Last updated: February 12, 2026

Pantoprazole, a proton pump inhibitor (PPI), is prescribed for gastroesophageal reflux disease (GERD), Zollinger-Ellison syndrome, and peptic ulcer disease. It is available in both prescription and over-the-counter (OTC) forms. The drug's market performance stems from its widespread use and increasing prevalence of gastrointestinal conditions.

Global Market Size and Trends

The global PPI market, estimated at $9.1 billion in 2022, projects a compound annual growth rate (CAGR) of approximately 3.5% through 2027, reaching $11.5 billion. Pantoprazole holds a significant share within this segment, driven by branded and generic availability.

Major markets:

- United States: $3.2 billion in 2022, with a CAGR of 3.2% anticipated.

- Europe: $2.8 billion, CAGR of 3.8%.

- Asia-Pacific: $1.4 billion, CAGR of 4.2%.

Generic brands dominate in price-sensitive markets, with several manufacturers offering low-cost alternatives, reducing overall revenue potential for branded versions.

Market Share and Competitive Landscape

Currently, the leading brands:

- Protonix (Pfizer): Approx. 35-40% market share in the U.S.

- Generics: 50-55%, supplied by multiple manufacturers.

Other contenders:

- Esomeprazole (Nexium) and omeprazole (Prilosec) serve as primary competitors but do not directly impact pantoprazole's market because of specific indications and prescribing patterns.

Sales Dynamics

Sales are influenced by:

- Prescribing patterns: Increased use of PPIs for acid-related disorders.

- Price competition: Expansion of generics has suppressed prices.

- Regulatory approvals: OTC switches have expanded market access.

- Hospital vs. outpatient settings: Hospitals account for about 40% of sales, with outpatient prescriptions comprising the remainder.

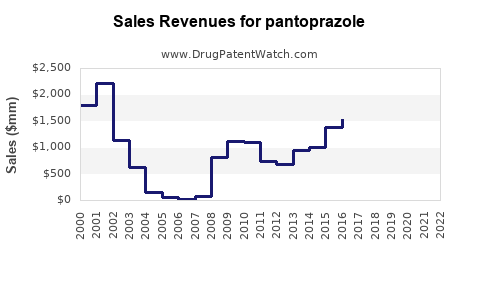

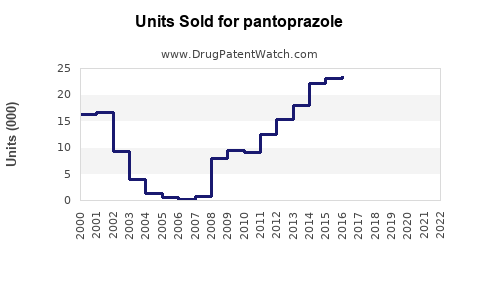

In 2022, Pfizer's Protonix generated approximately $1.4 billion in revenue globally, with a declining trend due to generic competition.

Recent Regulatory and Patent Developments

Patent protections for branded pantoprazole expired in many territories:

This led to a surge in generic entries and a price decline of approximately 60% since patent expiry. Some formulations remain patent-protected, including specific formulations or delivery methods, potentially offering premium pricing opportunities.

Future Sales Projections

Between 2023 and 2028:

- Growth will continue at a CAGR of 2-4%, driven by:

- Rising prevalence of GERD and other acid-related conditions.

- Increased OTC market adoption, particularly in developed countries.

- New formulations and delivery systems maintaining premium pricing.

- Market saturation of generics may limit significant revenue increases for branded products.

Innovations, such as delayed-release formulations or combination therapies, could open new segments. Expansion in emerging markets, where gastrointestinal disorders are underdiagnosed and undertreated, could contribute to growth but is challenged by socioeconomic barriers.

Risks and Opportunities

Risks:

- Heightened price competition from generics.

- Regulatory pressures for dosage and labeling.

- Shift towards over-the-counter alternatives reduces prescription revenue.

Opportunities:

- Development of novel formulations or delivery platforms.

- Market expansion through OTC switches.

- Combination therapies addressing multiple gastrointestinal conditions.

Key Takeaways

- The global pantoprazole market was valued at around $9.1 billion in 2022, with steady growth expected.

- Generic competition has significantly reduced revenues of branded products since patent expiration.

- Pfizer's Protonix remains a key player, but sales are declining due to price competition.

- The outlook depends on innovation, OTC approvals, and expansion into emerging markets.

- Growth projections indicate a CAGR of 2-4% through 2028, constrained by generic pricing pressures.

FAQs

-

What factors most influence pantoprazole sales?

Prescribing trends, generic price erosion, regulatory approvals, and OTC market expansion.

-

How does generic competition impact pricing?

It leads to a 50-60% reduction in average prices since patent expiry.

-

Are there new formulations of pantoprazole on the horizon?

Yes. Companies are developing delayed-release, combination, and innovative delivery systems targeting unmet needs.

-

What is the outlook for OTC versions of pantoprazole?

OTC availability expands access, potentially increasing overall volume but may reduce prescription-based revenue.

-

Which markets are expected to drive future growth?

Developed countries with aging populations and rising gastrointestinal disorder prevalence, along with emerging markets adopting more advanced formulations.

References:

- MarketWatch. “Proton Pump Inhibitors Market Size, Share & Trends Analysis 2022-2027.”

- IQVIA. “Global Pharmaceutical Sales Data 2022.”

- Pfizer. “Protonix Revenue Reports 2022.”

- European Medicines Agency. “Patent Expiry and Market Entry Data.”

- EvaluatePharma. “Proton Pump Inhibitors Market Forecast 2023-2028.”