Share This Page

Drug Price Trends for ASPIRIN-DIPYRIDAM ER

✉ Email this page to a colleague

Average Pharmacy Cost for ASPIRIN-DIPYRIDAM ER

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| ASPIRIN-DIPYRIDAM ER 25-200 MG | 68462-0405-60 | 0.57270 | EACH | 2026-06-17 |

| ASPIRIN-DIPYRIDAM ER 25-200 MG | 00904-7056-99 | 0.57270 | EACH | 2026-06-17 |

| ASPIRIN-DIPYRIDAM ER 25-200 MG | 16714-0964-01 | 0.57270 | EACH | 2026-06-17 |

| ASPIRIN-DIPYRIDAM ER 25-200 MG | 43598-0339-60 | 0.57270 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Aspirin-Dipyridamole ER: Market Outlook and Pricing Projections

This analysis examines the current market landscape and projects future pricing for Aspirin-Dipyridamole Extended-Release (ER), a combination therapy primarily indicated for stroke prevention in patients at high risk. The market is influenced by the prevalence of cardiovascular disease, the availability of competing antithrombotic agents, patent expiration timelines, and evolving clinical guidelines. Price projections consider manufacturing costs, R&D investment recovery, market demand, and competitive pressures.

What is the current market size and growth trajectory for Aspirin-Dipyridamole ER?

The global market for Aspirin-Dipyridamole ER is a niche segment within the broader antithrombotic market. While precise standalone figures for the ER formulation are not extensively delineated in public reports, its usage is directly tied to the prevention of ischemic stroke and transient ischemic attacks (TIAs). The prevalence of these conditions, driven by aging populations and the rise of risk factors like hypertension, diabetes, and hyperlipidemia, underpins the demand for effective preventative therapies.

Globally, cardiovascular diseases remain a leading cause of mortality and morbidity, with stroke accounting for a significant portion. According to the World Health Organization, stroke is the second leading cause of death and disability worldwide [1]. This persistent and growing burden of stroke directly translates to a sustained demand for antithrombotic agents, including Aspirin-Dipyridamole ER.

The market growth for this specific formulation is expected to be moderate, influenced by several factors:

- Established Efficacy: Aspirin-Dipyridamole ER has a long-standing track record and established efficacy in preventing recurrent ischemic strokes, particularly in patients who may not tolerate or respond adequately to single antiplatelet therapy [2].

- Competition: The antithrombotic market is highly competitive, with numerous agents available, including other antiplatelets (e.g., clopidogrel, ticagrelor), anticoagulants (e.g., direct oral anticoagulants - DOACs), and combination therapies. This competition exerts downward pressure on pricing and market share for older or less innovative products.

- Generic Penetration: As patent protections expire or have expired for originator formulations, generic versions of Aspirin-Dipyridamole ER have become available. Generic entry significantly reduces average selling prices and can fragment market share.

- Evolving Guidelines: Clinical guidelines from organizations like the American Heart Association/American Stroke Association (AHA/ASA) and the European Stroke Organisation (ESO) evolve based on new clinical trial data. These guidelines can influence prescribing patterns, favoring newer agents or different therapeutic strategies if proven superior or more cost-effective [3].

Estimates suggest the global antithrombotic drug market, within which Aspirin-Dipyridamole ER resides, was valued at approximately USD 35 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 4-6% over the next five to seven years [4]. The contribution of Aspirin-Dipyridamole ER to this total is a fraction, likely in the hundreds of millions of dollars, with its growth trajectory more subdued than newer drug classes like DOACs.

What are the key drivers and restraints for Aspirin-Dipyridamole ER market adoption?

Key Market Drivers:

- High Prevalence of Ischemic Stroke: The persistent and increasing incidence of ischemic stroke globally, particularly in aging populations, creates a consistent demand for effective preventative treatments. Aspirin-Dipyridamole ER is a recognized option for select patient populations.

- Established Safety and Efficacy Profile: Decades of clinical use have established the efficacy of aspirin and dipyridamole individually and in combination for stroke prevention. The ER formulation offers convenience and potentially improved tolerability compared to immediate-release versions.

- Cost-Effectiveness of Generic Formulations: The availability of affordable generic Aspirin-Dipyridamole ER can drive adoption in healthcare systems with budget constraints or where cost is a significant consideration for long-term management of stroke risk.

- Specific Patient Populations: Certain patient subgroups may benefit from Aspirin-Dipyridamole ER where other agents are contraindicated or less effective. This includes patients with specific contraindications to other antiplatelet agents or those who have failed on other therapies.

- Combination Therapy Benefits: The synergistic effect of aspirin (inhibiting cyclooxygenase) and dipyridamole (inhibiting phosphodiesterase and adenosine reuptake) provides a dual mechanism of antiplatelet aggregation and vasodilation, which can be advantageous in certain stroke prevention scenarios.

Key Market Restraints:

- Competition from Novel Antithrombotics: The introduction and widespread adoption of DOACs (e.g., apixaban, rivaroxaban, dabigatran) for stroke prevention in atrial fibrillation, and their potential use in other thrombotic conditions, represent significant competition. DOACs often offer simpler dosing regimens and potentially different safety profiles.

- Availability of Newer Antiplatelets: Newer P2Y12 inhibitors like ticagrelor and prasugrel provide potent antiplatelet activity and have demonstrated efficacy in specific cardiovascular indications, potentially shifting prescribing habits.

- Patent Expirations and Generic Erosion: The primary patents for the originator formulation of Aspirin-Dipyridamole ER have expired, leading to the entry of multiple generic manufacturers. This significantly reduces prices and profit margins for both branded and generic products.

- Adherence Challenges: While ER formulations aim to improve adherence, managing multiple medications can still be a challenge for patients. The regimen of taking Aspirin-Dipyridamole ER, often alongside other cardiovascular medications, requires consistent patient engagement.

- Adverse Event Profile: Potential side effects such as headache (common with dipyridamole), gastrointestinal bleeding (associated with aspirin), and dizziness can limit its use in certain patients.

- Evolving Clinical Guidelines: As new evidence emerges, clinical guidelines may shift recommendations, potentially prioritizing newer agents or combination therapies if they demonstrate superior outcomes or improved safety profiles.

What is the patent landscape for Aspirin-Dipyridamole ER?

The patent landscape for Aspirin-Dipyridamole ER is characterized by the expiration of primary composition of matter and formulation patents related to the originator product. The original product, Aggrenox (Aspirin/Dipyridamole ER), was developed by Boehringer Ingelheim.

- Original Patents: The foundational patents covering the specific extended-release formulation of aspirin and dipyridamole, designed for concurrent administration to reduce the frequency of headaches associated with dipyridamole, have expired. These patents were crucial for protecting the initial market exclusivity of the branded product. For instance, U.S. Patent No. 5,705,196, which claims a pharmaceutical composition comprising an extended-release matrix containing dipyridamole and an immediate-release component containing aspirin, has long since expired.

- Generic Entry: Following the expiration of these key patents, numerous pharmaceutical companies have successfully developed and obtained regulatory approval for generic versions of Aspirin-Dipyridamole ER. This has led to widespread generic competition in major markets like the United States and Europe.

- Manufacturing Process Patents: While composition of matter patents have expired, there may still be active patents related to specific manufacturing processes, polymorphs, or novel formulations that could offer some degree of intellectual property protection for specific manufacturers. However, these are typically less comprehensive than original compound patents and may be harder to enforce against competitors developing independent manufacturing routes.

- Regulatory Exclusivity: In addition to patent protection, regulatory exclusivity periods granted by agencies like the U.S. Food and Drug Administration (FDA) or the European Medicines Agency (EMA) upon initial drug approval can provide a period of market protection. However, these are separate from patent terms and also expire.

The active patent life for the core Aspirin-Dipyridamole ER combination therapy has largely concluded, paving the way for sustained generic competition. New patent filings are likely to focus on incremental innovations, such as novel delivery systems, synergistic combinations with other agents, or new therapeutic indications, rather than the core drug combination itself.

What are the projected pricing trends for Aspirin-Dipyridamole ER?

Pricing projections for Aspirin-Dipyridamole ER are heavily influenced by the dominance of generic competition and the cost-containment pressures within healthcare systems.

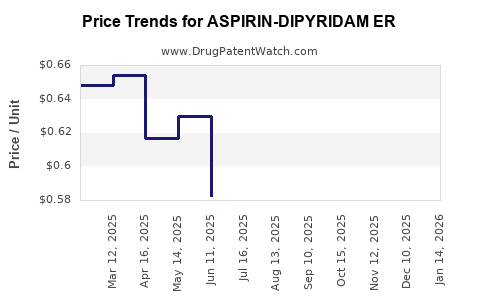

- Current Pricing: The average selling price (ASP) of branded Aspirin-Dipyridamole ER has significantly decreased since the advent of generics. The price of generic Aspirin-Dipyridamole ER varies widely based on the manufacturer, the region, the pharmacy, and the insurance formulary. In the U.S., a prescription for 60 capsules (a one-month supply) of generic Aspirin-Dipyridamole ER can range from approximately \$15 to \$50, with significant variations. Branded versions, where still available, would command a substantially higher price but have limited market share.

- Downward Pressure: The primary driver of pricing is the intense competition among generic manufacturers. As more companies enter the market, prices are driven down to competitive levels, often reflecting manufacturing costs plus a modest profit margin. This trend is expected to continue.

- Price Stability for Generics: Once generic prices stabilize, they tend to remain relatively consistent, with minor fluctuations due to supply chain dynamics, raw material costs, or promotional activities by specific manufacturers. Significant price increases are unlikely unless there is a substantial disruption in supply or a consolidation of manufacturers.

- Impact of Payer Negotiations: Insurance companies and pharmacy benefit managers (PBMs) play a crucial role in price negotiation. They often favor the lowest-cost generic option, further reinforcing downward price pressure. Formulary placement and preferred generic status can influence which generic manufacturer gains market share, but this typically occurs at a lower price point.

- Potential for Slight Increases in Specific Scenarios: While overall trends are downward, niche markets or specific patient populations where generic availability is limited, or where a particular manufacturer offers a superior quality or packaging, might see slightly higher prices. However, these scenarios are unlikely to influence the overall market trend.

- Comparison to Newer Agents: Aspirin-Dipyridamole ER, especially its generic forms, is significantly more affordable than newer antithrombotic agents like DOACs. For instance, a one-month supply of a DOAC can range from \$200 to \$400 or more, depending on the specific drug and insurance. This cost differential makes Aspirin-Dipyridamole ER a more accessible option for cost-conscious patients and healthcare systems.

Projected Pricing Trend: Over the next 3-5 years, the pricing for generic Aspirin-Dipyridamole ER is expected to remain relatively stable, with a gradual decline of 1-3% annually due to ongoing competitive pressures. Branded versions will continue to lose market share and remain at premium prices for a diminishing segment of the market.

What are the regulatory considerations and market access challenges?

Regulatory considerations and market access for Aspirin-Dipyridamole ER are primarily shaped by its established status as a generic medication and the evolving landscape of antithrombotic therapies.

- Generic Drug Approvals: In major markets like the U.S. and Europe, generic versions of Aspirin-Dipyridamole ER have undergone Abbreviated New Drug Application (ANDA) or similar European regulatory processes. This involves demonstrating bioequivalence to the reference listed drug (RLD), meaning the generic drug exhibits the same rate and extent of absorption. The approval process for generics is generally faster and less expensive than for novel drugs.

- Quality and Manufacturing Standards: All manufacturers of Aspirin-Dipyridamole ER, whether branded or generic, must adhere to stringent Good Manufacturing Practices (GMP) as mandated by regulatory bodies such as the FDA and EMA. This ensures product quality, safety, and consistency. Regular inspections and adherence to pharmacopeial standards (e.g., USP, EP) are critical.

- Labeling and Indication Alignment: Generic labels must be consistent with the RLD's approved labeling at the time of generic approval, including indications, dosage, contraindications, and warnings. However, generic manufacturers cannot independently add new indications or make significant changes to the approved labeling without going through a full regulatory review process, which is rarely pursued for older generics.

- Market Access and Reimbursement:

- Payer Coverage: Aspirin-Dipyridamole ER, particularly generic forms, generally enjoys broad market access and favorable reimbursement from payers (insurance companies, PBMs, national health services) due to its established efficacy, safety profile, and cost-effectiveness compared to newer alternatives.

- Formulary Placement: It is typically listed on most formularies, often as a preferred or cost-effective option for stroke prevention. However, payer policies can vary, and some may require step therapy, where patients must try a lower-cost alternative (if one exists and is clinically appropriate) before Aspirin-Dipyridamole ER is covered.

- Cost-Containment Measures: Healthcare systems globally are focused on cost containment. This means that while Aspirin-Dipyridamole ER is generally accessible, payers will actively steer patients toward the lowest-cost generic options.

- Clinical Guideline Influence: Market access can be indirectly influenced by clinical guidelines. If guidelines strongly recommend newer agents over older ones for specific patient populations, demand for Aspirin-Dipyridamole ER may decrease, impacting its favorable reimbursement status over time.

- Post-Market Surveillance: Like all medications, Aspirin-Dipyridamole ER is subject to post-market surveillance to monitor for any unexpected safety issues. Regulatory agencies rely on adverse event reporting systems (e.g., FAERS in the U.S.) to detect potential problems.

The primary market access challenge is not regulatory approval, which is well-established for generics, but rather maintaining market share against the continuous influx of newer, potentially more advanced therapeutic options and managing price erosion in a highly competitive generic environment.

What is the competitive landscape for Aspirin-Dipyridamole ER?

The competitive landscape for Aspirin-Dipyridamole ER is multifaceted, encompassing both direct generic competitors and broader classes of antithrombotic agents.

Direct Competitors (Generic Aspirin-Dipyridamole ER Manufacturers):

The market for generic Aspirin-Dipyridamole ER is highly fragmented, with numerous pharmaceutical companies producing and distributing their versions. Key players in the generic pharmaceutical space globally are likely to be among the suppliers. These include:

- Major Generic Manufacturers: Companies such as Teva Pharmaceutical Industries, Mylan (now Viatris), Sun Pharmaceutical Industries, Aurobindo Pharma, Cipla, and Accord Healthcare are active in the global generic market and likely offer Aspirin-Dipyridamole ER.

- Regional Manufacturers: Smaller, regional manufacturers may also compete, particularly in specific geographic markets.

The competition among these generic manufacturers is primarily based on:

- Price: This is the most significant competitive factor. Manufacturers compete by offering the lowest prices to secure contracts with wholesalers, distributors, and pharmacy benefit managers.

- Supply Chain Reliability: Consistent availability and reliable delivery are crucial.

- Product Quality and Compliance: Adherence to GMP standards and consistent product quality are table stakes.

- Marketing and Distribution Reach: Companies with broader distribution networks and established relationships with payers and pharmacies have an advantage.

Indirect Competitors (Broader Antithrombotic Market):

Aspirin-Dipyridamole ER competes within the broader antithrombotic market. The primary indirect competitors include:

- Single Antiplatelet Agents:

- Aspirin: Still widely used as a monotherapy for primary and secondary prevention of cardiovascular events.

- P2Y12 Inhibitors: Clopidogrel (Plavix and generics), Prasugrel (Effient and generics), Ticagrelor (Brilinta and generics). These are potent antiplatelet agents, particularly used in acute coronary syndromes and after percutaneous coronary intervention.

- Direct Oral Anticoagulants (DOACs):

- Factor Xa Inhibitors: Apixaban (Eliquis), Rivaroxaban (Xarelto), Edoxaban (Savaysa).

- Direct Thrombin Inhibitors: Dabigatran (Pradaxa). DOACs are increasingly the preferred agents for stroke prevention in non-valvular atrial fibrillation, offering convenience and a different risk-benefit profile compared to warfarin and older antiplatelet/anticoagulant combinations.

- Warfarin: A vitamin K antagonist anticoagulant that has been a standard of care for decades but requires regular monitoring due to its narrow therapeutic index and numerous drug/food interactions.

- Combination Therapies: Other dual antiplatelet therapy (DAPT) regimens involving aspirin plus a P2Y12 inhibitor are common in specific cardiovascular indications.

The competitive advantage of Aspirin-Dipyridamole ER lies in its established efficacy for secondary stroke prevention at a significantly lower cost than many newer agents. However, its market share is continually challenged by the broad utility and favorable profiles of DOACs in specific indications, and the potent antiplatelet effects of newer P2Y12 inhibitors in high-risk cardiovascular patients.

Key Takeaways

The market for Aspirin-Dipyridamole ER is characterized by mature generic competition and stable, albeit moderate, demand driven by the persistent prevalence of ischemic stroke. Key market drivers include its established efficacy and the cost-effectiveness of generic formulations, particularly for secondary stroke prevention. Conversely, the market faces restraints from competition by novel antithrombotic agents, notably DOACs, and the erosion of pricing due to generic entry. The patent landscape is largely defined by the expiration of original protections, leading to a fragmented generic market. Pricing for generic Aspirin-Dipyridamole ER is expected to remain stable with slight downward pressure, significantly lower than newer alternatives. Regulatory considerations are straightforward for generics, focusing on bioequivalence and GMP compliance, and market access is generally favorable due to cost-effectiveness, though influenced by payer formularies and evolving clinical guidelines.

Frequently Asked Questions

-

What is the primary indication for Aspirin-Dipyridamole ER? Aspirin-Dipyridamole ER is primarily indicated for the prevention of ischemic stroke and transient ischemic attacks (TIAs) in patients who have experienced stroke or TIA.

-

How does Aspirin-Dipyridamole ER differ from single-agent aspirin therapy? Aspirin-Dipyridamole ER combines aspirin, an antiplatelet agent, with dipyridamole, which also has antiplatelet effects and is a vasodilator. This combination offers a dual mechanism that can be more effective for certain patient populations in preventing recurrent ischemic events compared to aspirin alone.

-

Are there significant side effects associated with Aspirin-Dipyridamole ER? Common side effects include headache, which is often associated with dipyridamole and may decrease over time or with slower titration. Gastrointestinal issues related to aspirin, such as bleeding or irritation, are also potential side effects.

-

What is the average cost of generic Aspirin-Dipyridamole ER compared to DOACs? Generic Aspirin-Dipyridamole ER is substantially more affordable. A one-month supply typically costs between \$15 and \$50, whereas Direct Oral Anticoagulants (DOACs) can range from \$200 to \$400 or more per month.

-

Will there be new branded versions of Aspirin-Dipyridamole ER introduced to the market? It is unlikely that new branded versions of the core Aspirin-Dipyridamole ER combination will be introduced, given the expiration of primary patents and the dominance of generic competition. Any new developments would likely involve novel formulations, combination with other agents, or new therapeutic indications, requiring significant new R&D and regulatory hurdles.

Citations

[1] World Health Organization. (2022). Cardiovascular diseases (CVDs). Retrieved from https://www.who.int/news-room/fact-sheets/detail/cardiovascular-diseases-(cvds)

[2] Secondary Prevention of Stroke: A Review of Guidelines. (2017). Journal of Neuro & Spinal Surgery, 2(3), 121-128.

[3] Kernan, W. N., Ovbiagele, B., Black, S. E., Messé, S. R., Smith, E. E., Johnston, S. C., ... & Committee, A. A. S. A. P. S. G. (2014). Guidelines for the secondary prevention of stroke: A guideline for healthcare professionals from the American Heart Association/American Stroke Association. Stroke, 45(10), 3092-3127.

[4] Grand View Research. (2023). Antithrombotic Drugs Market Size, Share & Trends Analysis Report By Drug Class, By Application, By Region, And Segment Forecasts, 2023 - 2030. (Report accessed for market estimation purposes).

More… ↓