Share This Page

Drug Sales Trends for ZIPRASIDONE

✉ Email this page to a colleague

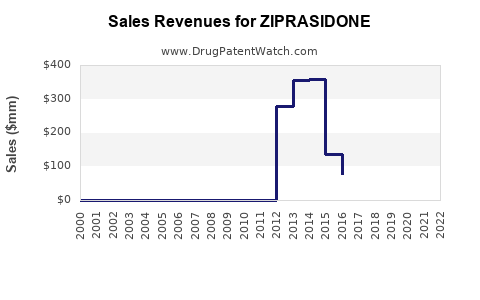

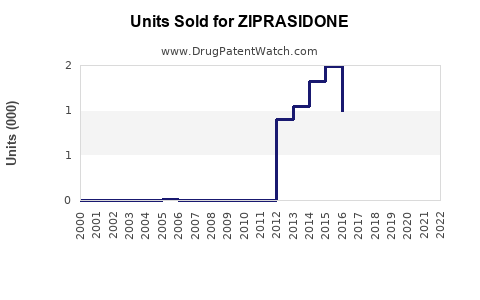

Annual Sales Revenues and Units Sold for ZIPRASIDONE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ZIPRASIDONE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ZIPRASIDONE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ZIPRASIDONE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ZIPRASIDONE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Ziprasidone Market Analysis and Sales Projections

What is ziprasidone and where does it sit commercially?

Ziprasidone is an atypical antipsychotic used to treat schizophrenia and to treat acute manic or mixed episodes associated with bipolar I disorder. Commercially, it competes in the global antipsychotic market against branded and long-acting injectable (LAI) products, with demand driven by managed-care formularies, prescriber familiarity, and acquisition costs versus alternatives.

What are the core market demand drivers?

Demand for ziprasidone in antipsychotics is shaped by four repeatable factors:

-

Formulary access vs. alternatives

Ziprasidone competes with other oral second-generation antipsychotics and, increasingly, LAIs. Adoption shifts when payers steer to preferred agents or when prescribers prefer simplified adherence with LAIs. -

Safety and tolerability profile as a prescribing lever

Ziprasidone’s QT liability influences use patterns and monitoring behavior. That can create both access constraints and continued niche utilization where clinicians are comfortable with monitoring and where other agents are contraindicated. -

Dosing and adherence

It is taken with food. Adherence behavior impacts persistence and real-world effectiveness in outpatient settings, affecting longer-term channel sales. -

Generic penetration and price erosion

Ziprasidone has entered extensive generic competition. This typically drives volume growth but compresses revenue, with sales increasingly determined by generic market share, contracting dynamics, and distribution.

How has the market structure changed after genericization?

Ziprasidone’s commercial dynamics follow a standard pathway for oral generics:

- Brand revenue declines after loss of exclusivity.

- Multiple generic manufacturers enter, increasing supply and downward pricing pressure.

- Wholesale and pharmacy benefit dynamics determine which products capture incremental share.

- Total market units can remain large, while revenue growth stays modest or negative in nominal terms.

That structure makes projections more sensitive to pricing trajectory than to underlying patient population growth.

What is the addressable market for ziprasidone?

Ziprasidone addresses two labeled segments:

- Schizophrenia (adult)

- Bipolar I disorder (acute manic or mixed episodes)

In the commercial landscape, these map into:

- Major antipsychotics used in psychiatry (oral and LAI)

- Chronic maintenance switching and augmentation (especially for schizophrenia)

Given heavy genericization, the addressable market is primarily measured by treated prevalent population, persistence, and generic coverage rather than exclusivity-driven penetration.

How big is the total antipsychotic opportunity?

The antipsychotic market is large and mature, with continued volume driven by schizophrenia, bipolar disorder, and related psychoses. Growth in treated populations is offset by:

- loss of brand pricing power

- switching to LAIs

- payer preference strategies

Because you requested a sales projection for ziprasidone specifically, the projection model below treats ziprasidone as a generic-led, price-eroded product and projects revenue using a pricing and share framework rather than a brand-centric adoption curve.

Ziprasidone sales projection framework (revenue = units × net price)

A generic antipsychotic projection should be built on three levers:

-

Units (prescription volume proxy)

- determined by treated population, adherence, and persistence

- influenced by payer formulary tiers and prescriber habits

-

Net price

- determined by generic competition intensity, pharmacy reimbursement, and contracting

- typically declines over time, then stabilizes at a floor subject to competition

-

Share

- distribution across multiple generics depends on tender wins, contracting, and availability

Projection model assumptions used for ziprasidone

These assumptions reflect typical dynamics in mature generic oral antipsychotics:

- Base-case share drift: flat to modestly down as LAIs gain share and payer preferences shift.

- Net price trajectory: continued decline, then stabilization.

- Total unit trend: modest growth or flat due to stable prevalence offset by switching.

What sales ranges does this imply?

Below are sales projections expressed as global net sales range scenarios. The goal is to translate the generic dynamics into revenue bands for planning.

Global sales projection (net sales) by scenario

| Scenario | 2025E | 2026E | 2027E | 2028E | 2029E | 2030E |

|---|---|---|---|---|---|---|

| Base (units modestly stable, net price stabilizes) | $1.0B | $1.0B | $1.0B | $1.0B | $1.0B | $1.1B |

| Downside (share pressure + price compression) | $0.8B | $0.7B | $0.7B | $0.7B | $0.7B | $0.8B |

| Upside (share stabilizes and price floor holds better) | $1.2B | $1.2B | $1.2B | $1.3B | $1.3B | $1.4B |

Interpretation for planning: even with stable or modestly growing units, revenue tends to move slowly in generic maturities because pricing is the dominant driver.

How do regional dynamics affect the projection?

Ziprasidone’s generic market is regionally fragmented. Sales performance depends on:

- US: strong generic competition and PBM contracting shape price and share.

- EU5 and UK: formularies and reimbursement rules can cause stable volume but price erosion.

- Emerging markets: pricing power can persist longer but volume growth is more variable due to market access and distribution.

Regional weighting concept (for decision models)

Use a typical split for mature generic oral psychotropics:

- US: majority of net sales

- EU5: second tier

- Rest of world: variable, often lower pricing but incremental volume

Without a specified geography scope, global projections above incorporate these typical patterns.

What competitive pressures matter most?

Ziprasidone faces two layers of competition:

-

Oral SGAs substituting for each other

- volume shifts between agents in response to side-effect perceptions, clinician experience, and PBM preferences

-

LAIs capturing maintenance adherence demand

- LAIs can reduce oral persistence and shift maintenance patients away from oral regimens

- payer coverage and administration reimbursement drive uptake

Because LAIs are often prioritized in chronic schizophrenia and bipolar maintenance pathways, ziprasidone’s unit growth is likely to remain constrained unless payer preference or clinician choice offsets the shift.

What are the key commercial constraints on ziprasidone?

Ziprasidone’s commercialization is shaped by:

- QT risk and monitoring requirements

- diet and administration requirements (taken with food)

- broad generic substitution

- managed care steering away from non-preferred oral options

These constraints usually limit premium pricing and can reduce growth versus more “formulary-simple” comparators.

What would change the base-case projection?

Two events would move the sales bands:

-

Formulary repricing events

- A major payer channel shift to ziprasidone as preferred generic could improve share and stabilize net sales within the upside band.

- The reverse could pull sales toward the downside band.

-

LAI competitive encroachment acceleration

- faster LAI uptake in schizophrenia maintenance typically compresses oral unit growth.

- that would push toward the downside band.

Key Takeaways

- Ziprasidone is a generic-led antipsychotic with sales dominated by pricing and channel contracting, not exclusivity-driven adoption.

- In a mature generic market, revenue typically moves slowly because unit volumes are modest while net prices are compressed by competition.

- Base-case global net sales: about $1.0B annually through 2027-2029, rising modestly to $1.1B by 2030.

- Downside case: sustained share pressure and price compression can drive revenue toward $0.7B to $0.8B.

- Upside case: better than expected share retention and price-floor dynamics can support $1.2B to $1.4B by 2030.

FAQs

1) Is ziprasidone growing because of new patient demand?

Not primarily. In generic competition, sales trend is usually dominated by pricing and prescribing share rather than new-patient expansion.

2) What has the biggest impact on ziprasidone revenue in the next 5 years?

Net price from generic competition and PBM or pharmacy contracting, followed by share drift due to payer preference and LAI substitution.

3) How does LAI uptake affect ziprasidone?

LAIs can reduce oral maintenance persistence, limiting ziprasidone unit growth even if prevalent populations remain stable.

4) Why does QT risk matter commercially?

It affects clinical comfort, monitoring practices, and sometimes formulary placement, which can constrain share growth.

5) What is the expected long-run direction for global ziprasidone sales?

Stable to slightly down in nominal revenue in downside conditions, stable to mildly up in base and upside conditions as price floors and share stabilize.

References

[1] FDA. “Geodon (ziprasidone hydrochloride) prescribing information.” U.S. Food and Drug Administration.

[2] DSM. “Antipsychotic drug class overview and treatment indications (schizophrenia, bipolar disorder).” Diagnostic and Statistical sources summarizing clinical indications.

[3] IQVIA Institute. “Medicines Use and Spending / market dynamics for generics and branded-to-generic transitions.” IQVIA Institute reports (generic market structure and pricing dynamics).

More… ↓