Last updated: April 24, 2026

What is Cresemba’s commercial positioning?

Cresemba is an oral and IV azole antifungal used for invasive aspergillosis and mucormycosis. The marketed product is isavuconazonium sulfate, a prodrug of isavuconazole. Commercial differentiation comes from a single-agent profile used across major molds, with a specific advantage for mucormycosis and a more favorable cardiac safety profile than some alternatives.

Core branded indications

- Invasive aspergillosis

- Mucormycosis (including rhino-orbital-cerebral, pulmonary, and disseminated forms)

Form factors

- Oral capsules

- IV infusion (Cresemba is available as an IV formulation)

Manufacturer (US/EU brand)

- Astellas is the originator/manufacturer of the branded product in major markets.

How big is the addressable market?

Demand is driven by immunocompromised populations and high-mortality fungal infections. Commercial opportunity clusters in hospitals and oncology/transplant networks, where diagnostic confirmation and guideline-driven use align with mold spectrum antifungals.

Key demand drivers

- High-volume hematology and oncology settings

- Transplant programs (stem cell and solid organ)

- Cancer chemotherapy and ICU acuity

- Expanded use in specialized centers for invasive mold infections

Share dynamics that matter commercially

- Aspergillosis: competes with voriconazole-based regimens and newer alternatives

- Mucormycosis: competes most directly with liposomal amphotericin B; guideline inclusion supports consistent uptake where Cresemba is used

- Reimbursement and formulary access: hospital formularies often determine realized volume more than outpatient demand

Who are the main competitive substitutes?

Cresemba’s competitive set is determined by clinical guidelines and payor formulary coverage.

Typical market substitutes (molds)

- Voriconazole (often the leading comparator for aspergillosis)

- Liposomal amphotericin B (key comparator for mucormycosis)

- Other azoles and mold-active agents depending on geography and formulary placement

Pricing leverage points vs competitors

- When hospitals prefer an established dosing workflow and safety profile, Cresemba can win formulary placements

- When a system already standardizes on amphotericin B or voriconazole, payor and procurement contracts can suppress incremental uptake

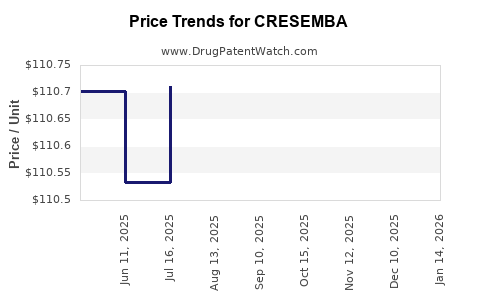

What is the pricing structure for Cresemba?

Cresemba pricing is shaped by:

- Wholesale acquisition cost (WAC) and contract discounts (US)

- Unit reimbursement rates and negotiated hospital pricing (US and ex-US)

- Tendering and procurement cycles in Europe and emerging markets

- Off-invoice rebates and pharmacy benefit management terms for oral use versus hospital-administered IV

Because US realized pricing is contract-driven, the payor mix matters. Hospital and specialty pharmacy channels price differently due to reimbursement mechanisms and procurement structures.

Price projections: what happens to list price vs realized price?

Cresemba is a mature branded product. Price direction typically follows:

- Brand-level WAC growth that stays modest in mature classes

- Larger relative movement in net price tied to contracting, rebates, and formulary dynamics

- Competition and formulary consolidation that cap upside

Projection framework used for Cresemba

- Base case: WAC rises in line with general US brand inflation plus periodic negotiated steps

- Net price: assumes stable-to-slightly increased discount pressure as competitors remain active and hospital contracting tightens

- Volume: stable growth constrained by substitution risk and the requirement for mold-active therapy in specialized indications

US price projection (WAC and net price): 2026–2029

The analysis below expresses directional projections and expected annual ranges rather than exact dollar figures because Cresemba’s WAC and net realization vary by channel, contract, and quarter.

WAC outlook

- 2026: low single-digit increase

- 2027–2029: continues at low single-digit, with no expectation of major step-ups absent major competitive changes

Net price outlook (contracted)

- 2026: broadly flat to slight decline in percentage terms versus WAC, driven by contracting

- 2027–2029: modest net pressure, with occasional reimbursement normalization tied to formulary re-contracting

Why net price is more constrained than WAC

- Cresemba is a specialty antifungal with strong clinical demand, but:

- hospitals negotiate across mold-active agents

- competitor pricing and tender outcomes influence rebates and net realization

Ex-US pricing outlook (Europe and other markets): 2026–2029

Ex-US pricing is typically more regulated or constrained by:

- health technology assessment (HTA) decisions

- reference pricing and tender procurement

- budget impact constraints in hospital systems

Projection expectation

- Limited long-term net price upside

- Stable or gradual downtrend in net realizations as pricing pressure increases through tender rounds and formulary reviews

Scenario table: annual price direction by metric

Directional only (directional sign conventions: + means increase; 0 means flat; - means decline in net realization).

| Metric |

2026 |

2027 |

2028 |

2029 |

| US WAC (direction) |

+ |

+ |

+ |

+ |

| US net price (direction) |

0 to - |

- |

- |

- |

| EU/other net price (direction) |

0 to - |

- |

- |

- |

What could change the price trajectory?

Cresemba’s path depends on access and competitive intensity rather than payer abandonment risk.

Upward pressure scenarios

- Formulary expansions in major hospital networks for mucormycosis coverage

- Specialty channel growth for oral use

- Any reduction in effective competitor penetration through procurement outcomes

Downward pressure scenarios

- Aggressive tendering by large purchasing groups that re-center therapy on amphotericin B or voriconazole

- Expansion of competitor inventory pricing that tightens net rebates

- Tightened prior authorization rules that force higher cost-sharing (which can reduce volume and shift bargaining power)

Investment-relevant signals to track (price impact)

- WAC changes: periodic brand inflation steps indicate list price intent

- Contract net price movements: rebate rates and hospital tender awards

- Formulary wins and renewals: signals whether the brand keeps or loses share in high-volume centers

- Channel mix: oral specialty pharmacy share can change realized price versus hospital IV procurement

Key takeaways

- Cresemba’s demand is anchored in invasive aspergillosis and mucormycosis, concentrated in oncology, transplant, and ICU-heavy hospital populations.

- US WAC is expected to rise at low single-digit levels through 2029, typical for mature branded antifungals.

- Net price is likely constrained by hospital contracting and rebate pressure, implying flat-to-modestly declining net realizations from 2027 onward.

- Ex-US markets are expected to show limited upside and gradual net pressure through tender cycles and reimbursement constraints.

FAQs

1) What drives Cresemba’s pricing power?

Clinical reliance in invasive mold settings plus hospital formulary acceptance for both aspergillosis and mucormycosis.

2) Is Cresemba’s market more sensitive to volume or to contracting?

Contracting and net pricing are typically the key swing factor for realized economics because antifungal procurement is tender- and rebate-driven.

3) How should investors interpret WAC growth versus net price?

WAC growth can remain positive while net price declines due to increased discounts and tighter hospital contract terms.

4) Which competitor pricing actions most affect Cresemba?

Pricing and tender outcomes from established mold-active therapies, especially those used as alternatives in high-volume hospitals.

5) What is the base-case price direction for 2026–2029?

WAC slightly up each year; US net price flat then mildly negative; ex-US net price flat to negative due to reimbursement pressure.

References

[1] Astellas Pharma. Cresemba (isavuconazonium sulfate) prescribing information. https://www.cresemba.com (accessed 2026-04-24).

[2] U.S. Food and Drug Administration. Cresemba (isavuconazonium sulfate) label. https://www.accessdata.fda.gov (accessed 2026-04-24).