Section 1: The European Generic Market: Scale, Drivers, and the Illusion of Uniformity

Sizing the Prize Accurately

The European generic drug market carries a valuation somewhere between USD 74.8 billion and USD 87.5 billion as of 2023, depending on methodology. The spread is not a reporting error. It reflects genuine definitional ambiguity: some datasets fold branded generics into the figure, others include biosimilars, and currency conversion timing distorts year-on-year comparisons when the euro moves sharply against the dollar. The compound annual growth rate cited across major market research houses sits between 7.0% and 8.4%, projecting a market of USD 161.7 billion to USD 228.8 billion by 2032.

Analysts who anchor on the midpoint of these ranges miss a more informative signal. The variance itself reveals the market’s structural complexity. A strategist treating Europe as a single revenue pool will misallocate capital just as surely as one who ignores the continent entirely. The useful frame is not “what is the market worth” but “what is each country worth to this specific molecule, at this specific stage of its exclusivity lifecycle.”

Generics account for roughly 70% of all prescription volume dispensed across Europe but less than 30% of total pharmaceutical expenditure. That asymmetry is the core economic logic of the generics business on this continent: massive volume, thin unit economics, and a value proposition that is entirely built around cost displacement.

The Four Structural Growth Drivers

Cost-Containment as Policy Mandate. European healthcare budgets face structural deficits driven by aging populations, the chronic disease burden, and the relentless price appreciation of novel biologics. Generics, which typically undercut originator prices by 20% to 90%, sit at the center of every national payer’s cost-reduction toolkit. This is not passive demand. Governments across the continent have embedded generic promotion into prescribing regulations, pharmacist substitution rules, and reimbursement architecture. The result is a market that grows not because patients prefer generics, but because every payer-facing incentive in the system pushes toward them.

The Patent Cliff of 2025 to 2030. The loss of exclusivity (LOE) wave building between now and the end of the decade will, by some industry estimates, expose over USD 220 billion in global branded revenue to generic competition. Europe is a primary theater for this transition. The most consequential LOEs over the next five years include apixaban (Eliquis, BMS/Pfizer), dulaglutide (Trulicity, Eli Lilly), pembrolizumab (Keytruda, Merck), nivolumab (Opdivo, Bristol Myers Squibb), palbociclib (Ibrance, Pfizer), and enzalutamide (Xtandi, Pfizer/Astellas). The IP valuation and competitive implications of each are examined in detail in Section 2.

Demographic and Epidemiological Shift. More than 20% of EU citizens are now aged 65 or older. That share will reach approximately 30% by 2050. An aging population produces durable, high-volume demand for chronic disease medications across cardiovascular, metabolic, oncological, and respiratory indications. These are precisely the therapeutic classes where major patent expirations are concentrated. Demand for affordable versions of these drugs is structural, not cyclical.

The Evolution Toward Complex and Specialty Generics. The market is bifurcating. Standard small-molecule generics face brutal price competition in mature markets. The growth margin lies in complex generics and value-added medicines (VAMs): products with complex delivery mechanisms such as inhalers, auto-injectors, or transdermal patches; modified-release formulations that extend dosing intervals; fixed-dose combinations; and new routes of administration. The specialty generics segment is projected to nearly double from approximately USD 21.5 billion in 2024 to USD 42 billion by 2033. These products carry higher development costs and more complex bioequivalence hurdles, but also face fewer competitors and support more sustainable pricing.

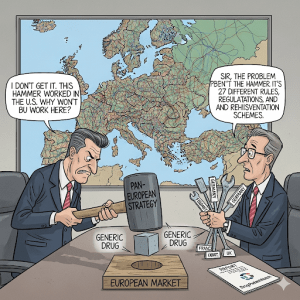

Why the ‘Single Market’ Frame Is Analytically Wrong

The EU’s framework for free movement of goods and the EMA’s centralized approval system create a plausible illusion of a unified pharmaceutical market. That illusion collapses at the national border. The levers that actually determine whether a generic drug earns money, which are pricing, reimbursement listing, and substitution policy, are the exclusive domain of the 27 individual Member States. No EU institution sets drug prices. No central body compels national payers to reimburse any specific product.

The practical consequence is that generics account for over 80% of prescription volume in Germany and the UK, while the figure sits at roughly 19% in Italy and around 30% in France. A company that wins the German tender market and assumes France will follow the same commercial logic will be wrong on pricing structure, wrong on the stakeholder map, wrong on the timeline, and wrong on the required organizational capabilities.

The “best” European market is not a fixed answer. It is specific to the molecule, the company’s cost structure, its regulatory and government affairs capabilities, and its risk appetite. A low-cost producer with world-class supply chain management has a different optimal entry sequence than a specialty-focused company with a complex injectable and a strong medical affairs function.

Key Takeaways: Market Structure

The European generic market is large and growing, but its growth is unevenly distributed across geographies and product classes. The headline CAGR figures are useful for investor presentations but inadequate for launch planning. The penetration gap between high-volume markets like Germany and low-penetration markets like Italy reflects different policy architectures, not different levels of generic quality or patient preference. Low-penetration markets often represent higher margin potential for companies willing to invest in sophisticated market access. The bifurcation between standard generics and complex generics is permanent and deepening. Any company that treats Europe as a single commercial unit will underperform against those that do not.

Section 2: The Patent Cliff, Drug-Level IP Valuation, and What Analysts Get Wrong

How to Value a Drug’s IP Position as a Core Asset

Before a generic company can price a European launch opportunity, it needs a precise assessment of the IP value embedded in the originator product it is targeting. That value is not the drug’s annual sales figure. It is a function of the remaining exclusivity runway, the probability that key patents survive a challenge, the number and quality of secondary patent claims that could be asserted against a generic entrant, the SPC expiry timeline, and the litigation history in each target jurisdiction. A drug generating EUR 3 billion per year with one strong composition-of-matter patent expiring in 24 months and no SPC is a categorically different opportunity from a drug generating EUR 3 billion with a fresh SPC plus a dense thicket of formulation and dosing patents.

Generic companies and their investors frequently value these opportunities as simple discounted cash flow exercises anchored on current brand revenue. That approach ignores the downside risk of litigation-driven delay and overstates the attainable price, particularly in markets like Germany where Day 1 competition from multiple entrants compresses margins within weeks. The following drug-level analyses apply a more granular framework.

Apixaban (Eliquis): BMS/Pfizer IP Valuation

Apixaban is a Factor Xa inhibitor marketed as Eliquis by Bristol-Myers Squibb and Pfizer. With over USD 12 billion in annual sales at peak, it is one of the most valuable generic entry opportunities of the current decade.

The core composition-of-matter patent for apixaban expired in Europe in 2022, but BMS and Pfizer held a combination of national SPCs and patent family continuations that extended exclusivity in some markets into 2026. Generic companies including Teva, Sandoz, and several Indian API manufacturers began staging European launches accordingly. The IP asset value that BMS embedded in apixaban over its commercial life included not only the base molecule patent but a secondary patent portfolio covering specific crystalline polymorphs, specific salt forms, and the 2.5 mg and 5 mg tablet formulations, each of which carries its own potential SPC eligibility.

For an investor evaluating a generic apixaban play, the relevant calculation is not the EUR 12 billion revenue figure but the addressable market post-LOE in each specific country, discounted by the probability and duration of patent litigation on secondary claims, adjusted for the likely number of Day 1 entrants, and further compressed by the specific P&R mechanics of each national market. In Germany, where the Sickness Funds will tender apixaban generics against each other, the competitive price will likely settle at 70-80% below the pre-expiry originator price within the first tender cycle. In France, the first generic must enter at a mandatory 60% discount to the originator, with further negotiated reductions over time.

The IP asset value of Eliquis for BMS/Pfizer is also visible in its evergreening approach: the companies have pursued patents on specific dosing regimens for indications like stroke prevention in atrial fibrillation, creating a further layer of claims that generic companies must either design around or challenge. A Freedom-to-Operate analysis for apixaban in Europe requires parsing not just the SPC landscape but the specific indication-by-indication claim structure in each target market.

Dulaglutide (Trulicity): Eli Lilly IP Valuation

Dulaglutide is a GLP-1 receptor agonist that Eli Lilly markets as Trulicity, with approximately USD 7 billion in peak annual sales. The first European biosimilar pathways for dulaglutide are expected to open around 2027, though the precise timeline depends on SPC status in individual markets.

The IP structure of dulaglutide is more complex than a small molecule. As a biologic, the core patents cover not just the amino acid sequence but the Fc-fusion protein architecture, the specific glycosylation profile, the prefilled single-dose pen delivery device, and the manufacturing process. The manufacturing process patents are a particularly critical variable for biosimilar developers, because they are often where originators litigate most aggressively. A biosimilar manufacturer that replicates the molecule but uses a process that a court finds infringes Lilly’s manufacturing IP faces injunction risk even after the primary sequence patent expires.

From an investment standpoint, the dulaglutide biosimilar opportunity in Europe is less about Day 1 revenue capture and more about the 3-to-5-year trajectory. Early entrants will need to invest heavily in clinical comparability studies, physician education, and the trust-building process that biosimilar uptake requires. The European GLP-1 market is also complicated by the entry of next-generation originator molecules like semaglutide (Ozempic, Wegovy) and tirzepatide (Mounjaro), which will compete with generic dulaglutide for formulary position and physician preference in type 2 diabetes management.

Pembrolizumab (Keytruda) and Nivolumab (Opdivo): The Checkpoint Inhibitor Cliff

Pembrolizumab (Merck’s Keytruda) and nivolumab (Bristol Myers Squibb’s Opdivo) are PD-1 inhibitor monoclonal antibodies that together represent tens of billions in annual revenue. Both face LOE in 2028, making the period from 2025 to 2028 a critical window for biosimilar development programs.

The IP architecture around checkpoint inhibitors is notably complex. Merck has assembled a portfolio of patents covering the pembrolizumab molecule, its specific manufacturing processes, specific dosing regimens (including the flat dosing at 200 mg Q3W and 400 mg Q6W), specific clinical indications, and combination use with chemotherapy. The combination-use patents are a particular concern for biosimilar manufacturers, because the most commercially valuable pembrolizumab revenue comes from first-line combination regimens. A biosimilar that is approved as a monotherapy biosimilar but lacks freedom to operate in the combination setting may find its commercial uptake sharply limited, since oncologists will default to the combination regimen label.

The onco-biosimilar market in Europe is also complicated by payer attitudes. Many national oncology treatment guidelines are updated slowly, and formulary committees in European hospitals can be reluctant to substitute in active cancer treatment regimens, even where the science strongly supports biosimilar equivalence. Investor models for checkpoint inhibitor biosimilars should build in a 12-to-24-month lag between regulatory approval and meaningful formulary access in the major European oncology markets.

Palbociclib (Ibrance) and Enzalutamide (Xtandi): The Oncology Pill Cliff

Pfizer’s palbociclib (Ibrance), a CDK4/6 inhibitor for HR-positive breast cancer, and enzalutamide (Xtandi, co-developed by Pfizer and Astellas), an androgen receptor inhibitor for prostate cancer, both face European LOE around 2027.

Both drugs occupy high-revenue, high-visibility positions in their respective oncology indications. The IP valuation of each includes consideration of the crystal form patents (palbociclib has multiple crystal form applications), specific salt form patents, and the specific combination regimen patents. The enzalutamide patent estate is particularly dense, with Pfizer and Astellas having pursued extensive secondary patenting that generic challengers will need to navigate carefully.

For a generic company planning a 2027 European launch of either product, the critical variables are: the outcome of any pending patent litigation in key markets, the SPC expiry date in each jurisdiction (which can vary by up to 12 months across Member States for the same molecule), and the speed with which national health authorities update their oncology treatment guidelines to reflect generic availability.

What Analysts Get Wrong About Patent Cliff Valuation

The most common analytical error is treating LOE as a binary event. Revenue does not go to zero at patent expiry; it erodes over a multi-year period at rates that vary enormously by country. In Germany, price erosion is rapid and severe, with generic prices settling at 70-90% below the originator within 18-24 months of first generic entry. In France, the 60% mandated discount at launch is followed by further CEPS-negotiated cuts, but the pace is slower and more predictable. In Italy, the AIFA negotiation process can mean that generics do not reach the market until 12-24 months after the basic patent expires, which compresses the commercial window for early movers.

Analysts also frequently undercount the number of Day 1 entrants in major generic categories. For a product as large as apixaban, 10 to 15 generic companies will have prepared simultaneous launch packages. The winner-takes-all dynamics of the German tender market mean that most of these companies will capture minimal German revenue, regardless of their Day 1 regulatory readiness. Portfolio strategy matters more than individual product launches: a company that loses the apixaban tender in Germany but wins on two other molecules in the same therapeutic area can still generate acceptable returns.

Key Takeaways: IP Valuation

Drug-level IP valuation in Europe requires a country-by-country SPC map, a litigation probability assessment for secondary patents, and a realistic Day 1 entrant count. The patent cliff is not a single date; it is a multi-year erosion curve with a country-specific shape. Biologic LOEs require additional analysis of manufacturing process patents, clinical indication coverage, and payer attitude to biosimilar substitution. The difference between the first and third generic entrant in Germany can mean the difference between capturing 40% of the tender volume and capturing nothing. Biosimilar investors in checkpoint inhibitors need to model a longer access ramp than small molecule generics, given oncology formulary conservatism.

Investment Strategy: The Patent Cliff

Institutional investors building a generics-focused position ahead of the 2025-2030 cliff face a specific selection problem: the publicly visible LOE dates do not differentiate between companies that have done the IP work and those that have not. A generic manufacturer announcing a palbociclib launch for 2027 that has not resolved freedom-to-operate on the CDK4/6 crystal form patents is a very different risk profile from one that has secured a clear FTO opinion or has a challenge patent proceeding already underway.

The most informative leading indicators are: the existence and outcome of Paragraph IV-equivalent patent challenge proceedings in the US (which often presage European strategies), the filing history in national patent offices for secondary claims, the track record of the company’s IP litigation team, and the depth of its regulatory dossier preparation evidenced by bioequivalence study initiation timelines. Companies with a structured IP intelligence function using platforms like DrugPatentWatch to track the full patent family, SPC filing history, and litigation docket in each European jurisdiction are categorically better positioned than those relying on headline patent expiry databases.

Section 3: The Four Regulatory Pathways: A Strategic Decision Matrix

The Marketing Authorisation: What It Does and Does Not Grant

A Marketing Authorisation (MA) in Europe grants the holder the legal right to place a product on the market in the covered territory. It does not grant the economic right to have that product reimbursed. These are separate rights governed by separate bodies. This distinction is the single most important regulatory concept for any company entering Europe from a US or emerging market background, where FDA approval is closely linked to commercial access. In Europe, the EMA’s scientific opinion is the beginning of the commercial process, not the conclusion.

For a generic or hybrid application, the core regulatory requirement is demonstrating that the product contains the same active substance as the reference medicinal product, has the same pharmaceutical form and route of administration, and is bioequivalent based on appropriate pharmacokinetic studies. The standard is governed by EMA Guideline CPMP/QWP/EWP/1401/98, which sets the bioequivalence acceptance criteria at a 90% confidence interval of 80.00-125.00% for Cmax and AUC.

The Centralised Procedure: Pan-European Scope, Significant Operational Load

The Centralised Procedure (CP) routes a single application through the EMA to the European Commission. The CHMP conducts the scientific assessment over a standard 210-day clock, with clock stops permitted for applicant responses. A positive CHMP opinion leads to a Commission decision, typically within 67 days, which grants a single MA valid across all 27 EU Member States plus Iceland, Liechtenstein, and Norway.

The CP is mandatory for products derived from biotechnology processes, treatments for cancer, HIV, diabetes, neurodegenerative diseases, and designated orphan medicines. For generic manufacturers, the CP is automatically available for any generic whose reference product was approved through the CP. It can also be accessed for nationally-approved reference products if the applicant can demonstrate scientific, technical, or public health interest at Union level.

The strategic case for the CP is clear when the product is a generic of a major CP-approved blockbuster and the company has the commercial infrastructure to execute simultaneous launches across multiple markets. The operational requirements are substantial: all labeling must be prepared in all EU official languages before approval, country-specific packaging must be ready, and national P&R dossiers must be prepared in parallel with the regulatory process because reimbursement decisions happen after MA, not simultaneously.

The CP is not always the optimal choice even for eligible products. A company that intends to launch in only five markets in Year 1 is absorbing the full regulatory and labeling cost of a 30-country approval for no commercial benefit in the markets it will not enter. For those companies, the Decentralised Procedure may be more capital-efficient.

The Decentralised Procedure: Targeted Multi-Country Launch

The Decentralised Procedure (DP) allows simultaneous submission to multiple national competent authorities for a product that has no existing MA in any EU country. The applicant designates one country as the Reference Member State (RMS) and identifies the remaining target countries as Concerned Member States (CMS). The RMS leads the scientific evaluation, prepares the draft Assessment Report, and circulates it to CMS for comment. Successful completion yields national MAs in all participating countries simultaneously.

The DP suits companies targeting a strategic cluster of markets. Common clusters are the five major economies (DE, FR, UK, IT, ES), the Nordic group (DK, SE, FI, NO), and Benelux. The DP requires careful RMS selection: a country chosen for its scientific predictability and speed of assessment, balanced against the commercial importance of the market. Germany’s BfArM and Sweden’s MPA are frequently chosen as RMS based on their track records of efficient assessment.

The practical limitation of the DP is that any CMS can raise an objection during the procedure, potentially triggering a formal Coordination Group process that extends the timeline. Companies should conduct a pre-submission assessment of potential objection risk in each proposed CMS based on the specific product profile and any known regulatory sensitivity in those jurisdictions.

The Mutual Recognition Procedure: The Phased Rollout Architecture

The Mutual Recognition Procedure (MRP) is available only after an MA has already been granted through a National Procedure in one EU Member State. That country becomes the RMS for the mutual recognition process, and other Member States are invited to recognize the existing approval. The MRP is the preferred mechanism for a phased, sequential launch strategy.

The strategic value of the MRP is risk mitigation and cash flow management. A company that uses the National Procedure to launch first in Germany, generating early revenue from the German tender market, can then use the German MA as the basis for MRP applications into Austria, the Netherlands, and Poland, funding the expansion from operational cash flow rather than upfront capital. The learning from the German launch also informs the commercial and regulatory approach in subsequent markets.

The limitation of the MRP is that the initial national MA scope limits the subsequent recognition application. If the German MA includes labeling restrictions or conditional requirements that differ from what a CMS would accept, those issues must be resolved before recognition can proceed.

The National Procedure: The Single-Market Beachhead

The National Procedure involves a direct application to a single national competent authority, BfArM in Germany, ANSM in France, MHRA in the UK post-Brexit, AEMPS in Spain, AIFA in Italy. The resulting MA is valid in that country only.

The NP is the correct choice for companies with a limited geographic scope, those entering Europe for the first time with one priority market, or those developing a beachhead strategy that will later be extended via MRP. It is also the only option for the UK post-Brexit, since the UK’s MHRA no longer participates in the EMA’s mutual recognition or decentralized procedures.

Regulatory Pathway Decision Matrix

The choice among these four pathways depends on the intersection of six variables: the number of target markets in Year 1, the reference product’s original authorization route, the company’s translingual labeling capacity, the commercial launch timeline pressure, the regulatory track record of candidate RMS countries, and whether the company intends to use the MRP for sequential expansion. A company that has a CP-approved reference product, plans to launch in 15 or more markets within 18 months of LOE, and has pan-European commercial infrastructure should use the CP. A company planning to launch in Germany first and expand later should use the German NP followed by MRP. A company targeting the Nordic cluster with no existing EU presence should evaluate the DP with Sweden as RMS.

Key Takeaways: Regulatory Pathways

The regulatory pathway choice is a commercial decision, not merely an administrative one. It determines launch timing, geographic scope, upfront cost, and the organizational demands placed on the regulatory and supply chain functions. The MA is the entry ticket; reimbursement is the match. A pan-European MA from the CP provides no commercial advantage in markets where the company is not prepared to execute a national P&R dossier. UK market access requires its own MHRA strategy independent of EMA procedures. RMS selection for DP applications should be based on assessment efficiency and commercial priority in equal measure.

Section 4: The Three-Dimensional IP Chessboard: SPCs, Bolar, and Patent Linkage

Layer One: Supplementary Protection Certificates (SPCs) in Full Technical Detail

A Supplementary Protection Certificate is a sui generis intellectual property right that comes into force at the expiry of the basic patent and extends market exclusivity for a product by up to five years. The extension is calculated using the formula: date of MA minus date of patent application, minus five years, with a maximum extension of five years. The paediatric extension under Regulation (EC) No 1901/2006 adds a further six months if the originator has completed an agreed Paediatric Investigation Plan, bringing the maximum total SPC duration to 5.5 years.

SPCs are granted at the national level by national patent offices. The same underlying European patent can generate SPCs with different durations in different Member States because the date of the first MA in the EU is used as a reference point, and administrative delays in obtaining the first MA can vary. For a generic manufacturer, this means the SPC expiry date for the same molecule may differ by 6 to 12 months across EU markets, requiring country-specific SPC mapping.

The SPC Manufacturing Waiver, introduced by Regulation (EU) 2019/933 and effective from July 2019, created two carve-outs from SPC infringement. First, EU-based manufacturers may produce an SPC-protected product for export to countries where the SPC has expired or never existed. Second, in the six months immediately before SPC expiry, manufacturers may produce and stockpile product for the EU market itself. The waiver requires compliance notification to the relevant national authority and the SPC holder, and the product must be clearly distinguished from the originator’s product (specific markings apply under the regulation).

The practical significance of the stockpiling waiver is substantial. Without it, a generic manufacturer could not legally manufacture product in the EU until the moment the SPC expired, creating a structural gap between the legal right to sell (Day 1) and the physical ability to deliver. The waiver closes that gap by allowing six months of pre-expiry production. Companies that use the waiver effectively can achieve genuine Day 1 supply to wholesalers and pharmacies across multiple markets simultaneously. Medicines for Europe continues to advocate for simplification of the notification requirements, which as currently structured create administrative friction that smaller manufacturers find burdensome.

The SPC system also intersects with the growing concept of second medical use patents. An SPC can only be granted for a product that is protected by a basic patent and for which a marketing authorisation has been obtained. Where an originator holds multiple SPCs for the same molecule based on different MAs (such as an MA for a new indication), generic companies need to assess which SPC protects which commercial use and whether their intended product and indications are genuinely within the scope of the SPC claims.

Layer Two: The Bolar Exemption: Scope, Fragmentation, and the Pharma Package Reform

The Bolar exemption permits generic manufacturers to conduct studies and trials needed to obtain a marketing authorisation without that activity constituting patent infringement. It was introduced at EU level by Directive 2004/27/EC amending Directive 2001/83/EC. The principle is straightforward: the time required to develop and file a generic regulatory dossier should not effectively extend the originator’s monopoly beyond the legal patent term.

The implementation of the Bolar exemption is not harmonized across Member States. Directive 2004/27/EC set a floor but not a ceiling, leaving Member States to define the precise scope of permitted activity. The resulting divergence is significant.

Italy has the broadest interpretation. Italian courts and scholars have read the Bolar exemption to cover studies conducted for the purpose of obtaining an MA anywhere in the world, not just in the EU. Italian law also extends protection to third-party suppliers of active pharmaceutical ingredients (APIs) that provide the patented compound to a generic company for the specific purpose of regulatory studies. This creates Italy as a jurisdiction of choice for early-stage bioequivalence work and API supply arrangements where the active ingredient is still under patent elsewhere.

Germany and the Netherlands have historically taken a narrower view, limiting the exemption to activities directly necessary for obtaining an EU MA. Activities conducted for the purpose of obtaining a US FDA approval, or for preparing an HTA submission without an MA application, have been treated as potentially infringing in some German case law.

The EU’s proposed new Pharmaceutical Legislation, which has been progressing through the legislative process since 2023, includes provisions that would expand the Bolar exemption to explicitly cover activities needed for pricing and reimbursement applications and HTA submissions. This is a meaningful practical improvement: currently, companies conducting pharmacoeconomic studies or preparing AMNOG dossiers for Germany while the basic patent is still in force face potential infringement exposure in some jurisdictions. However, industry observers have raised a legitimate concern that by specifying the exemption applies to ‘generic, biosimilar, hybrid, and bio-hybrid’ applications, the proposed text may inadvertently narrow the broader research exemptions that currently exist in countries like Italy and that protect innovative research activities as well.

The strategic implication for generic companies is that the choice of jurisdiction for pre-expiry R&D, bioequivalence studies, and API sourcing should be made with explicit reference to local Bolar interpretation. A study protocol signed off in Milan may be legally protected under Italian law while the same activity conducted from a German or Dutch laboratory would face litigation risk. Legal counsel experienced in the IP law of each specific Member State is not optional; it is core to the launch preparation process.

Layer Three: Patent Linkage: The Systemic Anti-Competitive Practice That Persists

Patent linkage is the practice by which national authorities responsible for granting marketing authorisations, pricing approvals, or reimbursement listings condition their decisions on the patent status of the reference product. The European Commission has declared this practice unlawful under EU competition law, ruling that national regulatory and pricing authorities are not competent to adjudicate patent validity, and that inserting a de facto patent enforcement role into the MA or reimbursement process amounts to an unlawful extension of the originator’s monopoly.

Despite this clear position, patent linkage persists in several EU Member States in various forms. Portugal has been one of the most problematic jurisdictions: the submission of a generic MA application has in practice been treated as a triggering event for originator patent litigation, creating a systematic pattern of pre-emptive injunctions against generic entry. The Portuguese pharmaceutical industry body and individual generic companies have documented cases where products were blocked from the market for 12 to 24 months based on patent claims that were subsequently invalidated.

France’s notification mechanism under the CEPS process operates as a soft form of patent linkage. When a generic company files for reimbursement listing, the pricing authority is required to inform the originator company. This notification is framed as a transparency measure but functions as a litigation trigger: originators routinely file patent infringement claims against the generic applicant within weeks of receiving the CEPS notification, often on the basis of secondary patent claims they know may not survive challenge but which cause enough delay and legal cost to impair the generic company’s commercial planning.

Hungary and Poland have required generic companies to submit formal declarations confirming they will not launch before relevant patents expire, in effect making the reimbursement process conditional on the patent landscape. This is a textbook form of patent linkage that compounds the delay already introduced by lengthy reimbursement negotiations.

The practical defense against patent linkage is a rigorous pre-launch patent validity analysis coupled with an aggressive litigation posture. Generic companies that quickly challenge secondary patents through invalidation proceedings in the relevant national patent courts or before national patent offices reduce the period of exclusivity that patent linkage can protect. Patent linkage is most potent when the originator’s secondary patents appear formidable on their face. Companies that have already secured a declaratory judgment of non-infringement, or that can point to a successful validity challenge in another jurisdiction, undermine the litigation threat that makes patent linkage effective as a delay tactic.

Key Takeaways: IP Navigation

The European IP landscape has three distinct layers, each requiring dedicated legal and strategic analysis. SPC expiry dates vary by country for the same molecule and must be mapped at a national level. The SPC Manufacturing Waiver enables pre-expiry stockpiling and export, but notification compliance is mandatory. The Bolar exemption has meaningfully different scope across Member States, and R&D location decisions should reflect local interpretation. Patent linkage persists despite being unlawful, and defense requires both proactive patent challenge proceedings and a litigation-capable IP team. A Freedom-to-Operate analysis that covers only the basic patent expiry date is inadequate for any product with a dense secondary patent portfolio.

Section 5: The Originator Playbook: Evergreening, Patent Thickets, and Authorized Generics

Understanding Evergreening as a Structured IP Strategy

Evergreening is the deployment of a portfolio of secondary patents to extend effective market exclusivity beyond the expiry of the core composition-of-matter patent. The practice is lawful where the secondary patents cover genuine innovations, and contested where they cover modifications that are obvious or trivially different from the original compound. In Europe, the European Patent Office (EPO) applies an inventive step standard that should, in theory, screen out low-quality secondary patents. In practice, the volume and complexity of secondary filings around major blockbusters create a patent thicket that can deter or delay generic entry regardless of the ultimate legal validity of any single claim.

The most commonly deployed evergreening tactics in European pharmaceutical markets include the following, in rough order of commercial impact.

Formulation Patents. These cover the specific physical or chemical form of a drug product: a specific crystal polymorph, a specific salt form, a specific amorphous form, or a specific particle size distribution. Formulation patents are among the most litigated categories in European pharmaceutical patent law because they often overlap with the core active ingredient in ways that are difficult to design around without changing bioequivalence characteristics.

Dosing Regimen and Method-of-Treatment Patents. These cover the specific dosing schedule or clinical indication for which a drug is approved. Method-of-treatment patents are generally not enforceable against generic manufacturers in Europe under the exemption for therapeutic methods, but dosing regimen patents can create legal exposure in jurisdictions that allow use-limited product claims.

Metabolite and Active Metabolite Patents. Where a drug’s pharmacological effect is mediated partly or fully by an active metabolite, the originator may hold separate patents on that metabolite compound. This is a common strategy in CNS and cardiovascular pharmacology. A generic manufacturer producing the parent compound may inadvertently infringe a metabolite patent in jurisdictions where the active metabolite claim is valid.

Chiral Switch and Enantiomer Patents. AstraZeneca’s strategy with omeprazole and esomeprazole is the most studied European example. After the omeprazole patent expired, AstraZeneca developed and patented the S-enantiomer, esomeprazole (Nexium), which it claimed had superior efficacy. Whether the incremental benefit was clinically meaningful was debated extensively, but the strategy gave AstraZeneca a new patent estate and a new SPC for esomeprazole, extending effective exclusivity in the proton pump inhibitor market by approximately a decade.

Device and Delivery System Patents. For products delivered via inhaler, auto-injector, or transdermal patch, the device itself is separately patentable. This is particularly relevant in respiratory medicine (where inhaler device patents are layered on top of drug compound patents) and in injectable biologics (where auto-injector platform patents can block biosimilar entry even after the molecule patent expires). GlaxoSmithKline, AstraZeneca, and Boehringer Ingelheim have all maintained dense inhaler device patent portfolios that have complicated generic and biosimilar respiratory product development.

Indication Extension Patents. New clinical indications approved for existing molecules generate fresh regulatory exclusivity periods under EU pharmaceutical law. A drug with a well-established primary indication that obtains approval for a new indication may be protected by a one-year regulatory data exclusivity period for the new indication under Article 10(5) of Directive 2001/83/EC, and by any underlying method patents covering the new use. Generic companies must carefully evaluate whether their proposed label overlaps with any exclusively-protected indication.

The Patent Thicket Problem: Quantitative Assessment

The concept of a patent thicket describes a dense cluster of overlapping IP rights around a single drug product, each requiring individual assessment, challenge, or avoidance. Analysis of the patent landscape around major European blockbusters typically reveals several layers of protection beyond the original composition-of-matter patent. A product like adalimumab (Humira, AbbVie) had over 100 patents filed in Europe covering the molecule, its manufacturing processes, formulations, and specific clinical uses. Navigating that thicket required biosimilar developers to conduct extensive FTO analyses, file multiple revocation proceedings at the EPO and national courts, and in several cases accept modest delays in exchange for litigation settlements.

The cost of thicket navigation is significant. Legal and regulatory costs associated with patent challenges for a major biologic product in Europe can exceed EUR 10 to 20 million per molecule across the full portfolio of national proceedings. For small-molecule products with 10 to 20 secondary patents, the cost is lower but still material. Generic companies that factor these costs into their opportunity assessments and budget for them explicitly will make better capital allocation decisions than those that treat patent challenge costs as unexpected expenses.

Authorized Generics: The Originator’s Commercial Defense

An authorized generic (AG) is a version of a branded product manufactured under the originator’s NDA or MA, typically launched either directly by the originator or through a licensee at or shortly after the point of generic entry. The AG strategy is more commonly deployed in the US (where it interacts with the 180-day Hatch-Waxman exclusivity period) but exists in European markets as well, particularly for products where the originator decides that capturing part of the generic market is preferable to watching revenue erode entirely to independent generic manufacturers.

In Europe, authorized generics can take the form of a “pseudo-generic” where the originator launches a lower-priced branded version under the same MA (sometimes called a “flanker brand”) or a licensed generic supplied through a partner distributor. France’s mandatory originator price cut of 20% at the moment of generic entry is in part designed to keep originator brands competitive without requiring a separate AG strategy. In Germany, originators sometimes participate directly in Sickness Fund tenders through rebate contract bids, effectively competing with independent generic manufacturers for the same tender volume.

Key Takeaways: Originator Strategy and Generic Defense

Originators deploy evergreening across six primary patent categories, each requiring its own FTO assessment. The patent thicket around major blockbusters can include more than 100 distinct claims, each requiring individual evaluation. Budget for thicket navigation explicitly: EUR 10 to 20 million for a major biologic patent challenge is not exceptional. Authorized generic strategies by originators compress the margin available to independent generic entrants, particularly in Germany’s tender market. Chiral switch and indication extension strategies can grant effective exclusivity extensions of 5 to 10 years beyond the core compound patent. AstraZeneca’s esomeprazole strategy remains the most instructive case study in European pharmaceutical evergreening.

Section 6: Pricing and Reimbursement: Five Markets, Five Philosophies

The Architecture of European P&R Fragmentation

The EU’s founding treaties reserve healthcare system design and drug pricing as exclusive national competencies. No directive has harmonized the pricing mechanisms, no regulation has standardized the reimbursement criteria, and no EU body sets drug prices. The consequence for generic manufacturers is that securing a Marketing Authorisation is a necessary condition for commercial access but an entirely insufficient one. The real market access work begins after the MA is issued, in negotiations with national payers who operate under different legal frameworks, different philosophical orientations toward market competition versus regulation, and different institutional structures.

The five largest European pharmaceutical markets (Germany, France, the UK, Spain, and Italy) collectively represent the majority of European generic drug revenue. They also represent five structurally distinct pricing philosophies. Understanding each system at a mechanistic level, not just at a headline description level, is the prerequisite for building country-specific commercial strategies.

Germany: The Tender Market and Its Unsustainable Economics

Germany is Europe’s largest pharmaceutical market. Generics account for approximately 80% of prescription volume, making it the continent’s highest-penetration market. The GKV (Gesetzliche Krankenversicherung) system, composed of around 110 statutory health insurance funds (Sickness Funds), covers approximately 90% of the German population. The pricing architecture for off-patent drugs is built on three interlocking mechanisms: Rabattverträge (rebate contracts through tendering), Festbetrag (reference pricing), and mandatory statutory rebates.

Tendering (Rabattverträge). The dominant price-setting mechanism for the majority of the retail generics market is the competitive tender. Sickness Funds issue Ausschreibungen (tenders) for specific active ingredient-strength-form combinations, typically covering a two-year supply period. Companies submit sealed bids, and the Sickness Fund awards an exclusive supply contract to one or a small number of winning bidders. The winning criterion is almost always price: the lowest bid wins, and the winner captures the volume of all prescriptions filled by that Sickness Fund’s insured patients for that molecule during the contract period. Pharmacists are required by law to dispense the contracted product.

The tender market produces extreme price erosion. Average generic prices in Germany have declined in real terms even as overall consumer prices rose by approximately 30% over the last decade. Some analysis puts the average tender-winning price for major generic molecules at 70 to 90% below the originator price. Several major generic manufacturers have publicly disclosed that they have withdrawn products from the German market because no economically viable tender price was achievable given their cost of goods. This market failure dynamic, where unsustainably low prices reduce supply and threaten availability, has prompted policy debate within the German government, with proposals to introduce minimum price floors for generic tenders and to differentiate between European-manufactured products and those sourced from lower-cost manufacturing regions outside the EU.

Festbetrag (Reference Pricing). Products not covered by an exclusive tender contract operate under the Festbetrag system. The G-BA (Gemeinsamer Bundesausschuss, or Federal Joint Committee) establishes reference groups of therapeutically comparable products and sets a maximum reimbursement level for each group. Any product priced above the Festbetrag becomes co-payable by the patient, creating a powerful commercial incentive for manufacturers to price at or below the reference level.

Mandatory Statutory Rebates. Even outside the tender system, the law requires generic manufacturers to pay a statutory manufacturer rebate of 7% to the Sickness Funds, with an additional 10% rebate specifically applicable to off-patent drugs. These mandatory rebates are applied before any additional rebates negotiated in individual Rabattvertrag contracts.

The AMNOG process (Arzneimittelmarktneuordnungsgesetz) governs the benefit assessment of newly launched drugs, including high-value generics and biosimilars that may claim therapeutic differentiation. Under AMNOG, a company launching a product with a premium over the Festbetrag must submit a benefit dossier to the G-BA within three months of launch. The G-BA conducts an accelerated benefit assessment (Nutzenbewertung) and assigns the product an AMNOG rating. Products rated with no added benefit are automatically priced at the Festbetrag level. Products rated with added benefit enter price negotiations with the GKV-Spitzenverband. Biosimilar manufacturers claiming any clinical differentiation over the reference biologic must prepare for this process.

The strategic implication of the German system is unambiguous: success requires cost leadership above everything else. A company without a highly optimized API sourcing strategy, a lean manufacturing process, and a supply chain capable of operating at margins that are effectively zero or negative on individual tender contracts will struggle to maintain a sustainable German business. The portfolio approach is essential: revenue from other European markets and from non-tender German volume must cross-subsidize the competitive investment required to win major tender contracts.

France: Regulated Discounts, the TFR Mechanism, and CEPS Negotiations

France is a large market historically characterized by lower generic penetration than Germany or the UK, strong centralized state control over drug pricing, and a reimbursement architecture that prioritizes predictability over market competition. The Agence Nationale de Sécurité du Médicament (ANSM) handles marketing authorisations at the national level. The Comité Economique des Produits de Santé (CEPS) handles pricing negotiations.

The Mandatory First-Generic Discount. The price for the first generic entering the French market is set by law, not negotiation, at a 60% discount to the originator’s pre-expiry price. Simultaneously, the originator’s price is automatically reduced by 20%, narrowing the gap to 40 percentage points between originator and generic. This predictable pricing structure reduces negotiation uncertainty but also sets a floor from which further cuts are negotiated with the CEPS over the product’s commercial lifecycle.

The Tarif Forfaitaire de Responsabilité (TFR). The TFR is a rate-setting mechanism activated when the health insurance system (Assurance Maladie) determines that generic uptake in a specific therapeutic class is below target. When a TFR is declared, the national health insurance system caps reimbursement at the lowest-priced generic in the class. Patients who insist on the originator brand, or whose physician has specified the brand, pay the full difference between the TFR ceiling and the originator price out-of-pocket. This is a punitive measure designed to force substitution and has been highly effective in driving penetration in classes where it has been applied, including statins, proton pump inhibitors, and ACE inhibitors.

For generic companies, the threat of a TFR declaration is actually a useful signal: it indicates that the Assurance Maladie is committed to driving uptake in that class and will backstop generic access with policy tools. The risk is that the TFR mechanism can also compress pricing if multiple TFR-listed products compete for the same reimbursement ceiling. Companies should monitor TFR declarations actively and factor them into lifecycle pricing models.

CEPS Negotiations and ASMR Ratings. All pharmaceutical pricing in France is ultimately subject to negotiation with the CEPS. The Transparency Commission (Commission de la Transparence, part of the Haute Autorité de Santé, HAS) evaluates the clinical benefit of medicines and assigns both an SMR (Service Médical Rendu, or overall medical benefit) rating and an ASMR (Amélioration du Service Médical Rendu, or improvement in medical benefit) rating. ASMR I to III ratings indicate meaningful added clinical benefit and support premium pricing negotiations with the CEPS. ASMR IV indicates minor added benefit. ASMR V indicates no added benefit over the existing standard of care.

Standard generics are rated ASMR V by definition, since they offer no clinical improvement over the reference product. This limits the ceiling on CEPS negotiations but also focuses the strategic work squarely on lifecycle management: managing the inevitable further price cuts that follow the initial -60% launch price, driving substitution rates to avoid TFR exposure, and maintaining formulary access as payers periodically reassess pricing in mature therapeutic classes.

Early Access to innovative medicines in France operates through the ATU (Autorisation Temporaire d’Utilisation) mechanism, now replaced in part by the Accès Précoce and Accès Compassionnel frameworks. These mechanisms are relevant primarily for innovative products rather than generics, but knowledge of them is important for any company considering a hybrid regulatory strategy for a new formulation or indication of an established molecule.

United Kingdom: The Drug Tariff System and Post-Brexit MHRA Independence

The UK exited the EU’s regulatory framework on January 1, 2021. The Medicines and Healthcare products Regulatory Agency (MHRA) now operates as a fully independent regulator, no longer participating in EMA procedures. UK generic manufacturers must file separately with the MHRA, and EU MAs are not automatically recognized in the UK. The MHRA has established its own reliance procedure, under which it can rely on an EMA assessment to streamline its own review, but this requires a separate UK filing and the payment of UK fees.

For generic pricing, the UK operates through the Drug Tariff, a monthly publication by the NHS Business Services Authority that sets reimbursement prices for dispensed medicines. The Drug Tariff has four categories relevant to generics: Category A, Category M, Category C, and Category D. Category M drugs are those where the NHS has determined that adequate market competition exists to keep prices in check; these are repriced monthly based on actual market data submitted by pharmacies. Category A drugs follow a manufacturer’s published list price. The reimbursement price in the Drug Tariff is the amount paid to the dispensing pharmacy; the pharmacy then sources the product from a wholesale supplier at a price that may be significantly below the Drug Tariff rate, and the margin constitutes the pharmacy’s gross profit on that dispensing.

This architecture incentivizes pharmacies to source the lowest-cost available generic, regardless of brand, and has driven UK generic prices to among the lowest in Europe. The manufacturer selling price for major Category M generics is typically 70-90% below the pre-expiry originator price within 12 to 24 months of first generic entry, with no formal tender requirement and no government-negotiated ceiling. The price finding is entirely commercial.

The NHS Voluntary Scheme for Branded Medicines Pricing and Access (VPAS, the successor to the Pharmaceutical Price Regulation Scheme or PPRS) applies to branded originator medicines and complex branded generics, not to standard commodity generics. Companies operating in the UK generic market are not subject to VPAS but should monitor it as a benchmark for what NHS payers consider acceptable commercial terms for more complex products.

Post-Brexit regulatory divergence is creating increasing complexity for companies with pan-European portfolio strategies. Products approved via the EMA Centralised Procedure now require a separate UK filing. The MHRA’s pediatric requirements, its approach to biosimilar extrapolation, and its clinical data standards are gradually diverging from EMA standards as the MHRA develops its own regulatory identity. Companies must plan for dual regulatory development costs in portfolios that include both EU and UK as target markets.

Spain: The Reference Price System, ATC5 Controversies, and Regional Payers

Spain’s generic market has grown substantially since the introduction of systematic reference pricing in the 1990s. Generics now account for over 40% of prescribed units but only approximately 21% of total pharmaceutical expenditure, a direct reflection of the price compression achieved through the reference pricing system.

The Reference Price System (RPS). The Sistema de Precios de Referencia groups medicines into ‘therapeutic clusters’ and sets a maximum reimbursement price (precio de referencia) for each cluster. All products within the cluster, including the originator brand, are reimbursed up to this ceiling. Products priced above the ceiling are not reimbursed unless the prescribing physician specifically certifies the need for the higher-priced product, in which case the excess becomes the patient’s co-payment.

The grouping methodology has been controversial. Originally based on ATC5 classification (same active substance, same route of administration, same pharmaceutical form), recent reforms have moved toward broader ATC5 groupings that can include drugs with different active ingredients but similar therapeutic effects. This broader grouping means that a new generic could be benchmarked against a lower-priced comparator from a different molecule class, compressing the reference price below what the direct substitutability analysis would support. The Inter-Ministerial Pricing Committee (CIPM, Comisión Interministerial de Precios de los Medicamentos) reviews these groupings and sets the reference prices nationally.

The First Generic Price Requirement. The first generic entering the Spanish market must be priced at least 40% below the originator’s approved price at the time of entry. The originator is required to lower its price to remain within the reference group reimbursement ceiling, creating price convergence between brand and generic within each therapeutic cluster.

Regional Payer Fragmentation. Spain’s 17 Comunidades Autónomas (autonomous communities) are both the health authorities and the ultimate payers for most outpatient and hospital medicines. National CIPM pricing sets the ceiling, but the autonomous communities control formulary listings, hospital tender procedures, and regional prescribing guidelines. A product with full national P&R approval may face a second access hurdle at the regional level, particularly for hospital-only products, specialty drugs, and biologics. Companies targeting the major autonomous communities (Catalonia, Madrid, Andalusia, Valencia) should budget for separate regional engagement activities and KAM resources distinct from the national market access team.

The national pharmacovigilance center AEMPS also plays a role in generic substitution policy through its management of the official list of substitutable products. Prescribers and pharmacists in Spain rely on AEMPS guidance to confirm which generics are substitutable for which reference products.

Italy: AIFA Negotiations, Class A vs. Class H, and the 400-Day Clock

Italy has Europe’s fourth-largest pharmaceutical market and one of the most challenging environments for generic market access. The combination of a complex AIFA negotiation process, low existing generic penetration, and protracted timelines creates both barriers and opportunity: the barriers explain why so many companies underweight Italy in their launch strategies, and the opportunity reflects the headroom that low penetration leaves for companies willing to invest in the process.

AIFA Classification and Reimbursement. The Agenzia Italiana del Farmaco (AIFA) classifies medicines into reimbursement classes that determine the extent of national health service coverage. Class A medicines are fully reimbursed for all eligible patients. Class H medicines are available only in hospital settings under the hospital formulary system. Class C medicines are not reimbursed by the national health service and are purchased entirely at patient cost. For a generic to be commercially viable in Italy, Class A listing is typically required. Class H listing can provide hospital-channel access, which is critical for injectables, specialty drugs, and some oncology products.

The Negotiation Process. All pricing and reimbursement decisions in Italy go through direct negotiation with AIFA’s Pricing and Reimbursement Committee (Comitato Prezzi e Rimborso, CPR). Unlike France’s statutory 60% discount or Germany’s tender system, Italian pricing involves a face-to-face negotiation in which the company presents its value dossier and AIFA presents its assessment of the product’s budget impact and clinical value. For standard generics, AIFA requires a minimum 20% discount to the originator reference price as a starting point, but the actual negotiated price is determined by a broader assessment including the existing reference pricing framework, the number of already-listed generics in the class, and the budget impact on the SSN (Servizio Sanitario Nazionale).

Timeline Risk. The average time from MA submission to AIFA pricing and reimbursement decision has historically been well over 400 days, with the total timeline from originator LOE to listed generic exceeding 24 months in some cases. This delay reflects the complexity of the AIFA process, staffing constraints within the agency, and the negotiation-based architecture that requires multiple rounds of committee review. Italy’s slow P&R process effectively means that for a product with a 5-year exclusivity window post-LOE, a generic manufacturer may capture only 3 to 3.5 years of Italian revenue after accounting for the access delay.

The AIFA process has undergone reform efforts in recent years under the Italian government’s broader healthcare access agenda, including proposals to expedite Class A listing for generics where a therapeutically equivalent product is already listed at a similar price. Progress has been incremental.

The Prontuario and Regional Hospital Formularies. The Prontuario Farmaceutico Nazionale (PFN) is Italy’s national formulary for reimbursed medicines. Inclusion in the PFN is a necessary condition for national reimbursement. However, many hospitals maintain their own formularies (Prontuari Terapeutici Ospedalieri, PTOs), and hospital-administered medicines often require separate formulary inclusion at the institutional level even after PFN listing. For oncology products and specialty injectables, companies need dedicated hospital account management resources in Italy’s major treatment centers.

Comparative P&R Analysis: A Five-Market Reference Table

Feature

Germany

France

UK

Spain

Italy

Generic Penetration (Volume)

~80%

~30%

~83%

~47%

~19%

Primary Mechanism

Tendering (Rabattverträge)

Fixed Discount (-60%) + TFR

Market-based (Drug Tariff)

Reference Price System (RPS)

AIFA Direct Negotiation

First Generic Price

Tender-determined (typically -70 to -90%)

Mandatory -60%

Market-determined

Mandatory -40% minimum

Negotiated (minimum -20%)

Key Payer Body

Sickness Funds / GKV-Spitzenverband

CEPS

NHS / NHSBSA

CIPM + 17 Autonomous Communities

AIFA CPR

Originator Automatic Cut

No (tender competition only)

-20% at first generic entry

No (commercial response only)

Forced to reference price ceiling

Case-by-case

Speed to Market (Post-MA)

Fast (tender cycle driven)

Moderate (6-12 months)

Fast (Drug Tariff-listed quickly)

Moderate (CIPM process 6-9 months)

Slow (400+ days typical)

Key Risk for Generics

Race-to-bottom pricing; product withdrawal

Lifecycle price erosion; TFR threshold

Razor-thin margins; UK/EU dual filing

Regional access barriers; ATC5 grouping

Timeline; negotiation complexity

Mandatory Rebates

7% statutory + 10% off-patent rebate

No additional statutory rebate

None (margin model)

None (reference price ceiling)

Payback mechanism for budget overruns

Key Takeaways: P&R Systems

Germany and the UK use market mechanisms (tenders and commercial pricing) to achieve cost containment; France and Spain rely on mandated price formulas; Italy uses direct negotiation. None of these systems is a variation on a common theme: they are architecturally distinct. A single commercial playbook fails across all five markets simultaneously. The organizational requirements for success in Germany (tender management, supply chain efficiency, KAM relationships with Sickness Funds) are categorically different from Italy (government affairs, negotiation expertise, health economics). Companies building European commercial organizations must staff each market function against its actual requirements, not against a generic country-manager template.

Investment Strategy: P&R Systems

For institutional investors evaluating generic drug companies with European exposure, the P&R profile of a company’s portfolio is more predictive of margin trajectory than revenue. A portfolio heavily weighted toward Germany will show high volume but compressing margins, with potential product withdrawal risk in categories where no sustainable tender price exists. France provides predictable initial pricing but relentless lifecycle erosion. The UK delivers thin margins compensated by high volume and speed of market entry. Spain and Italy are longer-cycle, potentially higher-margin markets for companies willing to absorb the timeline. The most durable European generic business models are those with genuine pan-European diversification, reducing dependence on any single national pricing system.

Section 7: Health Technology Assessment Under the 2021 Regulation: What Actually Changes

The EU HTA Regulation: Mechanics and Scope

Regulation (EU) 2021/2282 on Health Technology Assessment became applicable in January 2025 for the first wave of qualifying products. The regulation creates a framework for Joint Clinical Assessments (JCAs) to be conducted by the HTA Coordination Group, a body composed of representatives from national HTA agencies across the EU. The JCA produces a common Union-level clinical assessment report evaluating a medicine’s relative clinical effectiveness and safety compared to one or more defined comparators.

The regulation’s application is phased by product category. From January 2025, it covers new cancer medicines and Advanced Therapy Medicinal Products (ATMPs). From January 2028, it extends to orphan medicines. From January 2030, it covers all medicines approved via the Centralised Procedure. Standard generics approved through national or decentralized routes are not mandated to undergo JCA, and this is unlikely to change in the near term.

The JCA process is limited to the clinical assessment. It evaluates endpoints specified by the manufacturer in the clinical dossier and assessed against the nationally-defined comparator. The resulting JCA report is advisory, not binding, for national HTA decisions. Member States are required to give JCA reports ‘due consideration’ but retain full authority to conduct their own additional assessments, to weight outcomes differently based on local healthcare priorities, and to reach independent pricing and reimbursement decisions.

What the HTAR Does Not Harmonize

The regulation explicitly excludes economic evaluation, budget impact analysis, and pricing and reimbursement decisions from the JCA scope. These remain entirely national. A JCA report that concludes a biosimilar is clinically non-inferior to its reference biologic does not compel France’s CEPS to grant a particular price, does not require Germany’s G-BA to issue a specific AMNOG rating, and does not bind Italy’s AIFA to any particular negotiating outcome. The clinical finding flows into each national process as one input among several.

This structural limitation has a counterintuitive practical consequence for generic and biosimilar companies. By standardizing the clinical evidence base that flows into every national HTA process, the HTAR effectively removes clinical differentiation as a meaningful competitive variable across markets. Every national payer starts from the same clinical assessment. The differentiation that drives market access outcomes is therefore entirely in the economic dossier: the local budget impact model, the cost-effectiveness analysis calibrated to national healthcare cost thresholds, and the stakeholder engagement strategy. The quality and precision of country-specific health economic evidence becomes more important under the HTAR, not less.

Implications for Biosimilar Manufacturers

For biosimilar manufacturers, the HTAR’s treatment of biosimilar evidence is particularly important. The JCA framework will need to address how biosimilar comparability packages, which demonstrate analytical and clinical similarity to the reference biologic rather than superiority or added clinical benefit, fit into a framework designed around comparative effectiveness assessment. There is ongoing technical work within the HTA Coordination Group on methodology for biosimilar assessments, and the outcome of that work will significantly influence how national payers approach biosimilar formulary decisions after 2025.

Companies developing biosimilars should participate in HTA Coordination Group stakeholder consultations and ensure that their clinical development programs generate data that is compatible with both the EMA’s regulatory data requirements and the emerging JCA methodological framework. In some cases, generating comparator data against a locally-relevant standard of care (which may differ from the molecule used in pivotal biosimilar comparability trials) will be required to support national HTA submissions, even if the JCA does not specifically require it.

Key Takeaways: HTA Reform

The HTAR harmonizes only the clinical layer of HTA, leaving economic evaluation and P&R decisions national. The practical effect for companies is that health economic capabilities at the country level become more, not less, important. Biosimilar manufacturers face an evolving JCA methodology that is not yet fully defined. Standard generics are outside the mandatory JCA scope, but the culture of evidence-based value demonstration that HTA embeds across European payers will affect how all pharmaceutical products, including complex generics and VAMs, are discussed in pricing negotiations.

Section 8: Complex Generics and Biosimilars: Technology Roadmaps and Market Access Mechanics

The Complex Generic Development Roadmap

Complex generics are products where demonstrating bioequivalence to the reference product requires substantially more than standard pharmacokinetic studies in healthy volunteers. Complexity can arise from four primary sources: a complex active ingredient (e.g., a mixture of active stereoisomers, a complex polymeric drug), a complex formulation (e.g., a liposomal product, a drug-device combination), a complex route of administration (e.g., oral inhalation, transdermal delivery, intrathecal injection), or a complex drug-device combination (e.g., an auto-injector, a metered-dose inhaler).

Stage 1: Pre-IND/Pre-IMPD Reference Product Characterization. Before development begins, the complex generic developer must comprehensively characterize the reference product’s physicochemical properties, impurity profile, excipient composition, device performance characteristics (where relevant), and pharmacokinetic profile across the approved dose range. This characterization work takes 12 to 24 months and costs EUR 1 to 5 million depending on analytical complexity. It is the foundation for all subsequent development decisions.

Stage 2: Formulation and Process Development. The developer must match the reference product’s key quality attributes (KQAs) and critical quality attributes (CQAs) as closely as possible, without necessarily replicating the exact manufacturing process (which may be trade secret-protected or patent-protected). For inhaled products, this involves matching aerodynamic particle size distribution, fine particle fraction, and device performance metrics. For liposomal products, it involves matching particle size distribution, encapsulation efficiency, lipid composition, and drug release kinetics. For complex injectables, it includes endotoxin levels, osmolality, pH, and in some cases sterility testing under aseptic conditions.

Stage 3: Bioequivalence Study Design. The EMA’s guidelines for specific complex product categories set out the bioequivalence study requirements. For most locally-acting products (inhaled drugs, topicals, gastrointestinal products), standard pharmacokinetic bioequivalence is insufficient because the systemic exposure does not fully predict the local therapeutic effect. Pharmacodynamic endpoints or in-vitro-in-vivo correlation (IVIVC) approaches may be required. The EMA has published product-specific guidance for a growing number of complex generics through its Product-specific bioequivalence guidance database, which should be the first reference point for any complex generic developer.

Stage 4: EMA/MHRA Regulatory Engagement. EMA’s Scientific Advice and the Parallel Scientific Advice (PSA) process for complex generics are strongly recommended before initiating pivotal bioequivalence studies. PSA allows for joint scientific advice from both the EMA and a national HTA body, addressing the data requirements from both a regulatory and a market access perspective simultaneously. For products where the development pathway is genuinely uncertain, a PSA can save 12 to 18 months of regulatory back-and-forth after submission.

Stage 5: Post-Approval Device Validation (for Drug-Device Combinations). Complex generics that incorporate a delivery device require device validation studies under the EU Medical Device Regulation (MDR, 2017/745) or under the combination product guidance. For auto-injectors, metered-dose inhalers, and prefilled syringes, this involves usability studies, human factors testing, and device performance equivalence to the reference combination product. Device patents are a separate IP risk layer that must be assessed in parallel with drug compound FTO.

The Biosimilar Development and Market Access Roadmap

Stage 1: Analytical Similarity (24-36 Months). Biosimilar development begins with an extensive analytical characterization of the reference biologic. This involves state-of-the-art techniques including high-resolution mass spectrometry, nuclear magnetic resonance spectroscopy, X-ray crystallography, size-exclusion chromatography coupled to multi-angle light scattering (SEC-MALS), and cell-based functional assays. The goal is to establish that the biosimilar candidate matches the reference product’s primary structure, higher-order structure, post-translational modifications (particularly glycosylation for glycoproteins), and functional activity within narrow tolerances. This analytical package is submitted as part of the comparability exercise in the regulatory dossier.

Stage 2: Process Development and Manufacturing Scale-Up (12-24 Months). The cell line, upstream bioprocess conditions (media, feed strategy, pH, temperature, dissolved oxygen), and downstream purification process must be developed to produce a molecule that matches the reference product’s quality profile consistently at commercial scale. Process development is often the most expensive phase of biosimilar development, with costs ranging from EUR 20 to 80 million for a monoclonal antibody depending on production scale and process complexity.

Stage 3: Nonclinical and Clinical Comparability (12-24 Months). The EMA’s scientific guidelines require a stepwise comparability package. Nonclinical studies (in vitro and in vivo) confirm that the biosimilar and reference product have equivalent pharmacodynamic and toxicological profiles. Clinical pharmacokinetic and pharmacodynamic studies in healthy volunteers or relevant patient populations confirm biosimilarity in humans. For most monoclonal antibodies, one or two comparative PK/PD studies plus a randomized comparative efficacy trial in a sensitive indication are sufficient to support EMA approval. The concept of extrapolation allows the biosimilar to be approved for all of the reference product’s EU-approved indications based on this limited clinical program, provided the mechanism of action and target receptor are the same across indications.

Stage 4: Regulatory Submission and CHMP Review (12-18 Months). The biosimilar MAA is submitted to the EMA via the Centralised Procedure (mandatory for biologics). The CHMP conducts a full scientific assessment, including an assessment of the comparability data, the manufacturing process validation, and the proposed labeling. A typical CHMP review takes 12 months of active assessment time, with clock stops for applicant responses. EMA approval grants authorization across all EU Member States.

Stage 5: National Interchangeability and Substitution Policy Engagement. EMA approval as a biosimilar does not automatically entitle a pharmacist to substitute a biosimilar for a prescribed reference biologic. Substitution policy is national. Most EU Member States have adopted either an automatic substitution approach (where biosimilars are treated like generics and can be dispensed without specific physician authorization) or a physician-led substitution approach (where the prescribing physician must specifically approve the switch). France, the UK, and several Nordic countries allow automatic substitution in some circumstances. Germany does not permit automatic substitution at the pharmacy level for biosimilars; substitution requires physician consent. Italy’s position has evolved toward supporting substitution under national guidelines published by AIFA, but implementation is uneven at the hospital level.

Stage 6: Market Access Execution. Biosimilar market access in Europe requires a multi-track strategy. The pricing and reimbursement track involves negotiating with national payers to secure listing at a discount that is competitive versus other biosimilars in the market while preserving margin. For second or third entrant biosimilars in an already-competitive category (e.g., adalimumab, trastuzumab, bevacizumab), the pricing dynamics approach commodity levels in markets like Germany. The medical affairs track involves engaging prescribers, pharmacy directors, and hospital formulary committees with the clinical evidence base supporting the biosimilar, addressing concerns about extrapolation and long-term safety, and building institutional trust through published real-world evidence.

The Biosimilar Market: Where Europe Leads and Where It Lags

Europe has approved more biosimilars than any other regulatory jurisdiction. The EMA has granted over 90 biosimilar MAs since the framework launched in 2006. European biosimilars have generated an estimated EUR 56 billion in cumulative savings to healthcare systems and delivered approximately 7 billion patient-treatment days that would not have been possible at originator prices.

This leadership masks important fragmentation. The disparity in biosimilar uptake between markets is as large as the disparity in small-molecule generic penetration. Nordic countries, Germany (for hospital biosimilars at least), and the UK have achieved biosimilar penetration rates above 70% for established categories like anti-TNF biologics. France and Southern European markets have been slower, with physician loyalty to established brands, uncertainty about extrapolation, and inadequate substitution incentives contributing to the lag.