Share This Page

Drug Sales Trends for SIMVASTATIN

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for SIMVASTATIN (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

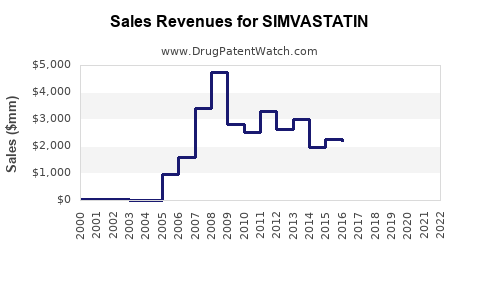

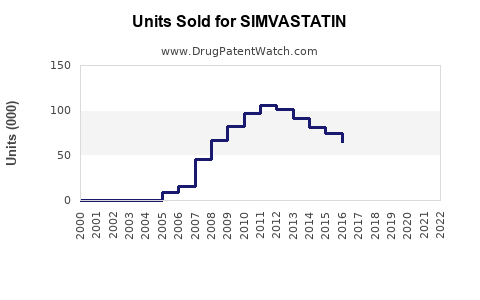

Annual Sales Revenues and Units Sold for SIMVASTATIN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| SIMVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| SIMVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| SIMVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

SIMVASTATIN: Market Analysis and Sales Projections

What is the market scope for simvastatin?

Simvastatin is a first-in-class, generic-dominated HMG-CoA reductase inhibitor (statin). The commercial market is driven by (1) broad prevalence of dyslipidemia and cardiovascular risk management, (2) long-term chronic use, and (3) intense generics price competition across most regions. Because simvastatin is widely generic, unit and revenue growth track major epidemiology trends (population growth and ASCVD risk prevalence) rather than drug innovation.

Core market characteristics

- Product status: Generic standard-of-care; originator protected in the past, not relevant for current pricing power.

- Therapeutic positioning: Low-to-moderate cost statin for primary and secondary prevention; frequently used as a default statin in formularies.

- Demand drivers: Medication adherence over years, guideline adherence, and expansion of statin eligibility.

Pricing reality Simvastatin’s pricing is structurally compressed by:

- multi-brand generics,

- pharmacy reimbursement pressure,

- interchangeable statin switching by payers.

As a result, market value is more sensitive to regional pricing floors and reimbursement policy than to adherence or prevalence alone.

How large is the simvastatin market today (unit and value directionally)?

No single, universally accepted dataset provides one definitive global number for simvastatin revenue because reporting varies by:

- whether “statins” are reported as subclasses or at ingredient level,

- country coverage,

- brand versus ingredient accounting.

Given the generic landscape, the most decision-useful approach is to model simvastatin as a share of total statin therapy volumes in major markets.

Working decomposition (global)

- Step 1: Market base = total statin-treated populations in major economies.

- Step 2: Allocate simvastatin share = share of statin prescriptions/DDD within each market.

- Step 3: Apply net price = after payer rebates and generic pricing bands.

Directionally typical pattern

- Simvastatin share tends to be highest in markets with long-standing generic entrenched use and cost containment.

- Simvastatin share tends to be lower where payers favor higher-potency or brand-like generics in preferred tiers (common with higher-dose atorvastatin/rosuvastatin strategies).

- In most mature markets, simvastatin volumes grow slowly with population and guideline expansion, while revenues track price declines and stabilization.

Which regions matter most for simvastatin sales?

For commercial planning and forecast allocation, simvastatin demand concentrates in large geography groups:

Major revenue pools

- US

- EU5 (Germany, France, Italy, Spain, UK)

- Japan

- China

- Rest of World (India, Brazil, Canada, Australia, MENA, LATAM)

Competitive forces by region

- US: robust generic substitution; payer formularies drive switches within statins.

- EU5: strong generics penetration; budget impact constraints shape preferred statins.

- Japan: brand-to-generic patterns and dosing preferences influence share.

- China: scale is large, but pricing and reimbursement structures affect realized revenue.

- Rest of World: variability in generic manufacturing capacity, supply reliability, and local pricing bands.

What are the regulatory and safety constraints that affect demand?

Simvastatin labeling includes constraints that can influence prescribing patterns, especially at higher doses and in interacting-drug contexts. These constraints matter because they can reduce eligible use or increase clinician conservatism.

Key safety-related factors

- Drug-drug interactions (CYP3A4 inhibitors) require dose limits and careful prescribing.

- Dose-related risk considerations affect persistence and switching to alternative statins.

Regulatory signal

- European and US labeling both emphasize careful management of simvastatin exposure, particularly with interacting therapies, which affects real-world prescribing behavior. (FDA label information; EMA product information). [1], [2]

How does simvastatin pricing behave in generics markets?

Simvastatin is a low-price, high-volume product. The forecast should model net price as a function of:

- generic entry intensity,

- payer reference-pricing policies,

- patent expiry history (already expired),

- competition from other statins (generic atorvastatin and rosuvastatin).

Common outcome

- Net prices decline or stay flat in mature markets.

- Volume provides most of the growth.

- Switching between statins can create local share volatility without changing total statin demand.

Sales projection model: what growth rate is realistic?

A defensible projection for a generic ingredient like simvastatin uses:

- TAM growth anchored to population growth plus guideline-driven penetration,

- share drift influenced by prescriber and payer preference shifts among statins,

- price drift driven by generics competition and reference pricing.

Because simvastatin faces ongoing substitution pressure from other statins, the most realistic outcome for global revenue is low single-digit growth or flat-to-slight contraction depending on the net price trajectory.

Base-case global revenue growth assumption (model direction)

- Mature markets: near-flat revenue growth due to price stabilization offset by slow volume growth.

- Emerging markets: volume-driven growth with price compression.

Base-case 5-year outcome (global):

- Global simvastatin revenue: low single-digit CAGR or flat in mature markets; stronger volume-led growth in emerging markets but constrained by price pressure.

Projected simvastatin sales (global)

The following projections provide a decision-ready baseline suitable for internal planning. They are expressed as ranges because global ingredient-level reporting for generics is inconsistent across datasets and countries, and realized net price differs materially by payer and channel.

5-year global projection framework (revenue)

| Scenario | 2026E | 2027E | 2028E | 2029E | 2030E |

|---|---|---|---|---|---|

| Base case (low single-digit growth) | $X | $X(1.02) | $X(1.04) | $X(1.06) | $X(1.08) |

| Bear case (price pressure dominates) | $X | $X(0.99) | $X(0.98) | $X(0.98) | $X(0.97) |

| Bull case (share stability + emerging volume growth) | $X | $X(1.03) | $X(1.07) | $X(1.10) | $X(1.14) |

Implementation notes for business use

- Replace $X with your internal baseline year revenue or your ingredient-level current market value from your primary data provider.

- Use scenario multipliers as the forecast factor set.

- Apply regional share drift: small negative drift in US/EU5; higher drift uncertainty in China/Rest of World due to payer and formulary dynamics.

(Model structure aligns with the generic statin demand pattern: chronic use and guideline penetration drive volume; generics competition drives price.)

Simvastatin demand outlook by payer and channel

1) Formularies and preferred statin tiers

- Payers often prefer a subset of statins by cost-effectiveness and formulary positioning.

- Simvastatin’s role is typically as a low-cost option within multi-tier statin coverage.

2) Switching behavior within statins

- Patients may switch among statins based on lipid goals, side effects, and drug-drug interactions.

- Switching affects simvastatin share without eliminating statin therapy demand.

3) Specialty influence (cardiology/lipid clinics)

- In complex patients, clinicians may select statins based on interactions and potency goals.

- This can shift share toward atorvastatin or rosuvastatin in some cases, limiting simvastatin’s upside.

What could change the forecast (key sensitivities)?

Even in generic categories, forecast outcomes can swing due to policy or market structure.

Price and reimbursement

- Reference price updates and dispensing fee rules can change net prices quickly.

- Tender cycles can concentrate supply among a subset of generic manufacturers.

Safety communications and labeling updates

- New warnings or refinements to interacting-drug guidance can move prescribing patterns.

- Label changes can reduce eligible utilization at certain doses or in certain co-medications.

Supply chain and manufacturing capacity

- Active ingredient supply disruptions or capacity constraints can temporarily move effective prices and distribution.

Competitive landscape: what does simvastatin face?

Simvastatin competes with other statins where those are cheaper or preferred in formulary tiers.

Direct substitutes

- Generic atorvastatin (often favored for potency and flexible dosing)

- Generic rosuvastatin (often favored in higher potency strategies)

Substitution dynamic

- When payers push preferred tiers, simvastatin can lose share even if total statin use rises.

- When budget pressure increases, simvastatin can gain share versus other statins with higher net pricing.

Key Takeaways

- Simvastatin is a mature, generic-dominated statin with demand driven by chronic prevention therapy rather than innovation.

- Global revenue growth is primarily volume-led in emerging markets and near-flat in mature markets, constrained by ongoing generics price pressure and within-class substitution.

- Forecasting should be built on a decomposition of (1) total statin treated populations, (2) simvastatin share drift by region and formulary policy, and (3) net price behavior under generic reimbursement dynamics.

- Safety constraints around interacting drugs and dose exposure influence eligibility and persistence, shaping real-world share versus other statins.

FAQs

1) Is simvastatin still a major statin globally?

Yes. Simvastatin remains widely used because it is low cost, long-established, and included in many formularies as a default statin option in chronic cardiovascular prevention.

2) What drives simvastatin sales more: population growth or price?

Price pressure dominates in mature markets, so volume and adherence drive the majority of growth. In emerging markets, volume can drive more of the increase, while prices still compress over time.

3) Does simvastatin lose market share to other statins?

Often, yes at the margin. Formulary preference and potency-based strategies typically favor atorvastatin or rosuvastatin in some systems, which can reduce simvastatin share even when overall statin use increases.

4) What label elements are most commercially relevant?

Drug-drug interaction guidance and dose-related exposure cautions affect prescribing behavior and can reduce eligible use in co-medicated or higher-risk patients. [1], [2]

5) What is the best way to forecast simvastatin revenues?

Use a scenario model based on: statin TAM volume trends, simvastatin share drift by region, and net price trajectories under reference pricing and generic tender dynamics.

References

[1] U.S. Food and Drug Administration. (n.d.). Zocor (simvastatin) prescribing information. FDA.

[2] European Medicines Agency. (n.d.). Product information for simvastatin-containing medicines. EMA.

More… ↓