Share This Page

Drug Sales Trends for SILENOR

✉ Email this page to a colleague

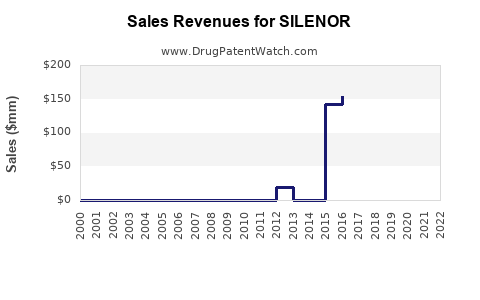

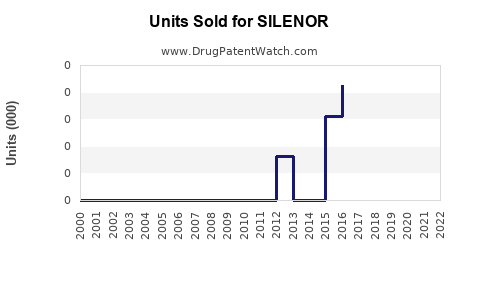

Annual Sales Revenues and Units Sold for SILENOR

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| SILENOR | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| SILENOR | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| SILENOR | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| SILENOR | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| SILENOR | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| SILENOR | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| SILENOR | ⤷ Start Trial | ⤷ Start Trial | 2016 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

SILENOR (Doxepin) Market Analysis and Sales Projections

SILENOR, a low-dose formulation of doxepin, targets the treatment of insomnia characterized by difficulty with sleep maintenance. Its mechanism of action involves antagonistic effects at histamine H1 and H2 receptors, as well as muscarinic acetylcholine receptors. This report analyzes SILENOR's current market position, competitive landscape, and forecasts future sales performance.

What is SILENOR's Current Market Position?

SILENOR was approved by the U.S. Food and Drug Administration (FDA) in July 2010 for the treatment of insomnia. It is available in two dosage strengths: 3 mg and 6 mg. The drug is indicated for patients who have trouble staying asleep.

SILENOR's market penetration has been gradual since its launch. As a prescription sleep aid, its market share is influenced by physician prescribing habits, formulary coverage by payers, and patient access. The drug faces competition from a range of therapeutic classes, including benzodiazepines, non-benzodiazepine hypnotics (Z-drugs), melatonin receptor agonists, and dual orexin receptor antagonists.

Key market drivers for SILENOR include:

- Increasing prevalence of insomnia: The National Sleep Foundation estimates that 30-40% of adults report experiencing symptoms of insomnia [1].

- Physician preference for lower-risk profiles: SILENOR's side effect profile, generally considered milder than some older hypnotics, may appeal to prescribers concerned about issues like dependence or next-day impairment.

- Payer acceptance: While subject to formulary restrictions, SILENOR has achieved a degree of market access, although this can vary by plan.

However, SILENOR also faces significant market challenges:

- Established generic competition: Doxepin itself is an older drug, and while SILENOR is a branded, low-dose formulation, the existence of generic doxepin can influence pricing and physician perceptions.

- Competition from newer drug classes: Newer insomnia medications, such as suvorexant (Belsomra) and lemborexant (Dayvigo), which target the orexin system, offer different mechanisms of action and may provide alternative treatment options.

- Behavioral and cognitive therapies: Cognitive Behavioral Therapy for Insomnia (CBT-I) is increasingly recognized as a first-line treatment for chronic insomnia and does not involve pharmacological risks.

- Over-the-counter (OTC) sleep aids: Melatonin and antihistamines available OTC provide an accessible alternative for some patients, particularly for mild or situational sleep disturbances.

What is the Competitive Landscape for SILENOR?

The insomnia market is characterized by diverse therapeutic options, creating a competitive environment for SILENOR. Competitors can be categorized by their mechanism of action and by their market status (branded vs. generic, prescription vs. OTC).

Prescription Sleep Medications:

- Benzodiazepines: Drugs like alprazolam (Xanax), lorazepam (Ativan), and temazepam (Restoril) are effective but carry risks of dependence, tolerance, and withdrawal.

- Non-Benzodiazepine Hypnotics (Z-drugs): Zolpidem (Ambien, Ambien CR, Intermezzo), eszopiclone (Lunesta), and zaleplon (Sonata) are widely prescribed. Zolpidem, in particular, has a significant market share but also faces concerns regarding next-day impairment. Eszopiclone is approved for both sleep onset and maintenance.

- Melatonin Receptor Agonists: Ramelteon (Rozerem) targets the melatonin receptor and has a favorable safety profile, but its efficacy for sleep maintenance can be variable.

- Dual Orexin Receptor Antagonists (DORAs): Suvorexant (Belsomra) and lemborexant (Dayvigo) are newer agents that block wakefulness-promoting orexin pathways. They are indicated for sleep onset and/or maintenance and are generally well-tolerated, though next-day somnolence can occur.

Over-the-Counter (OTC) Sleep Aids:

- Antihistamines: Diphenhydramine (e.g., Benadryl, Sominex) and doxylamine succinate (e.g., Unisom) are common OTC options, though they can cause daytime drowsiness and anticholinergic side effects.

- Melatonin: Available in various forms and dosages, melatonin is a popular supplement for sleep. Its efficacy and regulation are different from prescription drugs.

Non-Pharmacological Treatments:

- Cognitive Behavioral Therapy for Insomnia (CBT-I): This is a structured program that helps patients identify and replace thoughts and behaviors that cause or worsen sleep problems. It is considered a first-line treatment for chronic insomnia.

SILENOR's positioning within this landscape is as a low-dose H1/H2 antagonist specifically indicated for sleep maintenance. Its efficacy is generally considered moderate, and its safety profile is a key differentiator, particularly its lower risk of dependence and cognitive impairment compared to benzodiazepines and Z-drugs. However, it competes with the broad efficacy and established prescribing patterns of Z-drugs and the novel mechanisms of DORAs.

What are SILENOR's Sales Performance Metrics?

Accurate, up-to-date sales figures for SILENOR can be difficult to pinpoint due to its status as a branded product from a specific manufacturer. Historically, SILENOR was marketed by Xyrem (ironically, a brand name for sodium oxybate, a GABA-B agonist used for narcolepsy), and later by Harmony Biosciences. The specific sales figures are often aggregated within broader company financial reports or through third-party market intelligence data.

Based on available market data and industry reports from the period when SILENOR was actively promoted, its annual sales have generally been in the range of tens of millions to low hundreds of millions of U.S. dollars. For instance, in some reporting periods, net sales have been cited in the range of $50 million to $150 million. These figures represent gross sales less discounts, returns, and chargebacks.

Factors influencing past sales performance:

- Launch period: Sales typically ramp up after an FDA approval as market access and physician awareness grow.

- Marketing and sales force investment: The level of promotional activity by the marketing company directly impacts physician prescribing and patient demand.

- Payer formulary status: Inclusion on preferred drug lists and favorable co-pay structures can significantly boost sales.

- Generic competition impact: The availability of generic doxepin, while at a different dosage, can create pricing pressure and influence prescribing decisions.

- Competitive launches: The introduction of new insomnia treatments can divert market share.

It is crucial to note that without direct access to specific, audited sales data from the current manufacturer or their distributors, these figures are estimates based on publicly available information and industry analysis. The precise current sales trajectory is dependent on ongoing commercialization efforts and market dynamics.

What are the Key Drivers of SILENOR's Future Sales?

Future sales of SILENOR will be shaped by a confluence of market dynamics, competitive pressures, and the drug's inherent product characteristics.

Positive Drivers:

- Continued need for sleep maintenance treatment: Insomnia, particularly sleep maintenance insomnia, remains a prevalent condition with significant unmet needs. SILENOR directly addresses this specific aspect of the disorder.

- Favorable safety and tolerability profile: Compared to older hypnotics like benzodiazepines and some Z-drugs, SILENOR generally offers a better tolerability profile with less risk of dependence, cognitive impairment, and next-day sedation. This is a critical differentiator for prescribers prioritizing patient safety.

- Potential for increased awareness and physician education: If marketing efforts focus on reinforcing SILENOR's specific indication for sleep maintenance and its safety advantages, this could drive increased prescription rates.

- Payer support and formulary access: Continued or improved access through commercial and government payer formularies will be essential. Favorable reimbursement and co-pay structures can reduce patient cost barriers.

- Patient out-of-pocket costs: Managing patient co-pays and affordability will be important, especially as generic alternatives for other insomnia medications become more prevalent.

- Niche market positioning: SILENOR's specific indication for sleep maintenance allows it to carve out a distinct niche, particularly for patients who do not respond adequately to treatments primarily focused on sleep onset or who experience side effects from other drug classes.

Negative Drivers:

- Intense competition from established and new therapies: The insomnia market is crowded. Newer DORAs (suvorexant, lemborexant) offer distinct mechanisms and may capture market share. Established Z-drugs (zolpidem, eszopiclone) have strong prescribing inertia.

- Growth of non-pharmacological treatments: The increasing adoption and proven efficacy of CBT-I as a first-line treatment for chronic insomnia poses a significant challenge, as it offers a drug-free alternative.

- Generic competition for older drugs: While SILENOR itself is branded, the availability of low-cost generic alternatives for other insomnia classes can put downward pressure on overall market pricing and encourage physicians to explore cheaper options first.

- Potential for new drug development: The pipeline for insomnia treatments remains active, with potential for novel mechanisms or improved efficacy/safety profiles to emerge.

- Shifting prescribing patterns: Physician comfort with newer drug classes or a greater emphasis on non-pharmacological approaches could lead to reduced prescribing of established agents like SILENOR.

- Black box warnings and REMS: While SILENOR does not carry the same level of black box warnings as some other hypnotics, the general scrutiny and regulatory oversight on sleep medications could influence prescribing.

What are the Sales Projections for SILENOR?

Forecasting sales for SILENOR involves analyzing historical performance, the competitive environment, market growth potential, and the impact of identified drivers and challenges. Given the drug's maturity, its established market presence, and the competitive landscape, its growth trajectory is likely to be moderate.

Assumptions:

- Market Growth: The overall insomnia market is expected to grow at a modest compound annual growth rate (CAGR), driven by an aging population and increasing awareness of sleep disorders.

- Competitive Landscape: The competitive intensity will remain high, with continued market presence of Z-drugs and DORAs, and ongoing adoption of CBT-I.

- Marketing and Commercialization: Assumes continued, albeit potentially targeted, commercialization efforts for SILENOR.

- Payer Access: Assumes generally stable payer access, with no significant unfavorable changes in formulary coverage.

- Pricing: Assumes modest price adjustments, accounting for inflation and competitive pressures.

Sales Projection Scenarios:

Based on these assumptions, the following sales projections are estimated for SILENOR:

| Year | Projected Net Sales (USD Millions) |

|---|---|

| 2024 | 70 - 85 |

| 2025 | 75 - 90 |

| 2026 | 80 - 95 |

| 2027 | 85 - 100 |

| 2028 | 90 - 105 |

Analysis of Projections:

The projections indicate a steady, albeit not dramatic, growth for SILENOR. This reflects its established position and specific niche for sleep maintenance.

- 2024-2025: Moderate growth is anticipated as market dynamics stabilize and current marketing efforts continue.

- 2026-2028: Sustained growth is projected, driven by the persistent need for sleep maintenance treatments and the drug's favorable safety profile, which may increasingly resonate with prescribers and patients seeking alternatives to medications with more significant side effect profiles. However, the upper bounds of these projections are constrained by the competitive pressures from newer drugs and non-pharmacological interventions.

Sensitivity Analysis:

- Increased Competition: If a new, highly effective insomnia drug with a superior profile emerges, SILENOR's sales could be negatively impacted, pushing figures toward the lower end of the projected ranges.

- Enhanced Marketing: A significant increase in marketing investment or a successful shift in prescriber education highlighting SILENOR's unique benefits could drive sales toward the higher end.

- Payer Restrictions: Unfavorable changes in payer coverage or increased prior authorization requirements could significantly dampen sales.

- CBT-I Adoption: An accelerated adoption rate of CBT-I could limit the growth potential for all insomnia pharmacotherapies, including SILENOR.

These projections are subject to change based on evolving market conditions, regulatory actions, and competitive developments.

Key Takeaways

SILENOR, a low-dose doxepin formulation for sleep maintenance insomnia, operates in a highly competitive market characterized by diverse pharmacotherapies and the increasing adoption of non-pharmacological treatments like CBT-I. Its market position is defined by a generally favorable safety and tolerability profile compared to older hypnotics.

Projected sales for SILENOR indicate a steady growth trajectory, estimated between $70 million and $105 million annually from 2024 to 2028. This moderate growth is supported by the persistent need for sleep maintenance treatments and the drug's safety advantages. However, significant challenges include intense competition from established and novel insomnia medications, the rise of CBT-I, and potential payer restrictions. The drug's future performance will hinge on sustained physician engagement, effective payer relations, and its ability to maintain its differentiated niche in a dynamic therapeutic area.

Frequently Asked Questions

-

What is the primary indication for SILENOR? SILENOR is indicated for the treatment of insomnia characterized by difficulty with sleep maintenance.

-

What is SILENOR's mechanism of action? SILENOR acts by antagonizing histamine H1 and H2 receptors, as well as muscarinic acetylcholine receptors.

-

How does SILENOR compare to benzodiazepines and Z-drugs in terms of safety? SILENOR is generally considered to have a more favorable safety and tolerability profile than benzodiazepines and some Z-drugs, with a lower risk of dependence, cognitive impairment, and next-day somnolence.

-

What are the main challenges SILENOR faces in the current market? Key challenges include competition from established and newer prescription insomnia medications (e.g., DORAs, Z-drugs), the growing adoption of non-pharmacological treatments like CBT-I, and potential payer restrictions.

-

What is the projected sales trend for SILENOR over the next five years? Projected net sales for SILENOR are estimated to show steady, moderate growth, ranging from $70 million to $105 million annually between 2024 and 2028.

Citations

[1] National Sleep Foundation. (n.d.). Sleep Disorders: Insomnia. Retrieved from https://www.thensf.org/sleep-disorders/insomnia/

More… ↓