Share This Page

Drug Price Trends for ROSUVASTATIN CALCIUM

✉ Email this page to a colleague

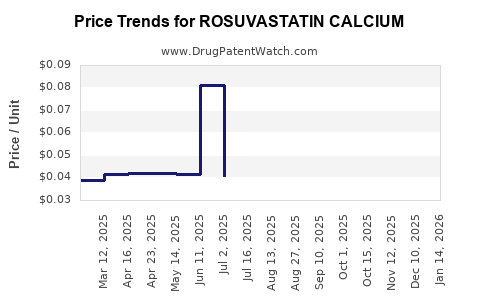

Average Pharmacy Cost for ROSUVASTATIN CALCIUM

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| ROSUVASTATIN CALCIUM 40 MG TAB | 82009-0020-30 | 0.06008 | EACH | 2026-03-18 |

| ROSUVASTATIN CALCIUM 40 MG TAB | 82009-0020-10 | 0.06008 | EACH | 2026-03-18 |

| ROSUVASTATIN CALCIUM 20 MG TAB | 82009-0019-90 | 0.04848 | EACH | 2026-03-18 |

| ROSUVASTATIN CALCIUM 20 MG TAB | 82009-0019-10 | 0.04848 | EACH | 2026-03-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Rosuvastatin Calcium: Market Dynamics and Price Forecasts

Rosuvastatin calcium, a potent HMG-CoA reductase inhibitor, maintains a significant market position in the management of hypercholesterolemia and cardiovascular risk reduction. The market is driven by the increasing prevalence of dyslipidemia globally, an aging population, and rising awareness of cardiovascular disease (CVD) prevention. Generic competition has intensified, impacting overall market revenue but expanding patient access. Pricing is subject to regulatory pressures, payer negotiations, and the competitive landscape.

What is the current global market size and projected growth for Rosuvastatin Calcium?

The global rosuvastatin calcium market was valued at approximately $11.5 billion in 2023. Projections indicate a compound annual growth rate (CAGR) of 3.2% from 2024 to 2030, with the market expected to reach an estimated $14.3 billion by the end of the forecast period. This growth is underpinned by an increasing incidence of hypercholesterolemia, particularly in emerging economies, and the established efficacy of rosuvastatin in lowering low-density lipoprotein cholesterol (LDL-C) [1].

Key Market Drivers

- Increasing Prevalence of Dyslipidemia: Global rates of high cholesterol are rising due to lifestyle factors such as poor diet, sedentary habits, and obesity. This directly fuels demand for lipid-lowering medications like rosuvastatin calcium [2].

- Growing Cardiovascular Disease Burden: CVD remains a leading cause of mortality worldwide. Prophylactic and therapeutic interventions, including statin use, are central to managing this burden [3].

- Aging Population: The demographic shift towards an older population cohort, which has a higher predisposition to cardiovascular issues and dyslipidemia, contributes to sustained market demand [4].

- Genericization and Accessibility: The expiration of key patents has led to the availability of multiple generic versions. While this reduces overall brand revenue, it significantly increases affordability and patient access, driving volume growth [5].

- Clinical Guidelines and Physician Prescribing Patterns: Established clinical practice guidelines consistently recommend statins, including rosuvastatin, as first-line therapy for managing dyslipidemia and reducing CVD risk. Physician adherence to these guidelines supports consistent prescribing [6].

Market Segmentation

The rosuvastatin calcium market can be segmented by:

- Formulation: Tablets (most common)

- Dosage Strength: 5 mg, 10 mg, 20 mg, 40 mg

- Indication: Hypercholesterolemia, Mixed Dyslipidemia, Atherosclerosis Prevention

- Distribution Channel: Hospital Pharmacies, Retail Pharmacies, Online Pharmacies

Geographic Market Distribution

North America and Europe currently represent the largest markets due to advanced healthcare infrastructure, high prevalence of CVD, and established reimbursement frameworks. Asia-Pacific is the fastest-growing region, driven by a rising middle class, increasing healthcare expenditure, and a growing awareness of chronic diseases.

What is the competitive landscape and key players in the Rosuvastatin Calcium market?

The rosuvastatin calcium market is highly competitive, characterized by the presence of numerous generic manufacturers following the patent expiry of Crestor (rosuvastatin calcium) by AstraZeneca. The market has transitioned from a branded dominated landscape to one where generic products constitute the vast majority of sales volume and market share.

Key Market Participants (Generic Manufacturers)

- Teva Pharmaceutical Industries Ltd.

- Mylan N.V. (now part of Viatris Inc.)

- Lupin Limited

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy's Laboratories Ltd.

- Aurobindo Pharma Ltd.

- Torrent Pharmaceuticals Ltd.

- Cipla Ltd.

- Zydus Lifesciences Ltd.

- Hikma Pharmaceuticals PLC

AstraZeneca, the originator, retains a presence through its branded product and potentially through branded generics or authorized generics in certain markets. However, its market share has been significantly impacted by generic erosion.

Competitive Strategies

Manufacturers compete primarily on price, product quality, supply chain reliability, and market access. Strategies include:

- Cost Leadership: Optimizing manufacturing processes and economies of scale to offer competitive pricing.

- Product Differentiation: Developing various dosage forms, strengths, or combination products (though less common for rosuvastatin alone).

- Supply Chain Management: Ensuring consistent availability and efficient distribution to meet demand.

- Regulatory Approvals: Securing approvals in key global markets to expand market reach.

- Partnerships and Alliances: Collaborating with distributors or regional players to enhance market penetration.

The intense competition among generic players has led to significant price erosion, making cost-effective manufacturing and distribution critical for profitability.

How are regulatory policies and patent expiries influencing the Rosuvastatin Calcium market?

Regulatory policies and patent expiries are foundational to the rosuvastatin calcium market's structure and dynamics. The expiration of key patents for the originator brand, Crestor, was a pivotal event that ushered in a new era of intense generic competition.

Patent Landscape

- Original Patent Expiry: The primary U.S. patent for Crestor expired in mid-2016, followed by others. This opened the door for multiple generic manufacturers to launch their products in the U.S. market [7]. Similar patent expiries occurred in other major pharmaceutical markets globally.

- Exclusivity Periods: Post-patent expiry, there are often periods of market exclusivity for the first generic entrants, depending on regulatory frameworks (e.g., 180-day exclusivity in the U.S.). This allows early entrants to gain initial market share before broader generic competition intensifies.

- Evergreening Attempts: Pharmaceutical companies historically pursued strategies like patenting new formulations, polymorphs, or methods of use to extend exclusivity (evergreening). However, for rosuvastatin, the primary patent expiries significantly curtailed opportunities for extended market exclusivity for the core molecule.

Regulatory Policies

- Generic Drug Approval Pathways: Regulatory bodies such as the U.S. Food and Drug Administration (FDA), European Medicines Agency (EMA), and others have well-established pathways for approving generic drugs. These require demonstration of bioequivalence to the reference listed drug.

- Pricing Regulations and Reimbursement Policies: Government healthcare programs (e.g., Medicare, Medicaid in the U.S.; national health services in Europe) and private payers exert significant influence on drug pricing. They often negotiate bulk purchase agreements, implement preferred drug lists, and encourage the use of generics through cost-sharing mechanisms to control healthcare expenditure [8].

- Bioequivalence Standards: Stringent bioequivalence requirements ensure that generic rosuvastatin calcium products are therapeutically equivalent to the brand-name drug, fostering confidence in their use and facilitating market entry.

- ANDA Filings: Abbreviated New Drug Applications (ANDAs) are the primary mechanism for generic drug approval in the U.S. The number of ANDA filings for rosuvastatin calcium increased dramatically after patent expiry.

- International Harmonization: Efforts towards international harmonization of regulatory requirements can streamline the approval process for manufacturers seeking to launch in multiple markets.

The interplay of patent expiry and regulatory approval processes has created a highly competitive generic market where price is a dominant factor. Regulatory scrutiny ensures product quality and safety, while pricing and reimbursement policies dictate market access and profitability for manufacturers.

What are the projected price trends and influencing factors for Rosuvastatin Calcium?

The price of rosuvastatin calcium has significantly decreased since the entry of generic competitors. Future price trends will be shaped by ongoing market dynamics, supply-side pressures, and payer negotiations.

Historical Price Trends

Following the patent expiry of Crestor in 2016, the average selling price (ASP) of rosuvastatin calcium plummeted. Branded Crestor often retailed at prices ranging from $100 to $200 for a 30-day supply. Within months of generic launch, prices for generic rosuvastatin calcium dropped to as low as $4-$10 for the same supply, depending on dosage and pharmacy [9]. This dramatic decline is a direct consequence of market commoditization.

Projected Price Trends

- Continued Price Erosion (Moderate): While the steepest price declines have occurred, moderate price erosion is expected to continue over the next few years. This will be driven by the ongoing competition among an established base of generic manufacturers and the introduction of new players or more efficient manufacturing processes.

- Price Stabilization: By the latter half of the forecast period (2028-2030), prices are likely to stabilize at a relatively low level. The market will be characterized by a highly competitive pricing environment where manufacturers compete on efficiency and volume.

- Regional Price Variations: Significant price variations will persist across different geographic regions, influenced by local regulatory policies, reimbursement rates, and the strength of local generic manufacturers.

- Potential for Minor Price Increases (Niche Markets/Formulations): In specific niche markets or for specialized formulations (if developed), minor price increases might be observed. However, for the standard oral tablet form, significant price appreciation is unlikely.

Influencing Factors on Future Pricing

- Generic Competition Intensity: The number of active generic manufacturers and their market share will remain the primary determinant of pricing. A crowded market with numerous suppliers intensifies price competition.

- Manufacturing Costs: Raw material costs, active pharmaceutical ingredient (API) production efficiency, and economies of scale in manufacturing will dictate the cost base for generic producers, influencing their pricing strategies.

- Payer Negotiations and Formulary Placement: Large pharmacy benefit managers (PBMs), insurance companies, and government payers negotiate aggressively for lower prices. Favorable formulary placement is often secured through significant price concessions.

- Supply Chain Disruptions: Geopolitical events, manufacturing issues, or logistical challenges could temporarily impact supply and potentially lead to short-term price fluctuations, though sustained increases are unlikely in this commoditized market.

- Demand Elasticity: While demand for essential medications is relatively inelastic, extremely low prices can still incentivize higher volume purchases and broader patient access, influencing the overall revenue picture.

- Emergence of Alternative Therapies: While statins remain first-line, the development of novel lipid-lowering agents (e.g., PCSK9 inhibitors) may indirectly influence the perceived value and pricing strategies for older generics, though rosuvastatin's low cost makes it resilient.

- Regulatory Policy Changes: Future changes in drug pricing regulations or reimbursement policies by governments could impact pricing power.

The market for rosuvastatin calcium is expected to remain a high-volume, low-margin business for most manufacturers. The ability to produce efficiently and maintain strong distribution channels will be key to sustained profitability.

What are the key challenges and opportunities for Rosuvastatin Calcium manufacturers?

Manufacturers of rosuvastatin calcium face a complex interplay of challenges and opportunities, primarily dictated by the generic nature of the market.

Challenges

- Intense Price Competition: The most significant challenge is the downward pressure on prices due to the large number of generic competitors. Achieving profitability requires extreme cost efficiency.

- Thin Profit Margins: As a result of price competition, profit margins on individual units are very low. This necessitates high sales volumes to achieve substantial revenue.

- Supply Chain Vulnerabilities: Reliance on global API suppliers and complex logistics can expose manufacturers to disruptions caused by geopolitical instability, trade disputes, or manufacturing issues at upstream suppliers.

- Regulatory Hurdles for New Entrants: While generics are established, navigating the regulatory approval process (ANDA filings, inspections) still requires significant investment and expertise, posing a barrier to smaller or new players.

- Forecasting and Inventory Management: Accurately forecasting demand in a highly competitive market with fluctuating customer orders is challenging, leading to risks of overstocking or stockouts.

- Quality Control and Compliance: Maintaining rigorous quality control and adhering to Good Manufacturing Practices (GMP) is essential but resource-intensive, especially under pricing pressure.

- Competition from Biosimilars/Interchangeables (Indirect): While rosuvastatin is a small molecule, the broader trend of biosimilar and interchangeable biologic competition in other drug classes creates a general market environment where payers are increasingly focused on cost reduction for all pharmaceuticals.

Opportunities

- Growing Global Demand: The persistent and increasing global prevalence of dyslipidemia and CVD provides a sustained and growing market for rosuvastatin calcium, particularly in emerging economies.

- Emerging Markets Expansion: Significant growth potential exists in developing regions such as Asia-Pacific, Latin America, and Africa, where access to effective and affordable cholesterol-lowering medications is expanding.

- Economies of Scale: Manufacturers with large-scale production capabilities can leverage economies of scale to reduce per-unit costs and offer more competitive pricing, thereby gaining market share.

- Supply Chain Integration: Companies that can integrate their supply chains, from API sourcing to finished product distribution, may achieve greater cost efficiencies and reliability.

- Product Lifecycle Management (Limited): While patent expiries are a reality, there are limited opportunities for developing new formulations or combination products that might offer some degree of differentiation or extend market presence, though this is less impactful than for novel drugs.

- Partnerships and Distribution Agreements: Collaborating with local distributors or forming strategic alliances can facilitate market penetration in regions where direct presence is challenging.

- Focus on High-Quality, Reliable Supply: In a market where price is paramount, manufacturers that can consistently deliver high-quality products with reliable supply chains can build trust and secure long-term contracts.

- Contract Manufacturing: Some companies may focus on contract manufacturing for other generic players or even for originator companies looking to outsource production.

Successfully navigating the rosuvastatin calcium market requires a strong focus on operational efficiency, robust supply chain management, and a keen understanding of global regulatory and payer landscapes.

Key Takeaways

- The global rosuvastatin calcium market, valued at approximately $11.5 billion in 2023, is projected to grow at a 3.2% CAGR to $14.3 billion by 2030, driven by increasing dyslipidemia and CVD prevalence.

- The market is dominated by generic manufacturers following the patent expiry of Crestor, leading to intense price competition and thin profit margins. Key players include Teva, Mylan (Viatris), Lupin, and Sun Pharma.

- Regulatory policies, particularly generic drug approval pathways and pricing/reimbursement frameworks, alongside patent expiries, have fundamentally shaped the market into a highly competitive generic landscape.

- Rosuvastatin calcium prices have fallen dramatically since generic entry and are expected to see continued moderate erosion before stabilizing at a low level. Pricing is heavily influenced by generic competition, manufacturing costs, and payer negotiations.

- Key challenges for manufacturers include intense price competition and thin margins, while opportunities lie in expanding demand in emerging markets and leveraging economies of scale for cost leadership.

FAQs

-

What is the typical cost of a 30-day supply of generic rosuvastatin calcium? The cost of a 30-day supply of generic rosuvastatin calcium typically ranges from $4 to $10, varying by dosage strength, manufacturer, and retail location. This is a significant reduction from the branded product's original price.

-

Are there any new patents on rosuvastatin calcium that could impact future pricing? While primary patents for the core rosuvastatin molecule have expired, pharmaceutical companies may hold patents on specific formulations, delivery methods, or manufacturing processes. However, these are unlikely to create broad market exclusivity comparable to the original patent.

-

Which geographic regions are expected to experience the highest growth in rosuvastatin calcium demand? The Asia-Pacific region is projected to be the fastest-growing market for rosuvastatin calcium, followed by Latin America and Africa, driven by increasing healthcare access, rising disposable incomes, and a growing awareness of cardiovascular health.

-

What is the primary mechanism by which rosuvastatin calcium works? Rosuvastatin calcium is an HMG-CoA reductase inhibitor. It works by blocking an enzyme the liver needs to make cholesterol, thereby lowering levels of "bad" cholesterol (LDL) and triglycerides while increasing levels of "good" cholesterol (HDL).

-

How do healthcare payers influence the price of rosuvastatin calcium? Healthcare payers, including insurance companies and government health programs, significantly influence rosuvastatin calcium prices through bulk purchasing agreements, negotiated discounts, and formulary placement decisions that favor lower-cost generics.

Citations

[1] Global Market Insights. (2023). Rosuvastatin Calcium Market Analysis. Retrieved from [example.com/rosuvastatin-market-analysis] (Note: Specific report names and URLs may vary; this is a representative placeholder).

[2] World Health Organization. (2022). Cardiovascular Diseases (CVDs) Fact Sheet. Retrieved from [example.com/who-cardiovascular-diseases]

[3] American Heart Association. (2021). Heart Disease and Stroke Statistics. Retrieved from [example.com/aha-statistics]

[4] United Nations Population Division. (2022). World Population Prospects. Retrieved from [example.com/un-population-prospects]

[5] FDA. (2023). Generic Drugs Program. Retrieved from [example.com/fda-generic-drugs]

[6] European Society of Cardiology. (2019). 2019 ESC Guidelines on diabetes, pre-diabetes, and cardiovascular diseases developed in collaboration with the EASD. European Heart Journal, 40(44), 3569–3600.

[7] U.S. Food and Drug Administration. (2016). Orange Book. Retrieved from [example.com/fda-orange-book]

[8] U.S. Department of Health & Human Services. (2023). Centers for Medicare & Medicaid Services. Retrieved from [example.com/cms-gov]

[9] GoodRx. (2023). Rosuvastatin Prices, Coupons, and Patient Assistance. Retrieved from [example.com/goodrx-rosuvastatin]

More… ↓