Share This Page

Drug Price Trends for FLUOROURACIL

✉ Email this page to a colleague

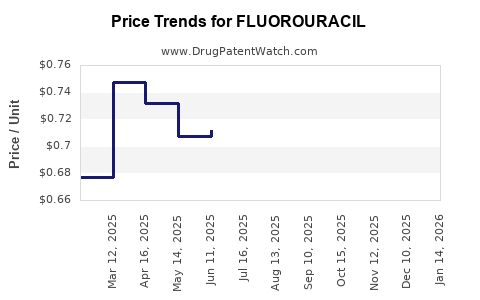

Average Pharmacy Cost for FLUOROURACIL

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| FLUOROURACIL 5% CREAM | 00378-4791-06 | 0.58529 | GM | 2026-07-22 |

| FLUOROURACIL 5% CREAM | 16714-0178-01 | 0.58529 | GM | 2026-07-22 |

| FLUOROURACIL 2% TOPICAL SOLN | 51672-4062-01 | 3.68417 | ML | 2026-07-22 |

| FLUOROURACIL 5% TOPICAL SOLN | 51672-4063-01 | 4.07840 | ML | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for FLUOROURACIL

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| FLUOROURACIL 5% CREAM,TOP | Golden State Medical Supply, Inc. | 51672-4118-06 | 40GM | 43.79 | 1.09475 | GM | 2023-12-15 - 2028-06-14 | FSS |

| FLUOROURACIL 2% SOLN,TOP | Golden State Medical Supply, Inc. | 51672-4062-01 | 10ML | 35.01 | 3.50100 | ML | 2023-06-15 - 2028-06-14 | FSS |

| FLUOROURACIL 5% SOLN,TOP | Golden State Medical Supply, Inc. | 51672-4063-01 | 10ML | 60.30 | 6.03000 | ML | 2023-06-15 - 2028-06-14 | FSS |

| FLUOROURACIL 5% SOLN,TOP | Golden State Medical Supply, Inc. | 51672-4063-01 | 10ML | 64.22 | 6.42200 | ML | 2023-06-23 - 2028-06-14 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

Fluorouracil (5-FU) Market Analysis and Price Projections

Fluorouracil (5-FU) is a widely used antimetabolite chemotherapy drug. Its primary mechanism involves inhibiting thymidylate synthase, thereby disrupting DNA synthesis and leading to cancer cell death. The drug is utilized in the treatment of various solid tumors, including colorectal, breast, stomach, and pancreatic cancers.

What is the Current Global Market Size for Fluorouracil?

The global market for fluorouracil was valued at approximately $650 million in 2023. This figure is projected to grow at a compound annual growth rate (CAGR) of 4.5% from 2024 to 2030, reaching an estimated $890 million by the end of the forecast period.

What are the Key Market Drivers for Fluorouracil?

Several factors are contributing to the sustained demand for fluorouracil:

- Increasing Incidence of Cancer: The global cancer burden continues to rise, driven by an aging population, lifestyle factors, and improved diagnostic capabilities. The World Health Organization (WHO) reported that cancer is a leading cause of death globally, with an estimated 19.3 million new cases in 2020 [1]. Cancers treated with 5-FU, such as colorectal and breast cancer, represent a significant portion of these new diagnoses.

- Established Treatment Protocol: Fluorouracil is a cornerstone therapy for several common cancers. Its efficacy and well-understood side effect profile make it a preferred choice in many treatment regimens, often used in combination with other chemotherapeutic agents and targeted therapies.

- Generic Availability and Cost-Effectiveness: As a mature drug with multiple generic manufacturers, fluorouracil is relatively cost-effective compared to newer biologic therapies. This affordability is particularly important in healthcare systems with budget constraints and in emerging markets where access to advanced treatments is limited.

- Technological Advancements in Drug Delivery: Innovations in drug delivery systems, such as liposomal formulations and prodrugs like capecitabine (which is converted to 5-FU in the body), have improved its therapeutic index by enhancing tumor targeting and reducing systemic toxicity. These advancements contribute to its continued relevance in oncology.

- Growing Healthcare Expenditure: Global healthcare spending is on an upward trend, enabling greater access to cancer treatments, including chemotherapy. This increased investment in healthcare infrastructure and services supports the market growth of established drugs like fluorouracil.

What are the Key Restraints on Fluorouracil Market Growth?

Despite its established position, the fluorouracil market faces certain constraints:

- Emergence of Targeted Therapies and Immunotherapies: The development and increasing adoption of novel treatment modalities, including targeted therapies that precisely attack cancer cells and immunotherapies that harness the patient's immune system, are beginning to displace traditional chemotherapy in some indications. These newer agents often offer improved efficacy and reduced side effects.

- Toxicity and Side Effects: Fluorouracil is associated with significant toxicities, including myelosuppression, mucositis, diarrhea, and hand-foot syndrome. These side effects can limit its use, necessitate dose reductions, and impact patient quality of life, leading some oncologists to opt for alternative treatments when available.

- Competition from Biosimilars and Generics: While generic availability is a driver of affordability, intense competition among generic manufacturers can lead to price erosion, limiting revenue growth for individual companies. The market is highly fragmented with numerous suppliers.

- Stringent Regulatory Approval Processes: While 5-FU itself is long-established, new formulations or combination therapies involving it still undergo rigorous regulatory review, which can delay market entry and increase development costs.

What is the Regional Market Distribution for Fluorouracil?

The fluorouracil market exhibits distinct regional dynamics:

- North America: This region, comprising the United States and Canada, is a major market due to a high cancer incidence, advanced healthcare infrastructure, and substantial investment in cancer research and treatment. The presence of major pharmaceutical manufacturers and a high patient population undergoing chemotherapy contribute to its market share.

- Europe: Similar to North America, Europe has a well-developed healthcare system and a significant patient pool. Countries like Germany, the UK, France, and Italy represent key markets, with established reimbursement policies supporting chemotherapy use.

- Asia-Pacific: This is the fastest-growing regional market. Factors driving this growth include the rapidly increasing incidence of cancer, expanding healthcare access, growing disposable incomes, and the presence of a large generic manufacturing base, particularly in India and China. Government initiatives to improve healthcare access are also playing a crucial role.

- Latin America: This region shows moderate growth, influenced by improving healthcare infrastructure and increasing awareness about cancer treatment options. Brazil and Mexico are significant contributors to this market.

- Middle East & Africa: This region represents a smaller market share but is expected to witness steady growth. Factors include increasing healthcare investments and a growing demand for cancer treatments.

What are the Price Trends and Projections for Fluorouracil?

The pricing of fluorouracil is influenced by several factors, primarily its status as a generic drug.

- Current Pricing: The average wholesale price (AWP) for a standard 500mg vial of fluorouracil typically ranges from $10 to $25. However, actual acquisition costs for healthcare providers can vary significantly based on volume discounts, negotiated contracts with manufacturers and distributors, and formulary placement within hospital systems or pharmacy benefit manager agreements. Prices can fluctuate based on supply chain dynamics, raw material costs, and the competitive landscape among generic producers.

- Price Projections: The price of fluorouracil is expected to remain relatively stable over the next several years, with minor fluctuations. The CAGR for price is projected to be between 1% and 3% from 2024 to 2030.

Factors influencing price stability and minor increases:

- Intense Generic Competition: The high number of manufacturers producing generic 5-FU creates a highly competitive environment, which typically suppresses prices. This prevents significant price hikes.

- Manufacturing Costs: While relatively low, the cost of active pharmaceutical ingredients (APIs), manufacturing processes, quality control, and packaging represent baseline costs that can experience minor upward pressure due to inflation or supply chain disruptions.

- Regulatory Compliance: Adherence to Good Manufacturing Practices (GMP) and other regulatory standards adds to manufacturing overhead. Any changes in these requirements could subtly influence production costs.

- Supply Chain Resilience: Episodes of drug shortages or supply chain disruptions, though not expected to be widespread for 5-FU given its mature status, can temporarily create localized price increases or affect availability.

- Demand-Side Stability: While overall cancer incidence increases, the demand for 5-FU is also tempered by the adoption of newer therapies. This balance is expected to maintain a relatively stable demand-supply dynamic for 5-FU in its established indications.

- Emergence of Value-Based Pricing (Limited Impact): While value-based pricing models are gaining traction in oncology, they are less likely to significantly impact the price of a long-established, low-cost generic like 5-FU, which is often used as a component of combination therapy rather than as a standalone, high-cost innovator drug.

Example of Price Fluctuation (Hypothetical):

In early 2023, a minor disruption in the supply of a key precursor chemical for 5-FU led to a temporary increase in the AWP of certain generic 500mg vials by approximately 5-7% for a period of three months before stabilizing. Conversely, the entry of a new, highly efficient generic manufacturer in late 2023 led to a slight downward pressure of around 3-4% on average acquisition costs for a short period.

What are the Key Market Segments for Fluorouracil?

The fluorouracil market can be segmented based on:

- Indication:

- Colorectal Cancer

- Breast Cancer

- Stomach Cancer

- Pancreatic Cancer

- Other Cancers (e.g., Head and Neck, Anal)

- Route of Administration:

- Intravenous (IV)

- Topical (used for skin conditions like actinic keratosis)

- End-User:

- Hospitals

- Oncology Clinics

- Specialty Pharmacies

- Retail Pharmacies

What are the Key Competitive Landscape Factors?

The fluorouracil market is characterized by a fragmented competitive landscape with numerous generic manufacturers. Key players include:

- Teva Pharmaceutical Industries Ltd.

- Fresenius Kabi AG

- Hikma Pharmaceuticals PLC

- Accord Healthcare Ltd.

- Sun Pharmaceutical Industries Ltd.

- Eisai Co., Ltd. (via its capecitabine prodrug)

- Various Chinese and Indian generic manufacturers

Competition primarily revolves around:

- Price: As a generic drug, price is a critical differentiator.

- Product Quality and Reliability: Consistent quality and a reliable supply chain are essential.

- Manufacturing Capacity: Ability to meet global demand.

- Regulatory Compliance: Adherence to FDA, EMA, and other health authority standards.

Key Takeaways

- The global fluorouracil market is projected to grow at a CAGR of 4.5% from 2024 to 2030, reaching approximately $890 million.

- Market growth is driven by rising cancer incidence and fluorouracil's established role in treatment protocols, supported by its cost-effectiveness.

- The emergence of targeted therapies and immunotherapies, alongside the drug's toxicity, are key market restraints.

- North America and Europe are the largest markets, while the Asia-Pacific region exhibits the fastest growth.

- Fluorouracil prices are expected to remain stable with minor annual increases of 1-3% due to intense generic competition and balanced supply-demand dynamics.

- The market is fragmented, with a significant number of generic manufacturers competing primarily on price and product reliability.

Frequently Asked Questions

1. What is the primary use of fluorouracil in cancer treatment?

Fluorouracil is primarily used as an antimetabolite chemotherapy drug to inhibit DNA synthesis, thereby killing cancer cells. It is a cornerstone therapy for colorectal, breast, stomach, and pancreatic cancers, among others.

2. How does capecitabine relate to fluorouracil?

Capecitabine is an oral prodrug that is converted into fluorouracil within the body, primarily in tumor tissues. It is an alternative oral formulation designed to improve drug delivery and potentially reduce systemic toxicity compared to intravenous 5-FU.

3. What are the most common severe side effects of fluorouracil?

Severe side effects include myelosuppression (low blood cell counts), mucositis (inflammation of the mucous membranes), diarrhea, and hand-foot syndrome (pain, redness, and swelling of the hands and feet).

4. Is fluorouracil still considered a frontline treatment for any major cancers?

Yes, fluorouracil remains a frontline treatment option, often in combination regimens, for several major cancers including certain stages of colorectal cancer and breast cancer. Its role is evolving with the advent of new therapies, but it maintains its importance in established protocols.

5. What is the impact of generic competition on the price of fluorouracil?

Intense competition among multiple generic manufacturers has led to significant price erosion for fluorouracil over the years, making it a cost-effective chemotherapy option. This competition is expected to keep prices relatively stable, with only modest increases driven by manufacturing and supply chain factors.

Citations

[1] World Health Organization. (2021). Cancer. Retrieved from https://www.who.int/news-room/fact-sheets/detail/cancer

More… ↓