1. What This Article Covers and Why It Matters Now

The baseline 20-year patent term for a small molecule drug is widely understood. What is less understood — and considerably more consequential for portfolio managers, IP counsel, and payers — is the secondary patent wall that manufacturers construct around the delivery device attached to that molecule. When the compound patent expires, the device patent survives. Competitors cannot enter without navigating a separate thicket of claims covering injector springs, inhaler valve geometries, pen needle assemblies, and dosing cartridges.

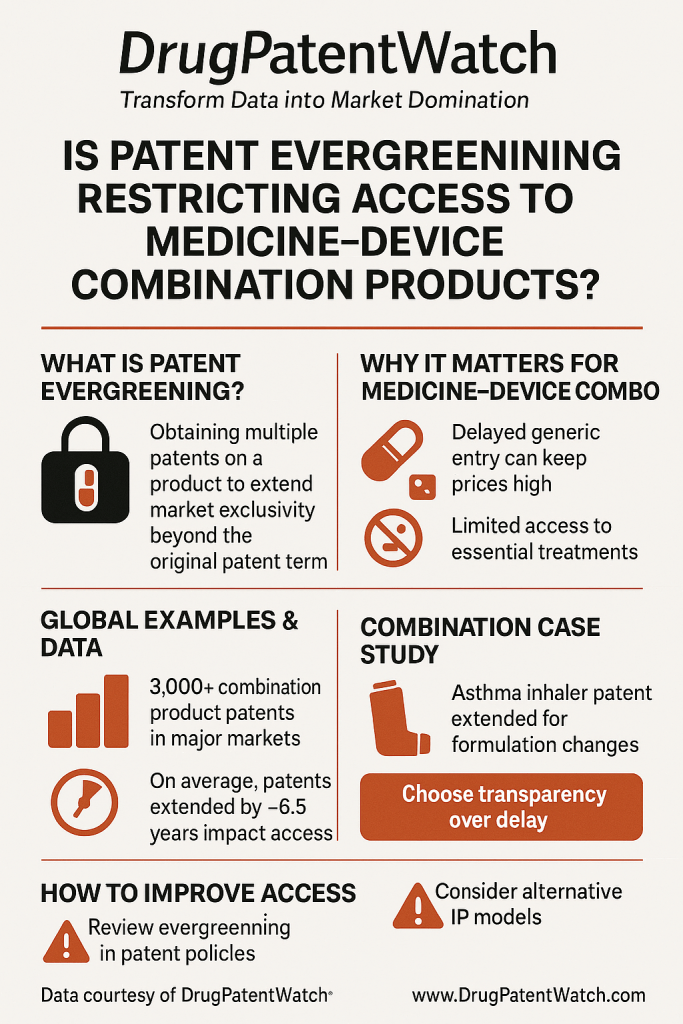

The median additional exclusivity conferred by device patents on medicine/device combination products is 4.7 years, with the high end reaching 15.2 years. Across a portfolio of branded combination products, that gap represents billions of dollars in revenue that would otherwise face generic competition.

This article maps the full mechanics of that system: how it works at the patent prosecution level, how Orange Book listing converts device patents into a Hatch-Waxman blocking tool, how the FTC’s 2023-2025 enforcement campaign is dismantling it, and what the Federal Circuit’s January 2025 ruling means for every NDA holder with device patents currently listed.

For analysts, the competitive implications go beyond individual drugs. Entire therapeutic franchises in respiratory, diabetes, and allergy have been built on this architecture. Understanding where device patents stand, product by product, is now a core requirement for accurate revenue forecasting and LOE (loss of exclusivity) modeling.

2. Evergreening: A Precise Definition

The term ‘evergreening’ gets used loosely. A workable definition for IP and commercial teams requires precision.

In its general form, evergreening occurs when a secondary patent extends a product’s exclusivity period without delivering a proportionate public benefit of any kind. In its health-specific form, it occurs when secondary patents extend exclusivity without a proportionate improvement in the standard of care. These two definitions are not identical. A device modification might reduce greenhouse gas emissions without improving clinical outcomes; whether that counts as adequate ‘proportionate benefit’ is genuinely contested.

What is not contested is the structural mechanism. Pharmaceutical compounds and their delivery devices are separately patentable under U.S. law. A metered-dose inhaler, an auto-injector pen, a soft-mist inhaler, an insulin cartridge system — each component generates its own patentable claims: mechanical assemblies, valve designs, dosing mechanisms, materials specifications, software interfaces in digital devices, manufacturing processes. Companies file on each independently. The expiry dates of those patents do not track the expiry of the original compound patent.

The result is that a drug whose active ingredient has been off-patent for decades can remain shielded from generic combination-product competition through an intact device patent portfolio. This is not a loophole or an accident. It is the deliberate output of a patent prosecution strategy known in lifecycle management circles as ‘patent stacking’ or ‘secondary patenting on combination products.’

Evergreening is different from, though related to, several other lifecycle management tactics pharma IP teams use:

A ‘chiral switch’ re-patents a racemic mixture by isolating one enantiomer (omeprazole to esomeprazole).

‘Product hopping’ shifts patients from an original formulation to a modified one before generics enter the original market.

‘Formulation patents’ cover new salt forms, polymorphs, or extended-release versions.

Device evergreening specifically covers the physical or electronic apparatus through which the molecule is delivered.

Device evergreening is analytically distinct because the patented innovation is entirely external to the molecule’s therapeutic mechanism. The spring tension in an auto-injector does not change what epinephrine does in anaphylaxis. The valve geometry in a soft-mist inhaler does not change the bronchodilatory profile of ipratropium. Whether those device modifications have clinical value is a separate question from whether they deliver the molecule as effectively as a less elaborate device would.

3. The Anatomy of a Medicine/Device Patent Stack

To understand how device evergreening creates market exclusivity, it helps to trace the layering of a typical combination product’s patent portfolio.

Layer 1: The Compound Patent. This covers the active pharmaceutical ingredient (API) — its chemical structure, synthesis method, and sometimes its polymorphic form. For most branded drugs launched before 2000, this patent has expired or is close to expiry. It is the original basis for the 20-year exclusivity clock.

Layer 2: Formulation Patents. These cover the pharmaceutical formulation: the suspension vehicle, excipients, buffer systems, preservatives, and particle size specifications that govern drug stability and bioavailability. In inhalation products, formulation patents frequently cover the propellant (HFA vs. CFC), the surfactant system, and the particle engineering that determines lung deposition.

Layer 3: Primary Device Patents. These cover the core delivery mechanism: the inhaler’s metering valve, the auto-injector’s spring-and-needle assembly, the insulin pen’s dose dial and cartridge interface. These patents are filed at or near the time of the original NDA and typically expire within a few years of compound patent expiry — but not always.

Layer 4: Secondary and Tertiary Device Patents. This is where evergreening operates. As the compound and primary device patents age, companies prosecute incremental modifications to individual device components. A 2018 study in Nature Biotechnology documented ‘tertiary patenting’ on drug-device combinations — patents filed on the device after the product had already been on the market for years, often covering minor mechanical refinements or ergonomic changes with no clinical data supporting improved outcomes.

Layer 5: Digital and Software Patents. As inhalers and injectors acquire Bluetooth connectivity, dose counters, companion apps, and sensor arrays, a new category of device patents covers the electronic and software architecture. These patents can extend exclusivity into the 2030s and 2040s for products whose APIs were synthesized in the 1970s.

The stacking across layers creates what patent lawyers call a ‘patent thicket’: a dense network of overlapping claims that a generic manufacturer must invalidate or design around to bring a competing combination product to market. Each layer involves separate litigation risk, separate PTAB inter partes review proceedings, and separate regulatory exclusivity analysis. The cost and time burden of clearing that thicket deters market entry independent of whether individual patents would survive challenge.

Key Takeaways — Section 3

The patent stack for a medicine/device combination product is not a single asset; it is a portfolio of assets with different expiry dates, claim scopes, and litigation profiles. IP teams conducting competitor landscape analysis must model each layer separately. Revenue forecasting that uses the compound patent LOE as the generic entry date will systematically overestimate when revenue erosion begins — but may also miss cases where device patents outlast compound patents by more than a decade.

4. How the Orange Book Turned Device Patents Into a Competitive Weapon

The Orange Book — formally the FDA’s ‘Approved Drug Products with Therapeutic Equivalence Evaluations’ — does more than catalog approved drugs. Under the Hatch-Waxman Act of 1984, a generic manufacturer filing an Abbreviated New Drug Application (ANDA) must certify with respect to every patent listed in the Orange Book for the reference listed drug (RLD).

A Paragraph IV certification — the most commercially aggressive path — asserts that the listed patent is either invalid or will not be infringed by the generic. Filing a Paragraph IV certification triggers an automatic 30-month stay on FDA approval of the generic ANDA, during which the brand manufacturer can litigate. The stay runs whether or not the patent is ultimately found valid, and whether or not the device patent has any genuine bearing on the API being copied.

This is the structural mechanism that converts a device patent from a narrow property right into a competitive blocking tool. By listing device patents in the Orange Book, brand manufacturers force generic ANDA filers into Paragraph IV litigation on patents that may claim nothing about the drug’s active ingredient. Each patent listing triggers a separate potential 30-month stay. Multiple device patents listed for the same product can create cascading stays that delay generic entry by years beyond the stay triggered by the compound patent.

The FDA’s rules governing what patents qualify for Orange Book listing have been ambiguous on device patents for decades. The statute requires listed patents to ‘claim the drug’ or ‘claim a method of using the drug.’ Whether a patent claiming only the mechanical components of a delivery device ‘claims the drug’ has been contested in the courts, at the FTC, and now at the Federal Circuit.

Until the FTC began its enforcement campaign in 2023, the practical answer was that companies listed device patents freely, generic filers faced litigation costs whether or not the patents were valid, and the ambiguity functioned as a de facto subsidy for brand manufacturers.

5. Case Study: Boehringer Ingelheim’s Respimat Line — IP Valuation and Competitive Dynamics

The Product and Its Patent Architecture

Combivent Respimat combines albuterol sulfate and ipratropium bromide, two bronchodilators. Ipratropium’s original compound patent dates to 1970. Albuterol’s to 1972. Both molecules have been generic for decades. Yet Combivent Respimat carried 25 Orange Book-listed patents as of recent counts, all covering the Respimat soft-mist inhaler device — with the last-to-expire running to 2030.

That gives Boehringer Ingelheim patent protection in one form or another on ipratropium since 1970, a span of 60 years and counting. The original 20-year compound patent term ended in 1990. Everything since has been formulation and device protection.

The product generated approximately $650 million in 2022 U.S. revenues. The COPD drugs market globally ran to roughly $19.5 billion that year. Following the Inflation Reduction Act enforcement actions and FTC challenges, several Combivent Respimat device patents were challenged for improper Orange Book listing. As of current data, the generic launch date based on the last remaining active patents is estimated at October 2030.

IP Valuation: The Respimat Platform

The Respimat inhaler is not a single-product asset. Boehringer listed the same device patents across its entire Respimat product line: Spiriva Respimat (tiotropium), Stiolto Respimat (tiotropium-olodaterol), and Striverdi Respimat (olodaterol). Stiolto Respimat carried 26 pre-approval Orange Book patents, including 18 device patents. Striverdi carried 25, also with 18 device patents.

From an IP valuation perspective, a platform device patent portfolio is significantly more valuable than product-specific device claims. A single device patent covering the Respimat valve mechanism can be listed for multiple NDAs, triggering Paragraph IV stays across all of them simultaneously. The cost to a generic challenger to mount PTAB inter partes review (IPR) petitions on all relevant claims across all products is multiplicatively higher than the cost Boehringer incurred to prosecute the underlying patents.

Boehringer’s effective IP barrier is therefore not 25 patents for Combivent alone — it is 18 shared device patents functioning as a franchise-wide moat across four respiratory products generating combined revenues in the multi-billion dollar range. The per-patent return on prosecution investment for a platform device claim of this type is extraordinary.

The FTC’s 2023 and 2024 warning letters specifically called out Boehringer Ingelheim as one of the companies that declined to delist challenged device patents. AstraZeneca and Teva similarly stood firm. The litigation that followed represents the first systematic legal testing of whether inhaler device patents are valid Orange Book listings — and its outcome will reprice this IP category for the entire respiratory sector.

The CFC-to-HFA Transition: A Regulatory Opportunity Converted to IP Strategy

The FDA’s ban on CFC-propellant inhalers, phased in between 2008 and 2013, created a regulatory mandate for manufacturers to switch to HFA-based formulations. This transition required genuine reformulation work. It also required new device engineering in some cases, particularly for soft-mist inhalers.

The patent opportunity was maximized. Manufacturers obtained new Orange Book-listed patents on HFA formulations, new device configurations, and updated particle engineering. The Combivent CFC product had been approved in 1996. The HFA-reformulated Respimat product extended protection from 1996 to at least 2030 — 34 years of continuous patent coverage for two molecules that went generic in the 1980s.

The same dynamic is now visible on the horizon with HFA propellants themselves. HFAs are potent greenhouse gas emitters. Regulatory pressure to replace them with low-global-warming-potential (low-GWP) propellants such as HFO-1234ze is building in the EU and UK. Each manufacturer that reformulates for low-GWP delivery has a commercially incentivized reason to patent the new device and formulation extensively, restarting the exclusivity clock for another decade or more. Without regulatory intervention, the CFC-to-HFA pattern will repeat.

Key Takeaways — Section 5

Boehringer’s Respimat architecture is the canonical example of platform device evergreening. The IP valuation lesson is that a device patent covering multiple products in a line is far more valuable than any single compound patent in that portfolio, because its blocking function operates across the entire franchise. For analysts modeling Boehringer’s respiratory revenue, the effective LOE dates for Respimat-platform products are device-patent-governed, not API-governed. Any generic challenge to one Respimat product’s device patents has immediate read-across valuation implications for the full line.

6. Case Study: EpiPen / Epinephrine Auto-Injectors — IP Valuation and Competitive Dynamics

The Product and Its Patent Architecture

Epinephrine has been used medically for over 120 years. It is among the cheapest molecules in commercial pharmacopeia. The EpiPen auto-injector, first approved in 1987, converted that commodity molecule into a branded franchise by pairing it with a spring-loaded, needle-retraction device designed for self-administration in anaphylaxis emergencies.

The key patent enabling that franchise is US7449012, filed by Meridian Medical Technologies (then a Pfizer subsidiary) on April 1, 2005 — 23 days after Mylan acquired the rights to the EpiPen from Merck Generics. That patent covers the auto-injector mechanism, including two locking assemblies for the needle cover. It was issued in November 2008 and formed the basis of a successful 2009 lawsuit against Teva Pharmaceuticals, which had attempted to bring a generic auto-injector to market.

Three further device patents were prosecuted and awarded between 2008 and 2014. With those patents protecting the 2011 redesigned EpiPen device, Mylan (later Viatris following its 2020 merger with Pfizer’s Upjohn division) maintained exclusivity on the branded auto-injector until September 2025, when the core device patents expired.

IP Valuation: The EpiPen Franchise

The EpiPen’s IP architecture illustrates a different evergreening pattern from Boehringer’s platform model. Rather than protecting a delivery device across multiple drug products, Mylan/Viatris used a succession of device patents on the same product — each covering incremental refinements — to maintain exclusivity for 38 years on a molecule that has been a generic commodity since before the device existed.

The price consequence was extreme. Between 2007 and 2016, the list price for a two-pack of EpiPens rose from approximately $94 to $608 — a 550% increase. The device patent portfolio was one structural enabler of that pricing power; PBM rebate practices and formulary dynamics also contributed.

The legal consequences have been substantial. In January 2025, Mylan settled for $73.5 million with KPH Healthcare Services after allegations that it conspired with Pfizer and Teva to delay generic EpiPen entry and protect market monopoly. That settlement followed years of litigation and regulatory scrutiny. The total litigation cost to the franchise — in legal fees, settlement payments, and congressional attention — likely exceeded $500 million.

For IP teams modeling the ‘return on evergreening’ in auto-injector categories, the EpiPen case is instructive: the device patent strategy generated multi-billion-dollar revenue that would otherwise have been competed away, but it attracted regulatory and litigation risk that materially reduced the net economic value of the strategy. Whether the trade-off was positive depends on assumptions about the timeline and probability of regulatory intervention that were genuinely uncertain at the time of the patent prosecution decisions.

The September 2025 Patent Expiry and Its Market Implications

The expiry of EpiPen’s core device patents in September 2025 opened the spring-loaded auto-injector mechanism to generic use. Competitors can now design around the expired claims rather than the active ones, significantly reducing the engineering cost of market entry. The resulting competition is expected to erode Viatris’s market share materially, with generics typically entering at 30-50% of branded pricing.

Viatris’s response will likely include applications for secondary patents on next-generation EpiPen features: Bluetooth connectivity for dose tracking, digital readouts, child-specific ergonomic modifications, or integration with allergy management apps. Whether those patents constitute genuine therapeutic innovation or a new cycle of device evergreening will depend on clinical data that does not yet exist.

Key Takeaways — Section 6

The EpiPen franchise demonstrates that device evergreening on a single-product auto-injector can sustain exclusivity for nearly four decades on a century-old molecule. The financial returns were substantial but attracted legal and regulatory costs that any IP team must now factor into evergreening strategy projections. The September 2025 expiry opens a new competitive window for both generic manufacturers and innovators developing genuinely differentiated epinephrine delivery technologies. For investors, the question is whether Viatris has a credible next-generation device platform or whether it faces straight revenue erosion.

7. Case Study: Insulin Delivery Systems — IP Valuation and Competitive Dynamics

The Structural Problem in Insulin Devices

Insulin was first isolated in 1921. Its patent, donated to the University of Toronto for $1, expired decades ago. Yet insulin delivery systems — pens, pumps, continuous glucose monitor (CGM) integrations, and closed-loop systems — carry extensive and active patent portfolios. Device patents account for 55% of all patents listed for diabetes medicine/device combination products studied in the original Beall et al. research.

The three dominant insulin manufacturers — Novo Nordisk, Eli Lilly, and Sanofi — each maintain proprietary pen injector systems: FlexPen, KwikPen, and SoloStar respectively. These pens are not interchangeable. A pharmacy cannot substitute one for another without a prescriber change, because the dose delivery mechanism differs between systems. This device-driven non-interchangeability is commercially significant: it reduces biosimilar interchangeability even in cases where the insulin analog itself is approved as interchangeable at the molecular level.

IP Valuation: Novo Nordisk’s FlexTouch Platform

Novo Nordisk’s FlexTouch pen system covers multiple insulin products: Tresiba (degludec), Victoza (liraglutide, a GLP-1 receptor agonist delivered by injection), Ozempic (semaglutide), and Levemir (detemir). The device patent portfolio for FlexTouch covers the dose-setting mechanism, the cartridge coupling system, the audible dose confirmation mechanism, and the pressure-minimizing injection feature Novo markets as reducing injection force.

From an IP valuation perspective, the FlexTouch platform represents the same franchise-wide device patent architecture as Boehringer’s Respimat: a single device portfolio protecting multiple high-revenue products. Ozempic alone generated approximately $14 billion in global revenue in 2023. A semaglutide molecule whose core patent expires in the mid-2020s can maintain significant market exclusivity through device and formulation patents running into the 2030s, combined with regulatory exclusivity periods. Novo’s device patents on semaglutide delivery are now among the most consequential IP assets in the pharmaceutical industry.

The device non-interchangeability problem compounds this: even where a biosimilar semaglutide is approved, a prescriber or payer seeking to switch a patient from Ozempic to a biosimilar must navigate differences in the pen device, dosing increments, and patient training requirements. This friction depresses biosimilar uptake independently of patent protection, extending the economic life of the branded product.

Closed-Loop Systems and the Insulin Device Patent Frontier

The integration of insulin pumps, CGMs, and automated insulin delivery (AID) algorithms represents the next layer of device patent accumulation. Systems such as Medtronic’s MiniMed, Insulet’s Omnipod, and Tandem’s t:slim X2 with Control-IQ create closed-loop architectures where the insulin, the pump, the sensor, and the algorithm are all potentially separately patentable.

For companies managing insulin products, the strategic question is whether to vertically integrate device capabilities or to license. Novo Nordisk’s acquisition strategy in the connected device space reflects a calculation that device IP control is as commercially valuable as molecule IP control for long-lifecycle insulin products.

Key Takeaways — Section 7

Insulin delivery represents the most complex form of medicine/device evergreening because device non-interchangeability creates a market-structure barrier that operates independently of formal patent protection. For biosimilar insulin developers, navigating device IP is a threshold requirement for commercial success, not just a legal formality. The FlexTouch platform and its equivalents at Lilly and Sanofi are franchise-defining IP assets whose value must be separately modeled from compound and formulation IP when assessing biosimilar entry timelines and revenue erosion curves.

8. The Economic Math — What Device Exclusivity Costs Healthcare Systems

The 4.7-Year Gap and Its Revenue Translation

The Beall et al. figure — a median 4.7-year extension from device patents, with a range of 1.3 to 15.2 years — is a starting point for financial modeling, not a complete picture. The economic impact of that extension depends on the revenue the product generates in those additional years at monopoly pricing versus what competition would have produced.

For a branded combination product generating $500 million annually, a 4.7-year device patent extension represents approximately $2.35 billion in revenue protected from generic competition, assuming full generic erosion would occur without the device patents. In practice, generic entry typically reduces branded revenues by 60-90% within two years of the first generic launch, so the counterfactual revenue loss from full generic erosion is material.

At the portfolio level, the Health Savers Initiative analysis found that addressing evergreening through FDA exclusivity reforms could reduce federal deficits by at least $10 billion over the 2021-2030 decade, including $7 billion in Medicare Part D drug costs and $4 billion in reduced premiums and cost-sharing for Medicare beneficiaries.

The Healthcare System Cost Structure

The burden of device-driven exclusivity falls unevenly across payers. Medicare Part D, which covers a disproportionate share of patients using inhalers and auto-injectors (older patients with COPD, type 1 and 2 diabetes, and severe allergies), bears the largest direct cost. Commercial insurers absorb costs through elevated formulary tiers for branded combination products. Medicaid programs in states with aggressive preferred drug list management have more flexibility to drive generic or therapeutic substitution, but are constrained by device non-interchangeability and prescriber habits.

For patients, the cost burden is most acute in therapeutic categories where generic alternatives are not clinically interchangeable due to device differences. A COPD patient on a specific branded inhaler cannot simply switch to a generic of the same molecules if those molecules are only available in a different device requiring different technique and training. This clinical friction is real, and it is also commercially convenient for brand manufacturers.

In the U.S., a two-pack of EpiPens listed at over $600 compared to generic epinephrine injection vials available for under $10. That price differential exists almost entirely because of the patented auto-injector device. The clinical advantage of a pre-loaded, spring-activated device over a manual injection is real and documented, particularly for pediatric patients and in high-stress emergency conditions. Whether that advantage justifies a 60-fold price premium is the question the patent system, as currently structured, does not ask.

Global Impact: Emerging Markets and Essential Medicines

The economic burden of device evergreening in high-income markets is documented and quantifiable. In low- and middle-income countries, the effects are more difficult to measure precisely but potentially more severe. Thailand’s health ministry has documented concerns that medicine/device combination products subject to extended device patents will become unaffordable for public insurance systems within the coming decade.

India’s Patents Act Section 3(d) — which prohibits patents on new forms of known substances unless they demonstrate significantly enhanced efficacy — addresses small-molecule formulation evergreening but was not designed for device patents. The device patent category largely escapes India’s anti-evergreening provision because a mechanical delivery system does not straightforwardly fit the ‘new form of a known substance’ framework.

Countries party to TRIPS-plus bilateral trade agreements with the United States face additional constraints in implementing patent policies that would differentiate device patents from compound patents in ways that accelerate generic entry.

9. The FTC’s Orange Book Enforcement Campaign (2023-2025)

The September 2023 Policy Statement

The FTC’s September 2023 policy statement was the opening move in a systematic campaign against device patent listings. The statement asserted that device patents without drug-substance claims do not meet the statutory requirements for Orange Book listing under Hatch-Waxman, and that improper listings may constitute unfair or deceptive acts or practices under Section 5 of the FTC Act.

The commercial significance was immediate. Orange Book listing had, for years, operated as a near-automatic process. NDA holders self-certify patent eligibility; the FDA does not independently verify claims. The FTC’s statement signaled that this self-certification system would face external scrutiny, and that the consequences of improper listing could extend beyond administrative delisting to antitrust liability.

The November 2023 Warning Letters and Initial Delisting

In November 2023, the FTC sent warning letters to 10 pharmaceutical companies requesting delisting of over 100 device patents from the Orange Book. Several companies complied within the 30-day response window. AstraZeneca, Boehringer Ingelheim, and Teva did not delist the challenged patents for their inhaler products.

The April 2024 and May 2025 Escalations

On April 30, 2024, the FTC targeted over 300 additional device patent listings, sending warning letters covering inhalers for asthma and COPD as well as device patents on auto-injectors for weight-loss and diabetes treatments — notably GLP-1 delivery devices, bringing Novo Nordisk and Eli Lilly into the enforcement perimeter.

In May 2025, the FTC challenged an additional 200 Orange Book patents across 17 drug products. The cumulative effect: several hundred device patents have been removed from the Orange Book following FTC actions through mid-2025. The FTC’s amicus brief in the New Jersey district court case covering inhaler device patents was directly cited by the court in its June 2024 ruling that several inhaler patents were improperly listed.

Antitrust Litigation Follow-On

The FTC’s enforcement campaign has generated private plaintiff litigation. Companies that paid higher prices for branded combination products during periods when device patents allegedly delayed generic entry are now pursuing damages claims under antitrust theories. The theory: improper Orange Book listing violates Section 5 of the FTC Act and, derivatively, supports treble damages under Section 2 of the Sherman Act.

The litigation risk for NDA holders who did not delist challenged patents is material and not yet fully reflected in public market valuations. Legal teams at any company with device-heavy Orange Book listings should model the potential damages exposure based on the revenue differential between actual branded pricing and the hypothetical competitive price during the challenged exclusivity period.

10. The Federal Circuit January 2025 Ruling: A Structural Shift

The Federal Circuit’s January 2025 ruling on Orange Book patent listing eligibility is the most definitive legal statement yet on what device patents can and cannot do under Hatch-Waxman. The court held clearly: to be listed in the Orange Book, a patent must claim the drug for which the NDA was submitted and approved. To claim that drug, the patent must claim at least the active ingredient. Patents claiming only device components of a combination product NDA do not meet this listing requirement.

This ruling has several immediate consequences for IP teams and portfolio managers.

First, it resolves the ambiguity that manufacturers relied on to list pure device patents. The question is no longer contested; pure device patents without active ingredient claims are ineligible for Orange Book listing. Any currently listed device patent of this type is legally vulnerable to delisting through the FTC dispute process or judicial order.

Second, it reframes how manufacturers must draft future device patent claims if they want Orange Book listing benefits. Patents covering a device in combination with the active ingredient — claiming the combination as the inventive element — may survive the Federal Circuit standard, depending on how the claim is structured. IP prosecution teams are already rewriting device patent claim language to incorporate active ingredient references where possible.

Third, it establishes a read-across for all existing combination product NDAs with device-only Orange Book listings. Each of those listings now represents a legal liability rather than a competitive asset. The 30-month stays they could trigger in ANDA litigation are no longer reliable blocking tools.

For analysts: the January 2025 ruling accelerates the effective LOE timeline for combination products that depended on pure device patents for their Orange Book blocking function. Products whose only remaining Orange Book-listed patents are device-only claims may face earlier generic competition than financial models currently assume.

11. Investment Strategy for Analysts

Remodeling LOE Timelines

Standard LOE modeling uses the last-to-expire Orange Book patent as the generic entry trigger. That methodology is now partially obsolete. After the Federal Circuit ruling, the operative question is: which of the listed patents survive the ‘claims the active ingredient’ test? For any combination product with a substantial proportion of pure device patents in its Orange Book listing, the effective LOE date must be recalculated using only the patents that meet the Federal Circuit standard.

This recalculation will, for some products, pull forward the effective LOE date by several years. Revenue models that do not reflect this adjustment will overstate protected cash flows.

Identifying High-Risk Portfolios

The highest-risk company profiles for LOE acceleration share several characteristics: they are heavily weighted toward respiratory, diabetes, and allergy combination products; they have a high proportion of device patents relative to compound patents in their Orange Book listings; and they are named in FTC warning letters or current antitrust litigation.

Based on public enforcement data, AstraZeneca, Boehringer Ingelheim, Teva, Novo Nordisk, and Viatris all fall within this profile to varying degrees. A proprietary analysis of each company’s Orange Book listings using the Federal Circuit’s new standard would identify the magnitude of the vulnerability more precisely.

Identifying Opportunities for Generic and Biosimilar Developers

The same regulatory shift creates opportunities. Generic manufacturers and biosimilar developers who previously faced prohibitive ANDA litigation risk from device patent Paragraph IV triggers can now move more aggressively on combination products whose only remaining Orange Book barriers are device-only claims. PTAB IPR petitions against remaining compound and combination patents may be more economically viable once the device-only patent stack is cleared.

The FTC’s enforcement record also provides evidentiary support for Freedom to Operate (FTO) analyses. A device patent that the FTC has challenged and that the patent holder declined to defend through the 30-day response process carries a different risk profile than an uncontested listing.

The GLP-1 Device Patent Watch

The GLP-1 receptor agonist class — semaglutide, tirzepatide, liraglutide — represents the next major battleground for device evergreening. The core semaglutide compound patent expires in the mid-2020s for certain markets. Novo Nordisk and Eli Lilly are building device patent portfolios around their respective delivery systems — the FlexTouch and KwikPen platforms and next-generation auto-injector designs — that could extend branded exclusivity on these molecules well into the 2030s.

The FTC’s April 2024 warning letters specifically referenced device patents on auto-injectors for weight-loss and diabetes treatments, signaling regulatory awareness of this risk. For analysts, the critical question is whether Novo’s and Lilly’s device patents meet the Federal Circuit’s ‘claims the active ingredient’ standard. Those that do can be legitimately listed and will generate 30-month ANDA stays. Those that do not face the same FTC delisting pressure that cleared the inhaler patent portfolios.

The resolution of this question directly affects peak revenue forecasts for Ozempic, Wegovy, Mounjaro, and Zepbound — four of the five highest-revenue drugs in the global pharmaceutical market. Given that these products generate a combined $30-plus billion annually, the IP analysis is not an academic exercise.

12. The Innovation Defense: What the Data Actually Shows

The Industry Argument

The pharmaceutical industry’s consistent defense of device patenting is that delivery device improvements deliver genuine patient benefit. The argument takes several forms in different therapeutic contexts.

For respiratory inhalers, the HFA reformulation genuinely removed environmentally harmful propellants and in some cases improved fine particle fraction — the proportion of drug particles small enough to deposit in the lower airways. Some HFA formulations achieved equivalent therapeutic effect at lower doses than their CFC predecessors. The Respimat soft-mist inhaler produces a slower-moving aerosol cloud than conventional pressurized metered-dose inhalers, which proponents argue improves lung deposition in older COPD patients with reduced inspiratory flow rates.

For auto-injectors, spring-loaded mechanisms reduce the skill and force required for self-administration in emergencies, which has documented adherence and outcomes implications for pediatric patients and patients with compromised dexterity. The EpiPen’s device design is clinically meaningfully different from drawing epinephrine from a vial with a syringe under acute anaphylactic stress.

For insulin pens, dose accuracy, injection depth consistency, and needle gauge refinements have incremental clinical value that is real, if modest.

What the Data Shows

The study population in the Beall et al. research included 49 medicine/device combination products across asthma/COPD, diabetes, and allergy. Device patents existed for 90% of those products. For 14 products, device patents were the only unexpired patent category. In those 14 cases, the sole remaining barrier to generic competition was the device patent — not the molecule, not the formulation, not a method-of-use claim. Whether any of those 14 device portfolios covered innovations with proportionate clinical benefit is a product-by-product question that the patent system does not directly evaluate.

The broader literature on pharmaceutical evergreening converges on a finding that the patent system incentivizes patentable ideas rather than the most therapeutically beneficial ones. A minor device modification that is patentable will be patented regardless of whether a more therapeutically valuable modification that is less patentable would have served patients better. This misalignment between patent incentives and clinical outcomes is structural, not the result of bad actors making deliberate anti-patient decisions. It is the predictable output of a system that rewards IP filings rather than clinical endpoints.

The perverse incentive identified in the PMC literature is worth stating explicitly: companies that can protect a high-revenue injectable molecule from generic competition by making it device-intensive have a financial reason to do so that is independent of any clinical logic. This may explain why, as researchers noted, manufacturers sometimes develop ‘device-intensive routes’ over potentially superior alternative delivery approaches that are less patentable.

13. Policy Reform Architecture

The Federal Circuit Path

The January 2025 ruling is the most significant near-term policy development because it does not require legislative action. It operates through judicial interpretation of existing Hatch-Waxman statute. Its implementation is immediate for new Orange Book listing decisions and its retroactive effect on existing listings is being worked out through the FTC enforcement process and ongoing litigation.

The limits of this approach are equally important. The Federal Circuit ruling addresses which device patents can be listed in the Orange Book, not whether device patents are valid or patentable. A device patent that does not meet Orange Book listing criteria still exists, still must be cleared in a Freedom to Operate analysis, and can still be enforced in district court litigation outside the Hatch-Waxman framework. The ruling removes one specific strategic tool — the 30-month ANDA stay — without eliminating the underlying patent.

Orange Book Transparency Reform

Several policy proposals call for an Orange Book annex or companion register specifically covering device patents that are approved for use with combination products, even where they do not meet the drug-listing criteria. This transparency measure would allow regulators, generic manufacturers, and payers to understand the full device patent landscape for any combination product without relying on formal Orange Book listing as the signal.

The practical benefit is significant: a generic manufacturer seeking to design around device patents currently has no centralized registry to consult. An NDA holder’s device patents are scattered across USPTO records without an obvious product-level organizational structure. A combination-product device patent annex, even without creating new exclusivity rights, would reduce the search costs and uncertainty that currently deter ANDA filings on combination products.

Heightened Utility Standards for Secondary Pharmaceutical Patents

India’s Section 3(d) approach — requiring demonstrably enhanced efficacy for patents on new forms of known substances — has not been adopted in the U.S. or EU. Adapting an analogous standard for device patents would require showing measurable clinical improvement (a defined threshold for lung deposition, injection accuracy, patient adherence outcomes, or safety) as a prerequisite for Orange Book listing eligibility, even for patents that otherwise satisfy novelty and non-obviousness requirements.

This approach faces resistance from two directions. The pharmaceutical industry argues it would impose an FDA-like clinical review burden on patent prosecution, which is outside the USPTO’s mandate. Patent purists argue that non-obviousness is the appropriate standard for innovation quality and that additional utility requirements distort the patent system. These are not trivial objections. But Section 3(d) has functioned in India for 20 years without destroying pharmaceutical innovation in the market — a fact that proponents of the approach cite in their favor.

The PREVAIL Act Counterweight

The Patent and Trademark Appeal and Validity Improvement of Litigation (PREVAIL) Act, which advanced out of the Senate Judiciary Committee in November 2024, would raise the standard for invalidating patents at PTAB by increasing the burden of proof for invalidity challenges. If enacted, it would make IPR petitions against device patents — currently one of the primary tools for clearing patent thickets before generic entry — materially harder to succeed on.

The PREVAIL Act’s proponents argue it corrects an imbalance created by PTAB’s historically high patent invalidation rates. Critics counter that PTAB’s invalidation rates for pharmaceutical patents are lower than the aggregate figures suggest: as of early 2024, only 15% of petitions challenging small-molecule drug patents resulted in final written decisions invalidating all claims. The PREVAIL Act, if passed, would affect the economics of device patent challenges in ways that partially offset the FTC enforcement gains.

14. The Next Frontier: Smart Devices, Digital Integration, and the Coming Patent Wave

Connected Inhalers and Dose Tracking

GSK’s ELLIPTA inhaler line and Teva’s Digihaler both incorporate electronics: dose counters, electronic sensors tracking when doses are taken, and Bluetooth connectivity for data transmission to companion apps. These digital features are separately patentable from the mechanical inhaler components. They also create genuinely new patent claims that do not merely cover the API — they cover software architecture, sensor design, and data processing algorithms.

The clinical evidence for connected inhaler outcomes is mixed. Studies show that digital dose tracking can improve adherence in some patient populations, but the magnitude of improvement varies significantly across trials. Whether adherence improvements are large enough to meet a proportionate-benefit test for device evergreening purposes is an open question. For the companies filing these patents, the question is less about clinical thresholds and more about prosecuting enforceable claims that extend Orange Book coverage or create FTO barriers for generic digital inhaler entrants.

The strategic dynamic here is the same as the CFC-to-HFA transition: a regulatory or market shift (in this case, toward digital health integration and reimbursement models tied to adherence monitoring) creates both genuine clinical opportunity and patent prosecution opportunity. The two are not mutually exclusive, but they are also not identical.

Closed-Loop Insulin Delivery and Algorithm Patents

The integration of CGMs, insulin pumps, and automated dosing algorithms in closed-loop systems creates a category of IP that is part device, part software, part method-of-treatment. Medtronic’s MiniMed, Insulet’s Omnipod 5, and Tandem’s Control-IQ all rely on proprietary control algorithms that determine how much insulin to deliver based on CGM readings.

Method-of-treatment patents on these algorithms — covering the decision logic for automated insulin dosing — may qualify for Orange Book listing to the extent they claim a method of using the drug (insulin). This is fertile ground for a new generation of evergreening in the diabetes device category, and it is not yet subject to the same regulatory attention as mechanical device patents.

For the next 10 years, algorithm and software patents will be the primary IP battleground for insulin delivery. The competitive question is not whether generic insulin can enter the market — it can, and biosimilar insulins are now available — but whether any biosimilar insulin can be paired with a fully functional closed-loop delivery system without infringing on proprietary algorithm patents. That technical barrier may prove more durable than any mechanical device patent.

GLP-1 Next-Generation Delivery and Oral Formulations

Novo Nordisk’s oral semaglutide (Rybelsus) and several pipeline oral GLP-1 formulations represent an interesting IP category: they use proprietary absorption-enhancing technology (the SNAC co-absorption system for semaglutide) that is itself patentable, even though the molecule is semaglutide. An oral delivery technology for a previously injectable compound creates a genuine innovation — the clinical differentiation from injectable semaglutide is real — but it also creates a new patent stack for the same molecule.

Whether oral delivery patents qualify as device-type evergreening under any definition depends on whether the SNAC system is classified as a device component, a formulation, or a novel drug product in its own right. The regulatory classification affects Orange Book listing eligibility, FTC scrutiny risk, and the standard for proportionate-benefit analysis.

15. Key Takeaways

On the core data: Device patents exist for 90% of studied medicine/device combination products. They extend exclusivity by a median of 4.7 years beyond the last-to-expire active ingredient patent, with the range reaching 15.2 years. For 14 of 49 studied products, device patents were the only remaining patent category. The Combivent Respimat architecture has sustained patent protection on two molecules that went generic in the 1980s through to at least 2030 — a 60-year exclusivity span for ipratropium.

On the regulatory shift: The Federal Circuit’s January 2025 ruling that Orange Book listing requires a patent to claim the active ingredient fundamentally changes the legal architecture of device patent blocking under Hatch-Waxman. Pure device patents without active ingredient claims are no longer viable Orange Book assets. Any LOE model that does not adjust for this ruling is using an outdated framework.

On the FTC campaign: By May 2025, the FTC had challenged over 600 device patent listings across multiple rounds of enforcement action. Several hundred patents have been removed. The companies that stood firm — AstraZeneca, Boehringer Ingelheim, Teva in the initial inhaler actions — now face both litigation risk and the Federal Circuit standard. The FTC has indicated it may expand scrutiny to packaging and manufacturing patents, extending the scope of the campaign beyond pure device claims.

On the economic stakes: The 2021-2030 federal deficit reduction estimate from addressing evergreening is $10 billion, with $7 billion in Medicare Part D drug cost savings. These are conservative figures that predate the GLP-1 era. If device patents on semaglutide and tirzepatide delivery systems are successfully listed and sustained, the decade-long cost to Medicare will be substantially higher.

On the innovation question: Some device improvements have genuine clinical value. The patent system does not currently evaluate clinical value; it evaluates novelty, utility, and non-obviousness. A spring-loaded locking assembly on an auto-injector is patentable on non-obviousness grounds without any clinical trial supporting its therapeutic advantage. The gap between patentability and clinical proportionality is where the policy debate sits, and it has not been resolved by any of the regulatory actions taken through 2025.

On the investment implications: For analysts, the post-Federal Circuit landscape requires product-by-product device patent audit against the ‘claims the active ingredient’ standard. The GLP-1 device patent portfolios are the single most consequential unresolved IP question in the pharmaceutical sector in terms of revenue at stake. Algorithm and software patents on closed-loop insulin delivery represent the next phase of the problem, arriving in a regulatory category that current Orange Book reforms have not yet addressed.

16. Frequently Asked Questions

What is the legal definition of patent evergreening?

No U.S. statute defines evergreening. The term describes a practice: obtaining secondary patents on existing products to extend exclusivity beyond what the original compound patent would have provided, without delivering a proportionate clinical benefit. The Beall et al. study proposed two definitions — a general form (no proportionate benefit of any kind) and a health-specific form (no proportionate improvement in standard of care). Neither is codified, which is why regulatory responses have focused on patent listing eligibility rather than on defining and prohibiting evergreening directly.

What is the median additional exclusivity that device patents add to combination products?

Research on 49 medicine/device combination products found that device patents extend exclusivity by a median of 4.7 years beyond the last-to-expire active ingredient patent. The range runs from 1.3 years at the low end to 15.2 years at the high end.

What did the Federal Circuit rule in January 2025?

The Federal Circuit held that to be eligible for Orange Book listing, a patent must claim the drug for which the NDA was approved, and that to claim the drug, the patent must claim at least the active ingredient. Patents covering only device components of a combination product NDA are ineligible for listing. This ruling means device-only Orange Book listings no longer generate enforceable 30-month ANDA stays against generic filers.

How many device patents has the FTC challenged?

Through May 2025, the FTC challenged over 600 device patent listings across three rounds of enforcement actions beginning in November 2023. Several hundred patents have been removed from the Orange Book following FTC action. The FTC has specifically targeted inhaler device patents (AstraZeneca, Boehringer Ingelheim, Teva) and auto-injector patents on weight-loss and diabetes delivery devices (Novo Nordisk, Eli Lilly) as of the April 2024 and May 2025 rounds.

Does India’s Section 3(d) address device evergreening?

Not directly. Section 3(d) of the Indian Patents Act limits patents on new forms of known substances unless they show significantly enhanced efficacy. It was designed to address small-molecule formulation evergreening. A mechanical delivery device does not fit the ‘new form of a known substance’ framework, so device patents largely escape Section 3(d) scrutiny in India. Anti-evergreening provisions tailored to device patents do not currently exist in any major pharmaceutical patent jurisdiction.

What should IP teams do now given the Federal Circuit ruling?

Four immediate priorities: audit every device patent currently listed in the Orange Book against the ‘claims active ingredient’ standard; assess litigation and FTC dispute exposure for listings that fail that standard; review prosecution strategy for pending device patent applications to incorporate active ingredient claim elements where the combination is novel; and update LOE models for any combination product whose blocking function depended primarily on pure device patent listings.

Drug patent expiry dates are subject to change based on patent term extension applications, PTAB proceedings, litigation outcomes, and ongoing FTC enforcement actions. Nothing in this article constitutes legal or investment advice.

")