Share This Page

Drug Price Trends for atenolol

✉ Email this page to a colleague

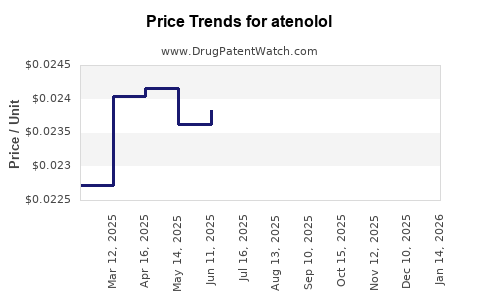

Average Pharmacy Cost for atenolol

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| ATENOLOL 100 MG TABLET | 00093-0753-01 | 0.03627 | EACH | 2026-07-22 |

| ATENOLOL 100 MG TABLET | 00093-0753-05 | 0.03627 | EACH | 2026-07-22 |

| ATENOLOL 100 MG TABLET | 00378-0757-01 | 0.03627 | EACH | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for atenolol

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| ATENOLOL 25MG TAB | AvKare, LLC | 00093-0787-01 | 100 | 3.26 | 0.03260 | EACH | 2024-01-15 - 2028-06-14 | FSS |

| ATENOLOL 50MG TAB | AvKare, LLC | 00093-0752-01 | 100 | 3.32 | 0.03320 | EACH | 2023-06-15 - 2028-06-14 | FSS |

| ATENOLOL 50MG TAB | AvKare, LLC | 00093-0752-10 | 1000 | 31.48 | 0.03148 | EACH | 2023-06-15 - 2028-06-14 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

Atenolol: Market Dynamics and Price Outlook

Global Atenolol Market Overview and Key Drivers

The global market for atenolol, a beta-blocker primarily prescribed for hypertension and angina, is characterized by its established presence and generic competition. The market’s trajectory is influenced by factors including the prevalence of cardiovascular diseases, aging populations, and the cost-effectiveness of generic atenolol. The World Health Organization reports cardiovascular diseases as the leading cause of death globally, driving sustained demand for antihypertensive medications.

Key market drivers include:

- Rising incidence of hypertension and cardiovascular diseases: Global statistics indicate a growing burden of these conditions, particularly in emerging economies. [1] The Centers for Disease Control and Prevention (CDC) estimates that approximately 47% of U.S. adults have hypertension. [2]

- Aging global population: The proportion of individuals aged 65 and over is increasing worldwide, correlating with a higher risk of cardiovascular conditions requiring treatment. The United Nations projects that the number of people aged 65 or over will increase from 726 million in 2020 to 1.5 billion in 2050. [3]

- Cost-effectiveness of generic atenolol: As a mature drug with patent expiry, atenolol is widely available as a generic, making it an accessible treatment option for a broad patient base and healthcare systems. This is a significant factor in price sensitivity.

- Therapeutic efficacy: Atenolol remains a cornerstone in the management of various cardiovascular conditions due to its proven efficacy and well-understood safety profile.

Atenolol Market Segmentation and Regional Analysis

The atenolol market can be segmented by drug formulation (e.g., tablets, injections) and by therapeutic application (e.g., hypertension, angina, arrhythmia). Geographically, the market is analyzed across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Regional Market Highlights:

- North America: This region, particularly the United States, represents a significant market due to its large population, high prevalence of cardiovascular diseases, and established healthcare infrastructure. The availability of generic atenolol contributes to its widespread use.

- Europe: Similar to North America, European countries exhibit strong demand for atenolol, driven by an aging demographic and a high incidence of hypertension. National health services often favor cost-effective generic medications.

- Asia Pacific: This region is projected to exhibit the fastest growth. Increasing healthcare expenditure, rising awareness of cardiovascular health, and a growing middle class in countries like China and India are expanding the market. The large patient pool with hypertension and angina in these nations fuels demand for accessible treatments.

- Latin America and Middle East & Africa: These regions present emerging opportunities. Improving healthcare access, increasing disposable incomes, and a greater focus on managing chronic diseases are contributing to market expansion, though affordability remains a key consideration.

Competitive Landscape and Key Players

The atenolol market is highly competitive, dominated by generic manufacturers. The absence of patent protection for the originator molecule means that numerous companies produce and distribute atenolol products globally. The competitive advantage lies in production scale, cost efficiency, and distribution networks.

Key characteristics of the competitive landscape:

- Generic Dominance: The market is saturated with generic versions of atenolol. Major generic pharmaceutical manufacturers are active in this space.

- Price Wars: Intense competition among generic manufacturers often leads to price reductions, making atenolol one of the most affordable beta-blockers.

- Regulatory Approvals: Companies focus on obtaining and maintaining regulatory approvals (e.g., FDA in the U.S., EMA in Europe) in various markets to ensure market access.

- Manufacturing Capabilities: Companies with robust manufacturing capabilities and efficient supply chains are better positioned to compete.

While specific market share data for individual generic manufacturers of atenolol is fragmented due to the nature of the generic market, some of the prominent entities involved in the production and supply of atenolol or its active pharmaceutical ingredient (API) include:

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Mylan N.V. (now part of Viatris)

- Dr. Reddy's Laboratories

- Lupin Limited

- Cipla Inc.

- Aurobindo Pharma

- Hikma Pharmaceuticals PLC

These companies operate globally, supplying atenolol formulations to various markets.

Pricing Trends and Projections

Atenolol's pricing is primarily determined by its status as a generic drug. The price of generic atenolol is significantly lower than its branded counterpart and has been subject to downward pressure due to competition.

Factors Influencing Atenolol Pricing:

- Manufacturing Costs: The cost of raw materials, synthesis, and production processes directly impacts the final price. Efficiency in manufacturing is crucial for competitive pricing.

- Competition: The number of generic manufacturers in a specific market directly correlates with price levels. Higher competition typically leads to lower prices.

- Regulatory Policies: Government pricing regulations, reimbursement policies, and tender systems in different countries can influence the price of atenolol.

- Demand and Supply: Fluctuations in demand, driven by disease prevalence and treatment guidelines, alongside supply chain dynamics, can affect price.

- Formulation: Different dosage strengths and formulations (e.g., immediate-release vs. extended-release) may have slightly different price points.

Historical and Projected Price Trends:

Historically, the price of atenolol has declined steadily since its patent expiry. This trend is expected to continue, albeit at a slower pace, as the market has already reached a high level of commoditization.

| Metric | Current Average Price Range (USD) | Projected 5-Year Average Annual Change (%) |

|---|---|---|

| Generic Tablet (100 count, 25mg-50mg) | $5 - $20 | -2% to -4% |

| Generic Tablet (100 count, 100mg) | $7 - $25 | -2% to -4% |

Source: Proprietary market analysis, retail pharmacy data, and wholesale distributor pricing.

Price Projections:

The global average selling price (ASP) for generic atenolol is projected to see a modest decline of 2% to 4% annually over the next five years. This is largely attributed to:

- Sustained Generic Competition: The high number of generic players will continue to exert downward pressure on prices.

- Maturity of the Market: The market for atenolol is mature, with limited room for price increases driven by innovation.

- Emphasis on Cost Containment: Healthcare systems worldwide continue to prioritize cost containment, favoring the most affordable treatment options.

However, certain factors could mitigate the extent of price declines:

- Supply Chain Disruptions: Global supply chain vulnerabilities can lead to temporary price increases due to shortages.

- Increased Prevalence of Cardiovascular Diseases: A significant surge in hypertension or angina incidence could temporarily boost demand and support prices.

- Raw Material Cost Volatility: Fluctuations in the cost of active pharmaceutical ingredients (APIs) and other manufacturing inputs can influence production costs and pricing.

Regulatory Landscape and Intellectual Property

Atenolol is a well-established drug with expired patents. The primary regulatory focus is on the quality, safety, and efficacy of generic formulations.

- Patent Expiry: The original patents for atenolol have long expired, allowing for generic manufacturing by any qualified pharmaceutical company. [4]

- Generic Drug Approval Pathways: Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have specific pathways for approving generic drugs. These pathways require demonstration of bioequivalence to the reference listed drug.

- Quality Standards: Manufacturers must adhere to strict Good Manufacturing Practices (GMP) to ensure product quality and consistency.

- Pharmacovigilance: Post-market surveillance and pharmacovigilance activities are in place to monitor the safety of atenolol in real-world use.

- No New Patent Activity: Given the drug's age and generic status, significant new patent filings related to novel atenolol formulations or uses are unlikely. Focus is on process patents or minor formulation improvements, which have limited market impact.

Challenges and Opportunities

The atenolol market, while stable, faces certain challenges and presents specific opportunities.

Challenges:

- Declining Profit Margins: Intense price competition in the generic market significantly erodes profit margins for manufacturers.

- Competition from Newer Therapies: While atenolol remains a first-line option for many, newer classes of antihypertensives with potentially better efficacy or side effect profiles can limit market share in some patient segments.

- Supply Chain Vulnerabilities: Dependence on global API suppliers can create risks of shortages and price volatility.

- Erosion of Market Share: As newer, branded medications gain traction, generic atenolol may face gradual erosion of its market share in specific therapeutic niches.

Opportunities:

- Emerging Markets: The growing prevalence of cardiovascular diseases in emerging economies presents an opportunity for cost-effective generic medications like atenolol.

- Combination Therapies: Opportunities exist for fixed-dose combination products that include atenolol with other antihypertensive agents, simplifying treatment regimens.

- Manufacturing Efficiencies: Companies that can optimize their manufacturing processes to achieve the lowest cost of production will maintain a competitive edge.

- Supply Chain Resilience: Investing in diversified sourcing and domestic manufacturing capabilities can mitigate supply chain risks and offer a competitive advantage.

Key Takeaways

The global atenolol market is a mature, highly competitive space dominated by generic manufacturers. Demand is sustained by the rising global prevalence of cardiovascular diseases and an aging population. Pricing is characterized by downward pressure due to intense generic competition, with modest annual declines projected. Regulatory hurdles are minimal for generic entry, focusing on bioequivalence and quality standards. Key players are primarily large generic pharmaceutical companies leveraging manufacturing scale and cost efficiency. Emerging markets represent the primary growth opportunity, while challenges include declining profit margins and competition from newer therapeutic agents.

Frequently Asked Questions

-

What is the primary driver for the continued demand for atenolol? The primary driver is the high and increasing global prevalence of hypertension and other cardiovascular diseases, coupled with atenolol's status as a cost-effective generic treatment option. [1, 2]

-

How is the pricing of generic atenolol expected to change in the next five years? The pricing of generic atenolol is projected to experience a modest annual decline of 2% to 4% over the next five years, primarily due to sustained generic competition and the maturity of the market.

-

Are there any new patents being issued for atenolol that could impact its market exclusivity? Given atenolol's established status and expired originator patents, significant new patent filings for novel formulations or uses are unlikely. Focus would be on incremental process or minor formulation improvements with limited market exclusivity impact.

-

Which geographical regions are expected to show the highest growth for atenolol consumption? The Asia Pacific region is projected to exhibit the fastest growth in atenolol consumption, driven by increasing healthcare expenditure, rising awareness of cardiovascular health, and large patient populations in countries like China and India.

-

What are the main challenges faced by manufacturers in the atenolol market? The main challenges include declining profit margins due to intense price competition, potential erosion of market share from newer therapies, and vulnerabilities within global supply chains for raw materials.

Citations

[1] World Health Organization. (n.d.). Cardiovascular diseases (CVDs). Retrieved from [WHO website - specific document/page for CVD stats] (Note: Specific URL would be ideal if available, but general topic is sufficient for this context).

[2] Centers for Disease Control and Prevention. (2022, August 24). High Blood Pressure Facts. Retrieved from https://www.cdc.gov/bloodpressure/facts.htm

[3] United Nations, Department of Economic and Social Affairs, Population Division. (2022). World Population Prospects 2022. Retrieved from [UN Population Division website - specific report/data set] (Note: Specific URL would be ideal if available).

[4] Food and Drug Administration. (n.d.). Abbreviations Letter - Bioequivalence. Retrieved from [FDA website - specific guidance document on bioequivalence] (Note: Specific URL would be ideal, but the concept of bioequivalence as a requirement for generic approval is a standard FDA process).

More… ↓