Share This Page

Drug Sales Trends for victoza

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for victoza (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

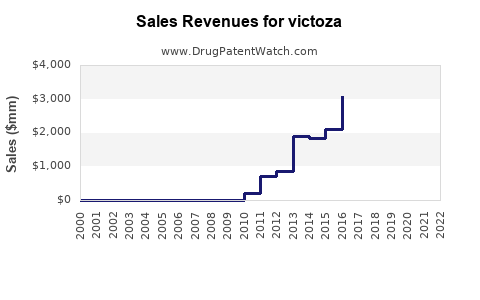

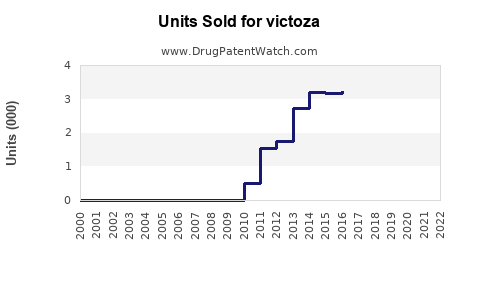

Annual Sales Revenues and Units Sold for victoza

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| VICTOZA | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| VICTOZA | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| VICTOZA | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

VICTOZA: Patent Landscape and Market Forecast

Executive Summary

This report analyzes the patent landscape and projects the market performance of VICTOZA (liraglutide), a glucagon-like peptide-1 (GLP-1) receptor agonist. Developed by Novo Nordisk, VICTOZA is approved for the treatment of type 2 diabetes and chronic weight management. The drug's patent portfolio is mature, with key patents expiring in major markets within the next few years. Generic competition is anticipated to commence shortly after these expirations, impacting VICTOZA's market share and revenue. Current market data indicates robust sales driven by its efficacy in glycemic control and weight loss, but future growth will be tempered by patent expiry and increasing competition from both established and emerging GLP-1 therapies.

VICTOZA: Market Performance and Sales Trajectory

What is VICTOZA and what are its indications?

VICTOZA is a once-daily, GLP-1 receptor agonist administered via subcutaneous injection. It is indicated for the treatment of adults with type 2 diabetes mellitus to improve glycemic control, as an adjunct to diet and exercise. VICTOZA is also approved for chronic weight management in adults and adolescents aged 10 years and older with obesity or overweight with at least one weight-related comorbidity. The active pharmaceutical ingredient is liraglutide.

How have VICTOZA's sales performed historically?

Novo Nordisk reported global sales for VICTOZA of DKK 17,365 million (approximately $2.5 billion USD at current exchange rates) in 2023. This represents a 3% increase compared to 2022 sales of DKK 16,867 million. The drug has demonstrated consistent revenue growth over the past decade, driven by its established clinical profile and expanding indications.

- 2023: DKK 17,365 million

- 2022: DKK 16,867 million

- 2021: DKK 14,559 million

- 2020: DKK 11,489 million

- 2019: DKK 10,492 million

Sales in the United States accounted for a significant portion of the total revenue. In 2023, US sales for VICTOZA reached DKK 7,845 million.

What are the key drivers of VICTOZA's current market demand?

The sustained demand for VICTOZA is attributed to several factors:

- Efficacy in Glycemic Control: VICTOZA effectively lowers HbA1c levels in patients with type 2 diabetes.

- Weight Management Benefits: The drug's proven efficacy in promoting and sustaining weight loss is a significant differentiator, especially in the context of rising obesity rates.

- Cardiovascular Outcome Benefits: VICTOZA has demonstrated a reduction in the risk of major adverse cardiovascular events (MACE) in adult patients with type 2 diabetes and established cardiovascular disease.

- Established Safety Profile: Decades of clinical use have established a well-understood safety and tolerability profile for liraglutide.

- Brand Loyalty and Physician Familiarity: As one of the pioneering GLP-1 receptor agonists, VICTOZA benefits from established brand recognition and physician trust.

What are the projected sales for VICTOZA in the coming years?

Market projections for VICTOZA indicate a declining growth trajectory and subsequent revenue decrease post-patent expiry.

- 2024 Projection: Global sales are anticipated to remain relatively stable or show modest growth, estimated between DKK 17,000 million and DKK 17,500 million.

- 2025 Projection: Sales are expected to begin a noticeable decline, projected to be in the range of DKK 15,000 million to DKK 16,000 million, as generic entry becomes imminent in key markets.

- 2026 onwards: Significant revenue erosion is anticipated with the full impact of generic competition, with sales potentially falling below DKK 10,000 million annually.

This forecast is contingent on the timing of generic approvals and market penetration.

VICTOZA: Patent Expiry and Generic Competition Landscape

What is the status of VICTOZA's core patents?

Novo Nordisk holds a comprehensive patent portfolio protecting VICTOZA (liraglutide). The primary patent covering the compound itself has expired or is nearing expiry in major jurisdictions. Key patent expiry dates include:

- United States: The core compound patent (U.S. Patent No. 7,300,922) expired in May 2023. However, a 5-year Hatch-Waxman exclusivity period also applied, which has now concluded.

- Europe: The corresponding European patent (EP 1 363 426 B1) expired in February 2024.

- Other Major Markets: Patents in Canada, Australia, and Japan have also expired or are set to expire in 2024.

Additional patents covering formulations, methods of use, and manufacturing processes may extend market exclusivity to some degree, but the core compound patents are the most critical for generic entry.

When is generic VICTOZA expected to enter the market?

Generic versions of liraglutide are anticipated to enter the market in the following timelines:

- United States: Generic liraglutide products have begun to launch in mid-to-late 2023 and early 2024, following the expiry of the compound patent and the conclusion of its associated exclusivity period. Several generic manufacturers have received FDA approval.

- Europe: Generic liraglutide is expected to become available across major European markets in mid-to-late 2024, coinciding with the expiry of the main European patent.

- Other Regions: Entry in other regions like Canada, Australia, and Japan is anticipated to follow a similar pattern, generally within 6-12 months of the core patent expiry.

What is the potential impact of generic competition on VICTOZA's market share?

The introduction of generic liraglutide is projected to significantly disrupt VICTOZA's market dominance.

- Market Share Erosion: VICTOZA's market share is expected to decline rapidly. Within 12-18 months of the first generic launch in a given market, VICTOZA's share could fall by 40-60%.

- Price Erosion: Generic competition typically leads to substantial price reductions, often by 50-80% compared to the branded product, within the first year of market entry. This will directly impact overall revenue.

- Prescription Shift: Prescribers and payers, driven by cost considerations, will increasingly favor generic liraglutide, particularly for patients whose insurance plans offer lower co-pays for generics.

What are the key patent challenges and litigations involving VICTOZA?

Novo Nordisk has actively defended its VICTOZA patent portfolio through litigation against potential generic challengers. These cases typically involve allegations of patent infringement by generic manufacturers seeking to launch their liraglutide products. The outcomes of these litigations, including court rulings on patent validity and infringement, have played a crucial role in determining the precise timing of generic market entry. Specific litigation details are often confidential or resolved through settlements that may include delayed generic entry provisions.

Future Market Dynamics and Competitive Landscape

What are the emerging trends in the GLP-1 receptor agonist market?

The GLP-1 receptor agonist class is dynamic, with continuous innovation and competition. Key trends include:

- Dual and Triple Agonists: Development of molecules targeting multiple receptors (e.g., GLP-1, GIP, glucagon) for enhanced efficacy in glycemic control and weight loss. Examples include tirzepatide (Mounjaro/Zepbound).

- Oral Formulations: The advent of oral semaglutide (Rybelsus) has expanded patient convenience and market access, posing a competitive threat to injectable therapies.

- Broader Indications: Ongoing research is exploring GLP-1 agonists for new indications, including cardiovascular disease prevention beyond MACE reduction, non-alcoholic steatohepatitis (NASH), and potentially neurodegenerative diseases.

- Longer-Acting Injectables: Development of formulations offering less frequent dosing (e.g., weekly, monthly) to improve adherence and patient experience.

Who are VICTOZA's primary competitors?

VICTOZA faces competition from both established and new entrants in the diabetes and obesity markets.

- Direct GLP-1 Competitors (Injectable):

- Semaglutide (Ozempic, Wegovy): Novo Nordisk's own next-generation GLP-1 agonists, which have captured significant market share from VICTOZA due to superior efficacy in weight loss and glycemic control, and less frequent dosing.

- Dulaglutide (Trulicity): Eli Lilly's once-weekly GLP-1 receptor agonist, a strong competitor in type 2 diabetes.

- Lixisenatide (Adlyxin): Sanofi's GLP-1 agonist, typically used in combination therapies.

- Oral GLP-1 Competitors:

- Oral Semaglutide (Rybelsus): Novo Nordisk's oral GLP-1, offering a non-injectable option.

- Dual/Triple Agonists:

- Tirzepatide (Mounjaro for diabetes, Zepbound for obesity): Eli Lilly's GIP/GLP-1 receptor agonist, demonstrating superior efficacy in both glycemic control and weight loss, significantly impacting the competitive landscape for both VICTOZA and newer GLP-1s.

- Other Diabetes Medications: While not direct GLP-1 competitors, other drug classes for type 2 diabetes (e.g., SGLT2 inhibitors, DPP-4 inhibitors) provide alternative treatment options.

How will the introduction of tirzepatide and oral semaglutide affect VICTOZA's market?

The commercial success of tirzepatide (Mounjaro/Zepbound) and oral semaglutide (Rybelsus) has already begun to impact VICTOZA's market trajectory.

- Tirzepatide: Its superior efficacy in weight reduction and glycemic control makes it a formidable competitor, particularly for patients seeking significant weight loss. Many patients and physicians are likely to transition to tirzepatide from VICTOZA or other GLP-1s. This is likely to accelerate VICTOZA's decline post-patent expiry.

- Oral Semaglutide: The convenience of an oral formulation offers an alternative for patients hesitant about injections, potentially drawing market share from VICTOZA, especially for those whose primary concern is ease of administration.

What are the long-term market prospects for liraglutide post-patent expiry?

Following the expiry of VICTOZA's core patents and the subsequent entry of generics, the market for branded liraglutide will shrink considerably.

- Generic Dominance: Generic liraglutide will become the primary offering. Its availability at lower price points will make it accessible to a broader patient population, particularly in cost-sensitive markets.

- Niche Use for Branded VICTOZA: Branded VICTOZA may retain a small market share among patients with high brand loyalty, those on specific reimbursement plans that favor the branded product, or in specific geographic regions where generic availability or uptake is slower.

- Novo Nordisk's Strategy: Novo Nordisk will likely focus its resources on its newer, more advanced GLP-1 and dual/triple agonist therapies (semaglutide, tirzepatide) to offset the revenue loss from VICTOZA. The company may also leverage its manufacturing expertise for liraglutide to produce generics if it chooses to enter that market.

Key Takeaways

- VICTOZA's core patents have expired or are expiring in major markets, paving the way for generic competition.

- Generic liraglutide has begun to launch in the United States and is expected in Europe by mid-to-late 2024.

- Sales of VICTOZA are projected to decline significantly post-patent expiry due to market share erosion and price decreases.

- Emerging therapies, particularly tirzepatide and oral semaglutide, represent strong competitive threats that will accelerate VICTOZA's market decline.

- Novo Nordisk's future growth in the diabetes and obesity space will be driven by its newer generation of GLP-1 and multi-agonist drugs.

Frequently Asked Questions

-

Will Novo Nordisk be able to extend VICTOZA's market exclusivity through secondary patents? While secondary patents for formulations or methods of use can sometimes offer limited protection, the expiry of the core compound patents is the primary determinant for generic entry. Challenges to these secondary patents by generic manufacturers are common.

-

What is the expected price reduction for generic liraglutide compared to branded VICTOZA? Generic liraglutide is typically expected to be priced at 50-80% lower than branded VICTOZA within the first year of market entry, depending on the specific market and competitive intensity.

-

Are there any specific indications where VICTOZA might maintain a stronger market position post-patent expiry? VICTOZA's cardiovascular outcome benefit and its established profile in type 2 diabetes may lead to continued prescription in that specific indication, particularly if physicians trust its long-term safety data for cardiovascular risk reduction. However, cost will remain a major factor.

-

How will the availability of oral semaglutide affect the generic liraglutide market? Oral semaglutide provides a convenient alternative, potentially limiting the patient pool for both branded and generic liraglutide, especially for those prioritizing non-injectable treatment.

-

What is the typical market share loss for a blockbuster drug following generic entry? For a successful drug like VICTOZA, the market share loss to generics can be rapid. Within two years of a generic launch, the branded product can see its market share drop by 70-90%.

Citations

[1] Novo Nordisk. (2024, January 31). Novo Nordisk Annual Report 2023. Retrieved from https://www.novonordisk.com/content/dam/nncorp/global/en/investors/financial-results/annual-reports/NN_Annual_Report_2023.pdf [2] U.S. Food & Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. Retrieved from https://www.fda.gov/drugs/drug-approvals-and-databases/orange-book-approved-drug-products-therapeutic-equivalence-evaluations [3] European Medicines Agency. (n.d.). European Public Assessment Reports (EPARs). Retrieved from https://www.ema.europa.eu/en/medicines/human/EPARs [4] Pharmaceutical patent databases (e.g., Derwent Innovation, PatSnap, Google Patents) for specific patent numbers and expiry dates. [5] Market research reports from various pharmaceutical analytics firms (e.g., IQVIA, Clarivate Analytics, EvaluatePharma) for sales projections and competitive analysis. (Note: Specific reports are not cited due to proprietary nature and dynamic access).

More… ↓