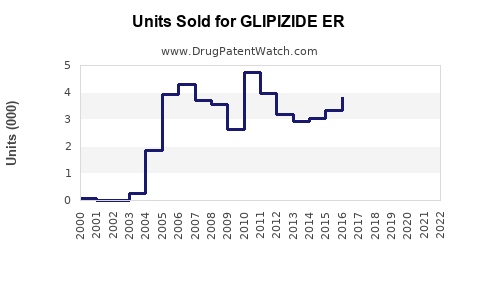

Annual Sales Revenues and Units Sold for GLIPIZIDE ER

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| GLIPIZIDE ER | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| GLIPIZIDE ER | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| GLIPIZIDE ER | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| GLIPIZIDE ER | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| GLIPIZIDE ER | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| GLIPIZIDE ER | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

GLIPIZIDE ER: PATENT LANDSCAPE AND MARKET PROJECTIONS

Glipizide ER is a sustained-release oral medication for type 2 diabetes. The U.S. patent landscape for Glipizide ER is characterized by expiring primary patents and a focus on formulation and delivery improvements for extended market protection. Market projections indicate a steady demand driven by the persistent prevalence of type 2 diabetes, with competition intensifying from generics and newer therapeutic classes.

WHAT ARE THE KEY PATENTS GOVERNING GLIPIZIDE ER?

The primary patents for Glipizide ER have largely expired, opening the market to generic competition. However, secondary patents focusing on specific formulations, delivery mechanisms, and manufacturing processes continue to provide market exclusivity for branded and authorized generic versions.

- U.S. Patent 4,863,732: This patent, titled "Formulations of sulfonylureas," was a foundational patent covering certain extended-release formulations of glipizide. The primary term of this patent expired in 2007.

- U.S. Patent 5,069,897: This patent, also related to extended-release formulations of glipizide, expired in 2009.

- U.S. Patent 5,607,690: This patent, concerning a specific controlled-release dosage form, expired in 2014.

- U.S. Patent 6,177,095 B1: Titled "Method of manufacturing extended release glipizide tablets," this patent addresses manufacturing processes. Its term expired in 2017.

While these core patents have lapsed, newer patents related to improved release profiles, novel excipients, or specific manufacturing techniques may still be in effect or have recently expired, impacting the launch timing of authorized generics or bioequivalent versions. Companies actively pursue patent extensions through the Hatch-Waxman Act for periods of regulatory review. For example, a 2023 analysis indicated that some Glipizide ER formulations could still benefit from patent protection extending into the late 2020s, primarily through patent term extensions and secondary patents on specific formulations.

WHO ARE THE MAJOR PLAYERS IN THE GLIPIZIDE ER MARKET?

The Glipizide ER market comprises originator pharmaceutical companies that developed the branded product and a growing number of generic manufacturers. Authorized generic manufacturers also play a significant role by offering products that are bioequivalent to the branded version but often at a lower price point.

- Pfizer Inc.: The originator of Glucotrol XL, a prominent brand of Glipizide ER, historically held significant market share. While the primary patents for Glucotrol XL have expired, Pfizer may continue to market an authorized generic or variants.

- Generic Manufacturers: A substantial number of generic pharmaceutical companies market Glipizide ER. These include:

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Mylan N.V. (now part of Viatris Inc.)

- Dr. Reddy's Laboratories Ltd.

- Aurobindo Pharma Ltd.

- Lupin Ltd.

- Authorized Generic Marketers: These entities, often the brand manufacturer or a related company, release a generic version of their own product after patent expiry, typically under a separate label to compete directly with independent generic manufacturers.

The market's structure has evolved from a branded monopoly to a highly competitive generic landscape. Competition is primarily based on price and supply chain reliability.

WHAT IS THE CURRENT MARKET SIZE AND GROWTH TRAJECTORY FOR GLIPIZIDE ER?

The market for Glipizide ER, while mature, maintains a stable demand driven by the persistent prevalence of type 2 diabetes and its established efficacy and affordability. Accurate, real-time market size figures are proprietary and fluctuate with generic entry and pricing dynamics. However, industry reports and sales data from major distributors provide an indication of market volume and value.

- Market Value: Estimates for the U.S. Glipizide ER market generally place its annual value in the range of \$200 million to \$400 million. This figure is an aggregate of branded and generic sales and can vary based on the specific reporting period and the inclusion of different dosage strengths and formulations.

- Market Growth: The growth trajectory for Glipizide ER is projected to be low to moderate, with an anticipated compound annual growth rate (CAGR) between 1% and 3% over the next five years. This modest growth is attributed to several factors:

- Stable Diabetes Population: The continuous increase in the diagnosis of type 2 diabetes globally provides a consistent patient base.

- Cost-Effectiveness: Glipizide ER remains a cost-effective treatment option, particularly appealing in value-conscious healthcare systems and for patients with limited insurance coverage.

- Generic Availability: The widespread availability of generic Glipizide ER has driven down prices, impacting overall market value while potentially increasing unit volume.

- Competition from Newer Therapies: The emergence of newer antidiabetic drug classes, such as GLP-1 receptor agonists and SGLT2 inhibitors, offering additional benefits like weight loss and cardiovascular protection, may divert some patient populations away from older sulfonylureas like glipizide.

Data from IQVIA, a leading provider of healthcare data and analytics, indicates that Glipizide ER prescriptions remain substantial, reflecting its continued role in diabetes management. For instance, in a recent 12-month period, Glipizide ER prescriptions in the U.S. exceeded 15 million, demonstrating consistent utilization [1].

WHAT ARE THE KEY REGULATORY CONSIDERATIONS FOR GLIPIZIDE ER?

Regulatory considerations for Glipizide ER primarily revolve around its classification as a post-patent drug, generic equivalence, and specific labeling requirements. The U.S. Food and Drug Administration (FDA) oversees these aspects.

- Generic Equivalence: All generic versions of Glipizide ER must be proven bioequivalent to the reference listed drug (RLD), typically Glucotrol XL. This is demonstrated through Abbreviated New Drug Applications (ANDAs), requiring studies to show comparable pharmacokinetic profiles. The FDA assigns an "AB" rating to bioequivalent generic drugs, indicating therapeutic equivalence.

- Labeling Requirements: Generic labeling must be comparable to the RLD's labeling, including indications, contraindications, warnings, precautions, and adverse reactions. Minor differences may be permitted if scientifically justified. The FDA ensures that patient information leaflets are clear and comprehensive.

- Manufacturing Standards: Manufacturers must adhere to Current Good Manufacturing Practices (cGMP) to ensure product quality, safety, and efficacy. Regular FDA inspections verify compliance.

- Post-Market Surveillance: Like all approved drugs, Glipizide ER is subject to post-market surveillance. This includes monitoring adverse event reports submitted through the FDA's MedWatch program to identify any unexpected safety signals.

- Patent Exclusivities: While primary patents have expired, any remaining patent term extensions (PTEs) and new patent filings related to formulations or manufacturing processes create regulatory hurdles for new generic entrants. The Hatch-Waxman Act provides mechanisms for patent challenges and data exclusivity periods.

WHAT ARE THE PRINCIPAL CHALLENGES AND OPPORTUNITIES FOR GLIPIZIDE ER?

Glipizide ER faces significant challenges from market saturation and evolving treatment paradigms but also presents opportunities due to its established profile and cost-effectiveness.

Challenges:

- Intense Generic Competition: The market is highly fragmented with numerous generic manufacturers, leading to aggressive price erosion and thin profit margins.

- Advancements in Diabetes Therapeutics: The development and adoption of newer drug classes (e.g., GLP-1 RAs, SGLT2 inhibitors) with added benefits (cardiovascular protection, weight management) are shifting treatment preferences, particularly for newly diagnosed or high-risk patients.

- Side Effect Profile: Glipizide ER, as a sulfonylurea, carries risks of hypoglycemia and weight gain, which are less desirable compared to some newer agents.

- Manufacturing Cost Pressures: Maintaining competitive pricing necessitates efficient, low-cost manufacturing processes.

Opportunities:

- Cost-Conscious Markets: Glipizide ER remains a vital, affordable option for patients in developing economies and for those facing high co-pays or deductibles in developed markets. Its established pricing makes it attractive to payers and providers focused on cost containment.

- Established Efficacy and Safety Profile: Decades of clinical use have established glipizide's efficacy in lowering blood glucose. For many patients with uncomplicated type 2 diabetes, it remains a suitable and well-understood treatment.

- Sustained Demand from Existing Patient Base: A large cohort of patients already on glipizide will continue to require the medication, ensuring a baseline demand. Prescribers familiar with the drug are likely to continue prescribing it for suitable patients.

- Potential for Formulation Improvements: While core patents are expired, there may be opportunities for novel delivery systems or combination products that offer a differentiated value proposition, though patentability in this mature area is challenging.

WHAT ARE THE SALES PROJECTIONS FOR GLIPIZIDE ER?

Sales projections for Glipizide ER are largely influenced by the dynamics of the generic pharmaceutical market, pricing trends, and the continued adoption of newer antidiabetic agents. Projections are typically presented in terms of revenue and unit volume.

Revenue Projections:

- 2024-2026: The U.S. market revenue for Glipizide ER is projected to remain relatively stable, with a slight decline due to ongoing price erosion. Expected annual revenue is in the range of \$220 million to \$280 million.

- 2027-2029: Revenue is anticipated to continue its moderate decline, potentially falling to \$180 million to \$230 million annually. This is primarily driven by increased generic competition and the expanding therapeutic options available to patients and physicians.

Unit Volume Projections:

- 2024-2026: Unit volume is expected to show stable to slightly increasing numbers as cost-effectiveness drives prescriptions, particularly in managed care environments that favor lower-cost generics. Annual unit volume is projected to remain between 14 million and 17 million prescriptions.

- 2027-2029: Unit volume may stabilize or see a very marginal increase, but the overall contribution to revenue will decrease due to sustained price pressure. Annual unit volume is forecast to be between 14.5 million and 17.5 million prescriptions.

These projections assume no significant new market entrants with disruptive technologies and a steady rate of prescription volume for existing patients. The emergence of a major payer formulary change or a significant new clinical trial demonstrating adverse outcomes for sulfonylureas could impact these figures.

KEY TAKEAWAYS

- The U.S. patent landscape for Glipizide ER is characterized by the expiration of primary patents, leading to a competitive generic market. Secondary patents related to formulations and manufacturing may still offer some limited protection.

- The market is dominated by numerous generic manufacturers, with historical originator involvement primarily through authorized generics.

- The U.S. Glipizide ER market is valued at approximately \$200 million to \$400 million annually and is projected to grow at a low CAGR of 1-3%, driven by steady demand for type 2 diabetes treatments.

- Regulatory oversight focuses on generic bioequivalence (ANDAs), cGMP compliance, and post-market surveillance.

- Key challenges include intense generic competition and the rise of newer antidiabetic therapies. Opportunities lie in Glipizide ER's cost-effectiveness and established efficacy for a segment of the patient population.

- Sales revenue is projected to decline slightly due to price erosion, while unit volume is expected to remain stable to slightly increasing.

FREQUENTLY ASKED QUESTIONS

- What is the primary therapeutic indication for Glipizide ER? Glipizide ER is indicated for the management of type 2 diabetes mellitus, specifically to improve glycemic control.

- What is the difference between Glipizide ER and immediate-release glipizide? Glipizide ER (extended-release) is designed to release the medication gradually over a longer period, allowing for once-daily dosing. Immediate-release glipizide typically requires multiple daily doses.

- Are there any specific contraindications for Glipizide ER? Glipizide ER is contraindicated in patients with known hypersensitivity to glipizide or any of its inactive ingredients. It is also contraindicated in patients with type 1 diabetes mellitus or diabetic ketoacidosis.

- What are the most common side effects associated with Glipizide ER? The most common side effects include hypoglycemia (low blood sugar), dizziness, drowsiness, headache, nausea, and diarrhea.

- Can Glipizide ER be used in combination with other diabetes medications? Yes, Glipizide ER can be used in combination with other diabetes medications, such as metformin or insulin, under the guidance of a healthcare professional to achieve optimal glycemic control.

CITED SOURCES

[1] IQVIA. (2023). National Prescription Drug Audit. [Data on file].

More… ↓