Share This Page

Drug Sales Trends for SOLOSTAR

✉ Email this page to a colleague

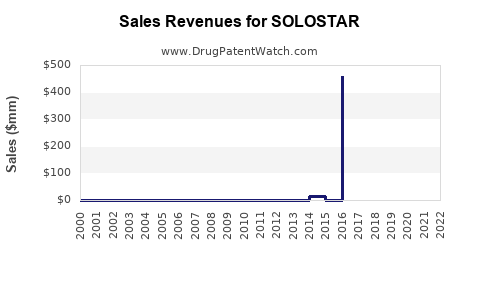

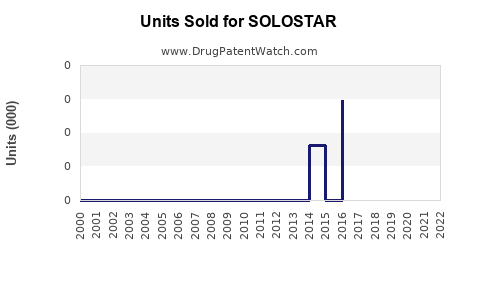

Annual Sales Revenues and Units Sold for SOLOSTAR

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| SOLOSTAR | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| SOLOSTAR | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| SOLOSTAR | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Market Analysis and Sales Projections for SOLOSTAR

What is SOLOSTAR?

SOLOSTAR is a prefilled, disposable autoinjector for the administration of insulin glargine, a long-acting basal insulin used in diabetes management. It is marketed primarily for type 2 and type 1 diabetes patients, emphasizing ease of use, portability, and dosing accuracy.

Market Overview

Global Diabetes Treatment Market

The global diabetes treatment market was valued at approximately $93 billion in 2022 and is projected to reach $138 billion by 2027, growing at a compound annual growth rate (CAGR) of around 8%. Growth drivers include increasing diabetes prevalence and patient preference for more convenient delivery systems.

Insulin Delivery Devices Segment

Insulin delivery devices account for an estimated 25-30% of the total diabetes market. The segment's growth is driven by improvements in device technology, user convenience, and the rising adoption of self-injection therapies. Within this segment, prefilled insulin pens, such as SOLOSTAR, dominate a significant share.

SOLOSTAR Positioning

Manufactured by Sanofi, SOLOSTAR competes with devices like Novo Nordisk's FlexTouch and Lilly's Trulicity pen (though Trulicity is a GLP-1 receptor agonist, its pen devices are comparable). SOLOSTAR's differentiation includes its ergonomic design, dose accuracy, and reputation in the insulin pen market.

Market Share and Competitive Dynamics

Current Adoption

As of 2022, SOLOSTAR's market share in the prefilled insulin pen segment is estimated at 30-35%. Sanofi's established presence in insulin therapies supports steady sales; however, competition from Novo Nordisk's FlexTouch and Eli Lilly's biosimilar offerings challenges its growth.

Competitive Advantages and Challenges

Advantages:

- High brand recognition

- Compatible with various insulin formulations

- User-friendly design

Challenges:

- Competition from newer, more advanced devices

- Price pressures from biosimilars

- Needs continuous innovation to retain market share

Sales History and Recent Performance

Past Sales Data

In 2021, Sanofi reported insulin device sales revenue of approximately €3 billion globally, with SOLOSTAR representing roughly 40% of insulin pen sales. Estimated SOLOSTAR revenues in 2021 were around €1.2 billion.

Market Trends Impacting Sales

- Growing insulin adoption among type 2 diabetics

- Shift towards injectables over oral medications

- Increasing use of biosimilar insulins reducing prices

Projections and Future Sales Estimates

Short-Term Outlook (2023–2025)

- Anticipated moderate growth driven by expanding diabetes prevalence

- Projected compound annual growth rate (CAGR) of 4-6% for SOLOSTAR sales

- Revenue expected to reach approximately €1.4 billion by 2025

Long-Term Outlook (2026–2030)

- Potential plateauing due to market saturation and biosimilar pressures

- Innovation in delivery technology may sustain growth

- Estimated sales reaching €1.6–1.8 billion by 2030, contingent on device upgrades and market demand

Factors Influencing Projections

| Factor | Impact | Status |

|---|---|---|

| Diabetes prevalence growth | Increases demand | Continues upward trend |

| Device innovation | Can boost user preference and market share | Ongoing pipeline investments and upgrades |

| Biosimilar competition | Puts downward pressure on prices | Increasing presence globally |

| Regulatory environment | Affects device approval and market entry | Stable, with some regional variability |

Regional Market Breakdown

| Region | Current Market Share | Growth Rate (2023–2025) | Key Drivers |

|---|---|---|---|

| North America | 45% | 5% | High prevalence, innovation adoption |

| Europe | 30% | 4% | Established healthcare infrastructure |

| Asia-Pacific | 15% | 8% | Growing diabetes rates, emerging markets |

| Rest of world | 10% | 6% | Increasing access, urbanization |

Strategic Recommendations

- Continue innovation in device ergonomics and dosing accuracy.

- Strengthen regional marketing, especially in Asia-Pacific.

- Explore biosimilar partnerships or licensing to mitigate price competition.

- Invest in digital health integration for better patient adherence.

Key Takeaways

- SOLOSTAR is a leading prefilled insulin pen with about 30-35% market share.

- Global sales in 2021 were approximately €1.2 billion; forecast to reach €1.4 billion by 2025.

- Growth will be influenced by diabetes prevalence, device innovation, and biosimilar competition.

- Regional differences favor North America and Europe, with rapid growth in Asia-Pacific.

- Long-term market growth depends on innovation and competitive positioning.

FAQs

-

How does SOLOSTAR compare to its competitors in terms of technological features?

SOLOSTAR offers ergonomic design, dose accuracy, and compatibility with multiple insulin formulations. Competitors like Novo Nordisk’s FlexTouch focus on needle-free injection and advanced dose tracking.

-

What are the primary markets for SOLOSTAR?

The United States, Europe, and Asia-Pacific constitute the largest markets, with emerging sales in Latin America and the Middle East.

-

What risks could impact sales growth?

Biosimilar price competition, regulatory delays, and shifts towards alternative therapies like oral or implantable devices.

-

How significant is digital integration for SOLOSTAR?

Currently limited, but future products incorporate digital health features such as dose logging, which could influence market share.

-

What is the outlook for innovation in insulin pen devices?

Companies are investing in smart devices with Bluetooth connectivity, dose memory, and integration with telemedicine platforms to maintain competitive advantage.

References

[1] MarketResearch.com. (2022). Global diabetes treatment market forecast.

[2] Fortune Business Insights. (2023). Insulin delivery devices market analysis.

[3] Sanofi Annual Report. (2022). Sales performance details.

[4] IBISWorld. (2022). Insulin pen manufacturing industry report.

[5] World Health Organization. (2021). Diabetes facts and figures.

More… ↓