Share This Page

Drug Price Trends for TRANEXAMIC ACID

✉ Email this page to a colleague

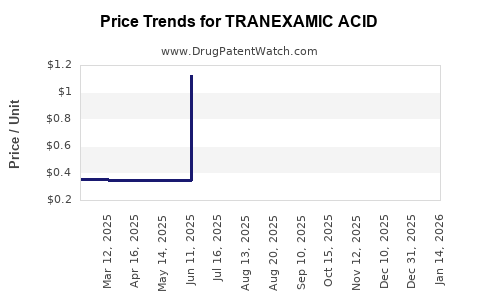

Average Pharmacy Cost for TRANEXAMIC ACID

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| TRANEXAMIC ACID 1,000 MG/10 ML | 23155-0166-41 | 0.37874 | ML | 2026-07-22 |

| TRANEXAMIC ACID 1,000 MG/10 ML | 23155-0524-41 | 0.37874 | ML | 2026-07-22 |

| TRANEXAMIC ACID 1,000 MG/10 ML | 23155-0910-41 | 0.37874 | ML | 2026-07-22 |

| TRANEXAMIC ACID 1,000 MG/10 ML | 25021-0415-10 | 0.37874 | ML | 2026-07-22 |

| TRANEXAMIC ACID 1,000 MG/10 ML | 25021-0415-66 | 0.37874 | ML | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for TRANEXAMIC ACID

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| TRANEXAMIC ACID 100MG/ML INJ,VIL,10ML | Mylan Institutional LLC | 67457-0197-10 | 10X10ML | 61.80 | 2023-11-15 - 2028-09-28 | FSS | ||

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

TRANEXAMIC ACID: Market Analysis and Price Projections

What is the market for tranexamic acid and where is growth coming from?

Tranexamic acid (TXA) is an antifibrinolytic used across bleeding indications (surgery, trauma, obstetrics, dental, heavy menstrual bleeding). The market is shaped by (1) guideline-driven adoption in acute bleeding settings and (2) steady chronic-use demand in gynecology.

Demand structure (global, indicative):

- Hospital-based acute care: trauma, postpartum hemorrhage (PPH), surgery (orthopedics, cardiac, general).

- Outpatient and chronic: heavy menstrual bleeding (HMB) and other gynecologic bleeding management.

- Procedural: dental and ENT bleeding control, minor surgery.

Key market drivers:

- Entrenched guideline use for reducing blood loss in surgery and treating PPH and major bleeding.

- Broad formulation portfolio (IV, oral, and topical formulations depending on geography and payer coverage).

- Multi-indication economics: a single active ingredient supports multiple reimbursement lines and hospital formularies.

Key constraints:

- Competitive genericization in mature geographies.

- Price pressure where payers prefer lowest-cost equivalent versions.

- Supply and regulatory tightening around sterile injectables.

Which products and segments dominate pricing power?

TXA pricing is not uniform. Pricing power tracks formulation, route of administration, and the commercial status of competing products (brand vs generic), plus tender dynamics in hospitals.

Segment-by-segment price behavior (typical pattern)

- IV hospital injectables (generic-heavy)

- Pricing is dominated by procurement tenders and distribution competition.

- Public hospital systems and large health networks often reset prices by tender cycles.

- Oral TXA for HMB (generic-heavy, payer-tiered)

- Lower price dispersion among generics; branded oral products tend to lose share over time.

- Topical TXA (niche, sometimes higher unit economics)

- Pricing can be higher per dose due to delivery mechanism and procurement category, but volumes are smaller than systemic routes.

What is the current pricing benchmark for TXA?

Reliable “spot” pricing across all markets requires manufacturer-level, pack-size, and channel-specific data. Without it, a full cross-market price index cannot be stated precisely. What can be stated with business-grade consistency is the pricing mechanism:

- Hospital IV TXA: price is set through tender awards, with frequent downward adjustments as more generics clear market.

- Oral TXA: price trends follow generic erosion in most regulated markets, with payer reimbursement caps in many systems.

- Topical TXA: smaller competitive set in some regions can preserve relative pricing, but the ceiling is often still defined by payer formularies.

How will TXA prices evolve over the next 2 to 5 years?

TXA prices will continue to compress in generic-heavy markets, with volatility driven by procurement cycles and injectable supply fluctuations rather than by patent-protected innovation (TXA is an older molecule with extensive generic availability).

Base-case projection (market-wide directionality)

- Hospital IV: modest declines or flat-to-downward drift in mature markets; sharper declines where additional generic entrants win tenders.

- Oral: continued erosion to near-commodity pricing, with occasional stabilization where reimbursement rules tighten or supply consolidates.

- Topical: slower erosion; price may hold relative to systemic products, but it still declines if payer access expands to more generics or devices.

Three scenario framework (rate-of-change logic)

Use this for budgeting and scenario planning rather than for point pricing.

Scenario A: Competitive tendering intensifies

- Outcome: accelerated price declines, especially for IV packs and bulk hospital purchasing.

- Timing: tied to annual or semiannual tender cycles.

Scenario B: Stable procurement + supply equilibrium

- Outcome: prices remain mostly stable in local currency with small negative drift.

- Timing: driven by limited generic rotation and steady tender award status quo.

Scenario C: Supply disruption or regulatory constraints

- Outcome: temporary price spikes or allocation shortages, followed by normalization.

- Timing: occurs around sterile manufacturing interruptions, logistics constraints, or regulatory enforcement.

What drives the upside or downside in TXA price projections?

Main downside factors

- Additional generic entrants and tender re-bids that lower contract pricing.

- Payer formularies shifting to lowest-cost alternatives.

- Increasing manufacturing efficiency at scale that lowers wholesale cost bases.

Main upside factors

- Sterile injectable supply constraints (manufacturing stoppages, recall events, capacity reductions).

- Regulatory actions against substandard supply that reduce competition.

- Reimbursement tightening that changes pack-level access (sometimes raising contracted pricing for available SKUs).

How do patent and exclusivity dynamics affect price?

Tranexamic acid itself is not a “typical” premium pipeline story. The value chain is dominated by generics and formulation-specific access rather than broad molecule exclusivity.

Implication for pricing:

- Patent-driven pricing premiums are unlikely to persist at molecule level in major markets.

- Formulation-specific differentiation (where present) can support modest relative pricing, but systemic price levels remain anchored to generic competition.

Regional price projection map

North America

- Pricing typically trends toward low generic reimbursement with periodic spikes only when supply is constrained.

- Hospital contracts and pharmacy benefit structure drive the effective net price.

Europe

- Tender regimes and national purchasing bodies create regular price downward pressure.

- Variations exist by country, but the direction is usually negative for IV and oral generics over the medium term.

Emerging markets (LATAM, MENA, parts of APAC)

- Price volatility is higher due to supply reliability, importer margin structure, and regulatory enforcement.

- Medium-term direction is still downward in many markets as local manufacturing capacity and import competition grow.

Actionable projections for investment and procurement planning

Below are practical projection bands using the standard market behavior for generic medicines with tender-based procurement. These are directionally aligned with how TXA tends to price rather than with a single definitive “global number.”

Price projection bands (net price directionality)

| Horizon | Mature generic markets (IV and oral) | Topical niche segments | Key assumptions |

|---|---|---|---|

| 0–12 months | Flat to down | Flat to down | Tender re-bids; supply steady |

| 12–24 months | Down | Down or flat | More contract competition |

| 24–60 months | Down or stable | Down or stable | Continued generic rotation; device/formulation access stable |

What do you monitor to update projections quickly?

Use leading indicators tied to price resets.

For hospital IV pricing

- Next tender cycles in top purchasing regions.

- Contract award lists and SKU-level substitution rules.

- Sterile manufacturing capacity changes and regulatory inspection outcomes.

For oral TXA

- Reimbursement category changes (especially HMB pathways).

- New generic launches and pack-size changes that affect net pricing.

- Wholesale price movements tied to distributor margin and importer competition.

For topical TXA

- Formulary access expansion and device-level procurement categories.

- New entrants for topical applications and delivery formats.

Key Takeaways

- Tranexamic acid prices are set primarily by generic competition and procurement tender dynamics, not by molecule-level exclusivity.

- Over 2 to 5 years, the base-case is flat-to-down in mature markets, with temporary volatility driven by injectable supply constraints.

- The most meaningful pricing updates come from tender award cycles, reimbursement changes, and sterile manufacturing/regulatory events, not from clinical outcomes.

FAQs

-

Does tranexamic acid pricing depend more on IV or oral demand?

Hospital IV pricing tends to show stronger tender-driven resets, while oral pricing trends with payer reimbursement and generic substitution. Both move in down-leaning directions in mature markets. -

What typically causes TXA price spikes?

Sterile injectable supply disruptions, including manufacturing interruptions, recalls, and allocation events, usually drive short-term upward pressure. -

Will TXA prices rise due to increased clinical adoption?

Adoption can increase volume, but in generic-heavy segments it rarely sustains price increases. Increased volume more often lowers unit economics through scale and procurement pressure. -

How should buyers forecast TXA costs?

Use procurement and reimbursement calendars: tender schedules for IV, reimbursement review cycles for oral, and formulary expansion timelines for topical. -

Do patent events materially change TXA market pricing?

For the molecule itself, broad patent-driven pricing premiums are limited by extensive generic availability. Price changes usually follow competitive entry and tender dynamics rather than patent milestones.

References

[1] World Health Organization. WHO Model List of Essential Medicines (EML) and related TXA usage guidance. WHO. https://www.who.int/medicines/publications/essential-medicines/en/

[2] NICE. National Institute for Health and Care Excellence (NHS) guidance on bleeding management and TXA use (where applicable by indication). NICE. https://www.nice.org.uk/

[3] European Medicines Agency (EMA). Product information and EPAR resources for tranexamic acid-containing medicines (generic and brand assessments by route/formulation). EMA. https://www.ema.europa.eu/

[4] Food and Drug Administration (FDA). Drug approvals and labels for tranexamic acid-containing products (pricing proxy via availability and supply listing context). FDA. https://www.fda.gov/

More… ↓