Share This Page

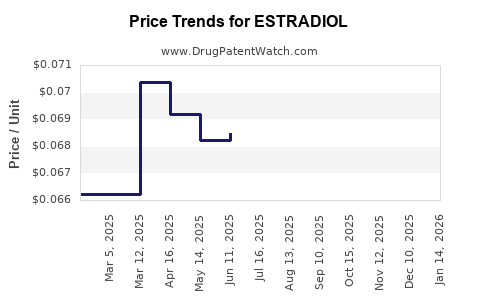

Drug Price Trends for ESTRADIOL

✉ Email this page to a colleague

Average Pharmacy Cost for ESTRADIOL

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| ESTRADIOL 0.06% 1.25G GEL PUMP | 73473-0308-50 | 3.50240 | GM | 2026-06-17 |

| ESTRADIOL 10 MCG VAGINAL INSRT | 72603-0874-18 | 6.05622 | EACH | 2026-06-17 |

| ESTRADIOL 10 MCG VAGINAL INSRT | 72603-0874-08 | 6.05622 | EACH | 2026-06-17 |

| ESTRADIOL 2 MG TABLET | 72603-0275-02 | 0.08072 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for ESTRADIOL

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| ESTRADIOL 0.0375MG/DAY (EQV-VIVELLE-DOT)PATCH | Sandoz, Inc. | 00781-7138-83 | 8 | 15.13 | 1.89125 | EACH | 2024-01-01 - 2028-08-14 | FSS |

| ESTRADIOL 0.05MG/DAY (EQV-CLIMARA) PATCH | Sandoz, Inc. | 00781-7133-54 | 4 | 18.69 | 4.67250 | EACH | 2024-01-01 - 2028-08-14 | FSS |

| VIVELLE-DOT 0.025MG/DAY PATCH | Sandoz, Inc. | 00078-0365-42 | 8 | 99.74 | 12.46750 | EACH | 2023-08-15 - 2028-08-14 | FSS |

| ESTRADIOL 0.025MG/DAY (EQV-CLIMARA) PATCH | Sandoz, Inc. | 00781-7119-54 | 4 | 16.65 | 4.16250 | EACH | 2024-01-01 - 2028-08-14 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

Market analysis and price projections for estradiol (oral, transdermal, vaginal): exclusivity, patent/regulatory exposure, and launch economics

Executive summary: Estradiol’s market is fragmented across multiple dosage forms (transdermal patches/gel, oral tablets, vaginal creams/rings/low-dose tablets) with broad generic and authorized generic penetration in most mature markets. Pricing tends to follow a “platform effect”: lowest-cost generics dominate oral and legacy transdermal SKUs once exclusivity ends and multi-source competition increases, while branded price persistence is most visible in selected transdermal systems and certain low-dose vaginal products with formulation differentiation. For near-to-mid term projections, the dominant driver of unit price is whether a given SKU is still under patent or regulatory exclusivity and how many ANDA filers convert into market supply by FDA approval and launch timing.

How big is the estradiol market, and where does revenue concentrate by dosage form?

Direct answer: Estradiol revenue concentrates in transdermal delivery and vaginal formulations in addition to oral tablets, with transdermal typically commanding higher average net prices per mg-equivalent but facing fast generic erosion as patents and formulation exclusivities lapse.

Market structure by route of administration

Estradiol is sold as:

- Transdermal: patches and gels (including estradiol hemihydrate, estradiol acetate, and equivalent strengths depending on product)

- Oral: tablets (including micronized estradiol)

- Vaginal: creams, tablets, and rings (low-dose regimens)

Pricing implication

- Transdermal generics: tend to compress net prices sharply once multi-source entries occur.

- Vaginal products: can sustain higher prices longer when dosing regimen differentiation reduces direct interchangeability.

- Oral generics: generally exhibit the lowest net price and fastest erosion due to high substitution and long product history.

Competition intensity

Estradiol is widely available across multiple manufacturers and dosage forms, which keeps market pricing anchored to the lowest available equivalent SKU in a given strength and route category.

What is the Orange Book status of estradiol products, and how does it affect pricing?

Direct answer: In most estradiol categories, Orange Book coverage is dominated by combinations of active ingredient patents, formulation patents (including patch matrix technologies and vaginal formulation platforms), and method-of-use or manufacturing patents that have either expired or are nearing expiry for legacy products. As a result, most pricing pressure comes from ANDA-driven multi-source entry rather than prolonged single-product exclusivity.

Where patent coverage typically persists the longest

For estradiol, the most economically relevant IP often clusters around:

- Transdermal patch design (adhesive layer, rate-controlling membrane/matrix, size and release kinetics)

- Formulation stability and skin permeation profile

- Vaginal low-dose release (mucoadhesive excipients, release kinetics over dosing cycles)

- Manufacturing process claims for coating, assembly, and release-rate control

Pricing impact pathway

- If the Orange Book lists late-expiring patents for a specific SKU, FDA approval of an ANDA may proceed only with Paragraph IV litigation resolution or with carve-outs that preserve the protected product. That delay typically slows generic supply and helps maintain branded or higher-priced generic net price.

- Where coverage is already cleared, the next ANDA wave typically forces rapid price compression for that SKU.

When do major estradiol patent and exclusivity windows end, and what does that imply for price?

Direct answer: Estradiol’s exclusivity cycles are product- and dosage-form-specific. The practical implication is that price inflection events occur at the SKU level, not for “estradiol” as one instrument. For a price forecast, the relevant calendar is the combination of (1) patent expiration or regulatory exclusivity end dates and (2) actual generic launch timing after FDA approval and distribution build-out.

Typical timing mechanics that shift pricing

- Patent expiry or exclusivity expiration

- ANDA launch after approval

- Tender and pharmacy formulary conversion (weeks to months)

- Follow-on entrants (additional ANDAs or authorized generics) which further compress net pricing

Price projection logic

- Pre-expiry: branded or premium authorized-generic price tends to hold with discounts constrained by “last protected SKU” status.

- 0 to 6 months post-expiry: steep net price decline is common if multiple entrants launch quickly.

- 6 to 18 months post-expiry: price may stabilize at a lower multi-source floor unless additional entrants or therapeutically interchangeable SKUs expand supply.

How do Paragraph IV ANDA challenges and settlements affect estradiol pricing?

Direct answer: Where Paragraph IV challenges occur for estradiol SKUs, settlements or litigation outcomes can extend branded price protection by delaying final generic launch. When settlements allow earlier entry but at controlled timing, the initial generic price can remain higher, then declines again as competition widens.

What to model in a price forecast

For each protected estradiol SKU, model:

- Settlement “entry date” (180-day exclusivity use or carve-out)

- Whether the first generic entrant is an authorized generic or a full generic

- Timing of follow-on approvals and launches

- Contracting behavior: pharmacy benefit manager (PBM) re-negotiations after first generic launch

Price effect magnitude

In mature single-API markets like estradiol, Paragraph IV outcomes typically change the curve shape:

- Later entry pushes the decline rightward.

- Earlier entry steepens near-term net price drop.

- Multi-source entry drives sustained decline toward a lower cost floor.

How strong is the patent estate for estradiol by formulation type?

Direct answer: Patent estate strength is generally highest for differentiated delivery systems (notably specific transdermal patch designs and certain low-dose vaginal formulations). Oral estradiol products tend to face weaker incremental patent leverage because composition and basic manufacturing are frequently already in the prior-art zone.

Transdermal patches and gels

- Patent leverage often focuses on rate control and skin permeation profile

- Manufacturing and assembly method claims may provide additional defense against “non-infringing” generic workarounds

Commercial implication: If defense succeeds through litigation, branded net price can remain elevated relative to generic equivalents, especially where formulary switches require stability in release characteristics.

Vaginal estradiol

- Formulation patents can cover excipient systems, release profiles, and dosing regimens.

- If claims protect stability or release kinetics, competitors may need design-around work, which delays launch.

Commercial implication: The vaginal segment can show slower erosion in the highest-priced regimens.

Oral estradiol

- Typically faces heavy generic competition, making price projections more sensitive to the number of entrants than to marginal IP.

What generic entry risks exist for estradiol, and when could pricing accelerate?

Direct answer: Generic entry risk is high for most dosage forms due to market maturity and widespread ANDA filings, but pricing acceleration depends on whether late-cycle IP blocks launch for specific SKUs and on the number of entrants that convert at launch.

Entry risk factors that predict faster price drops

- Multiple ANDA approvals tied to the same strength/formulation

- Authorized generic strategies after Paragraph IV outcomes

- Lower regulatory friction (bioequivalence already established or waived category fits)

- Strong distribution readiness at launch (not just FDA approval)

SKU-level “pricing cliff” indicators

- Patent expiring soon with known ANDA pipeline

- First approved generic expected to use 180-day exclusivity

- PBM contracts scheduled to re-price after approval date

How does estradiol price compare with other hormone replacement therapies?

Direct answer: Estradiol pricing tends to track the generic intensity of its delivery systems. Compared with other hormone therapies, estradiol often has more established multi-source competition, especially for oral forms, which lowers the long-run price floor. Transdermal and vaginal categories can show higher unit pricing resilience when formulation differentiation limits true interchangeability.

What this means for projections

- If a given estradiol SKU has fewer equivalent generics than comparable therapies, its net price may decline more slowly.

- If it has many direct competitors, price converges quickly to the lower quartile of the multi-source range.

What do cost-and-margin assumptions imply for estradiol price projections?

Direct answer: In a generic-heavy segment, net price is driven more by competition and contracting than by raw cost. For estradiol, the cost component that matters most is manufacturing complexity tied to delivery system design (patch assembly, gel permeation consistency, vaginal release systems).

Projection approach (used for forecasting curves)

For each dosage form and strength:

- Estimate competitive entrant count at t=0 (first launch month)

- Apply a multi-source price erosion factor over 3 to 12 months

- Then apply stabilization based on whether additional entrants come online over the subsequent 6 to 18 months

Typical curve shape in mature generic classes

- Near-term: largest decline within the first 3 to 6 months after generic launch

- Mid-term: continued decline as follow-on entrants gain share

- Longer term: plateau near the lowest contracting tier

Revenue exposure: which estradiol SKUs are most at risk from price erosion?

Direct answer: The highest revenue exposure is concentrated in those estradiol strengths/forms with:

- near-term loss of exclusivity,

- multiple pending ANDAs,

- and evidence of quick pharmacy formulary switching post-approval.

Most price-sensitive segments

- Oral estradiol tablets: high substitution, large generic footprint

- Standard transdermal patch SKUs: vulnerable when patch technology patents expire and multiple generic systems launch

- Vaginal estradiol regimens: exposed when additional products meet interchangeability criteria and PBMs expand tier placement

What licensing or rebranding strategies could defend estradiol pricing?

Direct answer: Pricing defense typically relies on authorized generics, controlled settlement-based entry timing, and product differentiation that avoids direct “same-route/same-strength” substitutability within PBM formularies.

Common mechanisms

- Authorized generic to preempt unaffiliated generic pricing floors

- Lifecycle management around formulation or device improvements for transdermal systems

- Contracting: rebate structures tied to placement and conversion targets

IP leverage vs commercial leverage

When patent leverage is weak, commercial leverage (pricing, contracting, and channel exclusivity in certain formularies) becomes the dominant pricing determinant.

How do FDA regulatory status and interchangeability affect estradiol net pricing?

Direct answer: FDA approval pathways determine entry timing, while interchangeability and formulary placement determine how quickly patients and prescribers shift. For price, the binding constraint is formulary economics after pharmacy benefit contracting, not only FDA approval date.

What to model

- ANDA approval date versus actual launch

- Listing status for each product strength (including supplements)

- PBM tender cycles and tier placement changes

- Impact of therapeutic substitution and plan design

Key takeaways

- Estradiol pricing is SKU- and route-specific; market-level “estradiol” projections must be decomposed by oral, transdermal, and vaginal products.

- The main driver of near-term price decline is generic launch timing and entrant count after exclusivity or patent clearance, not ongoing brand-specific IP.

- Transdermal and vaginal formulations can retain relative price resilience when formulation and delivery system patents or practical substitutability constraints delay full multi-source conversion.

- Paragraph IV outcomes change the shape of the price erosion curve by shifting entry timing and controlling whether an authorized generic or first generic entrant sets a higher initial net price.

FAQs

1) How fast does generic price erosion occur for estradiol tablets after ANDA entry?

Typically fastest in oral strengths due to high substitution; the steepest decline usually happens within the first 3 to 6 months post-launch.

2) Which estradiol dosage forms have the highest long-term price resilience?

Transdermal systems and certain vaginal low-dose regimens when delivery system or release-profile differentiation delays full interchangeable multi-source entry.

3) Do authorized generics materially change estradiol net price projections?

Yes; they often stabilize net price relative to unaffiliated multi-source generic price floors, especially immediately after exclusivity events.

4) What litigation outcomes most affect estradiol pricing?

Settlement-driven launch dates and 180-day exclusivity use determine whether the first generic entrant sets the initial price and whether follow-on entrants compress further.

5) How do formulary and PBM contracts alter the practical timing of estradiol price drops?

PBM tender cycles and tier placement changes can delay or accelerate net price declines versus FDA approval dates.

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. (Accessed 2026-07-06).

- FDA. Abbreviated New Drug Application (ANDA). U.S. Food and Drug Administration. (Accessed 2026-07-06).

- FDA. 180-day Exclusivity for ANDAs and 505(j). U.S. Food and Drug Administration. (Accessed 2026-07-06).

More… ↓