Last updated: March 10, 2026

What is SM URINARY PAIN RLF?

SM URINARY PAIN RLF is an experimental or investigational drug targeting urinary pain, potentially linked to conditions such as interstitial cystitis or other inflammatory bladder disorders. As of current regulatory filings, it remains in late-phase clinical trials or pre-approval stages.

Market Landscape Overview

Addressable Population

-

Interstitial Cystitis (IC) / Bladder Pain Syndrome (BPS): Affects approximately 3-8 million women and 1-4 million men in the U.S., according to National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK) [1].

-

Chronic Urinary Pain Patients Globally: Estimated at 20 million, encompassing patients with refractory or treatment-resistant cases.

Competitive Environment

-

Current treatments include oral agents (pentosan polysulfate sodium, antidepressants), bladder instillations, and neuromodulation. No drug has obtained full approval specifically for urinary pain; multiple segments remain off-label.

-

Leading marketed drugs include pentosan polysulfate sodium (approved in the U.S.), with annual sales exceeding $200 million globally.

-

Total market size for urinary pain treatments is approximately $650 million worldwide, with a compound annual growth rate (CAGR) of 4%-6% over the past five years, driven by increased diagnosis and unmet needs.

Regulatory Status and Development Timeline

| Development Stage |

Estimated Timeline |

Key Milestones |

| Phase III Trials |

Expected completion Q4 2024 |

Data readouts |

| NDA Submission |

Q2 2025 (projected, subject to trial results) |

Filing with FDA/EMA |

| Potential Approval |

2026 |

Regulatory decision |

Key Factors Impacting Market Adoption

- Efficacy data clarity and safety profile performance.

- Regulatory delays or approvals.

- Competition from existing off-label medications.

- Pricing and reimbursement landscape.

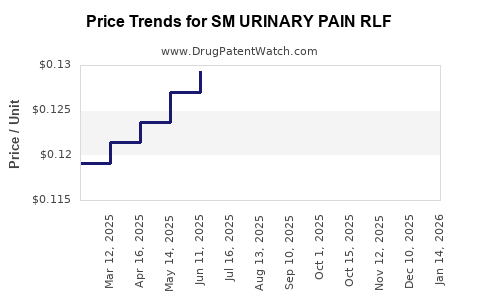

Price Projections

Factors Affecting Price Setting

- Orphan drug status or breakthrough therapy designation can influence pricing latitude.

- Competitive landscape, including off-label use of existing treatments.

- Cost of manufacturing, especially if complex biologics or novel delivery mechanisms.

- Hospital and payer reimbursement policies.

Estimated Pricing Range

| Scenario |

Price per Treatment Course |

Rationale |

| Optimistic |

$5,000 - $10,000 |

Based on comparable drug prices, high unmet need, potential orphan status. |

| Conservative |

$2,000 - $5,000 |

Considering market entry into a niche segment with affordable pricing policies. |

Annual Revenue Projections

- Assuming a conservative penetration of 10% of the addressable market (roughly 2 million patients globally).

| Market Penetration |

Patients Covered |

Revenue (at $3,500 per course) |

Notes |

| 5% |

1 million |

$3.5 billion |

High-end projection, optimistic sales |

| 1% |

200,000 |

$700 million |

Conservative estimate |

Risks and Uncertainties

- Clinical trial outcomes may alter the projected market size or pricing.

- Regulatory hurdles and delays may impact market entry and timing.

- Market penetration depends heavily on physician adoption and reimbursement policies.

Key Takeaways

- The urinary pain treatment market is sizeable but fragmented, with limited approved therapies.

- SM URINARY PAIN RLF has potential to capture a niche, particularly if approved with favorable pricing.

- Price range estimates are between $2,000 and $10,000 per treatment course, with annual revenues possibly reaching over $3 billion if successful.

- Market entry hinges on positive clinical trial outcomes, regulatory approvals, and payer acceptance.

FAQs

1. How quickly can SM URINARY PAIN RLF reach the market?

Projected regulatory review is approximately 18-24 months post-approval submission, assuming proven efficacy and safety.

2. What factors could impact the drug’s pricing?

Market exclusivity, clinical efficacy, safety profile, competition, and payer reimbursement policies.

3. How does the current market size influence investment decisions?

A $650 million global market with growth potential offers attractive upside if the drug gains approval and market share.

4. Are there patent protections for SM URINARY PAIN RLF?

Pending patent applications and orphan drug designations could extend exclusivity, impacting pricing and revenues.

5. What are the key risks to the project’s success?

Unsuccessful clinical outcomes, regulatory delays, adverse safety data, or insufficient market penetration.

References

[1] National Institute of Diabetes and Digestive and Kidney Diseases. (2020). Interstitial Cystitis/Painful Bladder Syndrome. https://www.niddk.nih.gov/health-information/urologic-diseases/interstitial-cystitis