Share This Page

Drug Sales Trends for RESTASIS OP

✉ Email this page to a colleague

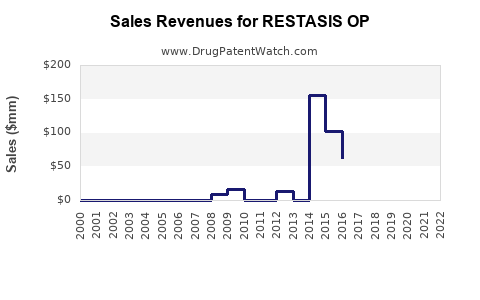

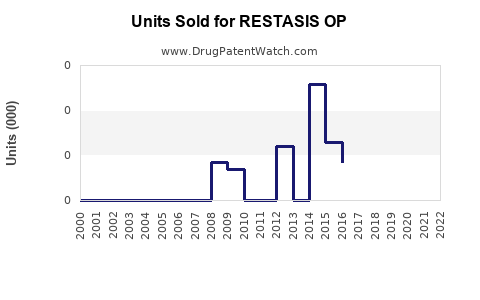

Annual Sales Revenues and Units Sold for RESTASIS OP

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| RESTASIS OP | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| RESTASIS OP | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| RESTASIS OP | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| RESTASIS OP | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| RESTASIS OP | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

RESTASIS OP Patent Landscape and Sales Projections

RESTASIS OP (cyclosporine ophthalmic emulsion) faces a complex patent environment, with its primary composition of matter patent expiring in 2024, alongside multiple formulation, method of use, and manufacturing process patents extending into the mid-2030s. This analysis projects near-term sales decline due to generic competition and outlines potential revenue streams from extended patent protections.

RESTASIS OP: Key Patent Expirations

The cornerstone patent for RESTASIS OP, U.S. Patent No. 4,649,043 (composition of matter), is set to expire on November 18, 2024. This expiration marks a critical juncture, opening the door for generic entrants to offer bioequivalent products.

Several secondary patents, however, extend the intellectual property protection for RESTASIS OP and its related technologies. These include:

- Formulation Patents: Patents covering specific emulsion compositions, particle sizes, and excipients.

- Method of Use Patents: Patents related to specific treatment regimens or indications for dry eye disease.

- Manufacturing Process Patents: Patents detailing novel or improved methods for producing the ophthalmic emulsion.

Table 1: Key RESTASIS OP Patents and Expiration Dates

| Patent Number | Title | Filed Date | Expiration Date | Technology Covered |

|---|---|---|---|---|

| 4,649,043 | Immunosuppressive compositions | 1985-12-19 | 2024-11-18 | Composition of Matter |

| 6,156,770 | Ophthalmic Emulsion Formulations | 1998-07-10 | 2026-08-08 | Specific Emulsion Composition |

| 7,399,764 | Method of treating dry eye syndrome | 2004-03-09 | 2025-01-14 | Method of Use |

| 8,629,159 | Ophthalmic Emulsion and Methods of Use Thereof | 2008-09-02 | 2031-08-23 | Formulation and Method of Use |

| 9,078,976 | Ophthalmic Emulsion with Improved Stability | 2011-06-20 | 2034-09-20 | Formulation (Stability Enhancement) |

| 9,387,250 | Method for Manufacturing Ophthalmic Emulsions | 2012-04-18 | 2033-05-01 | Manufacturing Process |

| 9,717,601 | Ophthalmic Emulsion Formulations | 2013-08-27 | 2035-06-19 | Specific Emulsion Composition |

| 10,022,569 | Ophthalmic Emulsion Formulations and Methods of Use | 2015-03-25 | 2035-07-17 | Formulation and Method of Use |

| 10,555,898 | Ophthalmic Emulsion Compositions | 2017-01-10 | 2036-02-18 | Formulation |

Source: U.S. Patent and Trademark Office (USPTO) database. Dates are approximate and subject to maintenance fee payments and potential legal challenges.

Generic Entry and Sales Impact

The expiration of U.S. Patent No. 4,649,043 in November 2024 is anticipated to trigger a substantial decline in RESTASIS OP's market share and revenue. Generic manufacturers, having successfully navigated or awaiting approval of their Abbreviated New Drug Applications (ANDAs), will introduce lower-cost alternatives.

Historically, branded ophthalmic products have experienced revenue erosion of 60% to 80% within the first 12-24 months of generic entry, depending on the number of approved generics and their pricing strategies [1].

Projected Sales Trajectory for RESTASIS OP:

- 2024 (Q4): Pre-expiration sales; stable revenue.

- 2025 (Q1-Q4): Significant revenue decline commencing with generic launches. Estimated revenue drop of 40-60% compared to 2024 annual figures.

- 2026 onwards: Continued market share erosion. Revenue stabilization at a significantly lower baseline, representing the retained market share of the branded product and patient preference for the originator.

Factors Influencing Generic Erosion:

- Number of Generic Competitors: Multiple approved generics intensify price competition.

- Pricing Strategies: Aggressive pricing by generic manufacturers will accelerate market share capture.

- Payer Formularies: Inclusion of generics on insurance formularies will drive physician and patient adoption.

- Physician Prescribing Habits: Established prescribing patterns for RESTASIS OP may lead to a slower, but inevitable, shift to generics.

Extended Patent Protection Opportunities

While the composition of matter patent expires, the suite of secondary patents offers avenues for continued revenue generation and market differentiation. These patents can protect:

- New Formulations: Development of novel formulations with improved efficacy, tolerability, or convenience (e.g., preservative-free versions, enhanced delivery systems).

- Combination Therapies: Patenting methods of using RESTASIS OP in conjunction with other therapeutic agents for synergistic effects in treating dry eye disease.

- Specific Patient Subgroups: Identifying and patenting specific patient populations who derive particular benefit from RESTASIS OP or its modified forms.

- Manufacturing Innovations: Patents on more efficient or cost-effective manufacturing processes can contribute to long-term cost of goods advantages.

Strategic Considerations for Extended Protection:

- Reformulation Efforts: Invest in R&D to develop next-generation formulations that circumvent existing generic formulations or offer distinct advantages. This could lead to a "RESTASIS 2.0" with new patent protection.

- Lifecycle Management: Proactively identify and pursue patent protection for incremental innovations and improvements to the existing product.

- Litigation Strategy: Vigilantly monitor generic manufacturers for potential patent infringement and actively pursue legal remedies when warranted. The strength and enforceability of secondary patents will be crucial.

Sales Projections: Post-Generic Entry

Post-generic entry, the sales trajectory of RESTASIS OP will be bifurcated. The originator product will likely capture a reduced, but stable, market share driven by brand loyalty, physician preference, and potentially physician-administered product.

Estimated Branded RESTASIS OP Sales (USD Millions):

- 2024: $1,500 - $1,600 (based on recent annual sales figures)

- 2025: $600 - $900 (estimated 40-60% decline)

- 2026: $400 - $600 (continued decline and stabilization)

- 2027: $300 - $500 (stabilized baseline)

- 2028-2035: Gradual decline, potentially influenced by the expiration of key secondary patents or the introduction of superior generic alternatives in later years. Sales in this period could range from $100 - $300 million annually, depending on the success of lifecycle management strategies and the market penetration of next-generation products.

These projections assume no significant new indications or blockbuster combination therapies emerge that dramatically alter the treatment landscape. The introduction of novel therapeutic modalities for dry eye disease could also impact RESTASIS OP's market position.

Key Takeaways

- The primary U.S. patent for RESTASIS OP expires in November 2024, necessitating a strategic response to impending generic competition.

- Significant sales erosion, estimated at 40-60% in the first year post-generic entry, is anticipated.

- A portfolio of secondary patents extends intellectual property protection for formulations, methods of use, and manufacturing processes, offering opportunities for continued revenue.

- Lifecycle management strategies, including reformulation and R&D into next-generation products, are critical for maximizing value from extended patent life.

- Branded RESTASIS OP sales are projected to stabilize at a reduced baseline post-generic entry, with potential for gradual decline through 2035.

Frequently Asked Questions

-

What is the primary reason for the anticipated decline in RESTASIS OP sales? The expiration of the composition of matter patent (U.S. Patent No. 4,649,043) in November 2024 permits generic manufacturers to introduce lower-cost bioequivalent versions of the drug.

-

How many significant secondary patents protect RESTASIS OP, and what do they cover? There are at least nine significant secondary patents covering formulations, methods of use, and manufacturing processes. These patents extend protection through the mid-2030s, offering avenues to protect specific product attributes or treatment approaches beyond the initial composition of matter patent.

-

What is the typical sales impact for branded ophthalmic drugs following generic entry? Branded ophthalmic products typically experience revenue erosion of 60% to 80% within 12-24 months of generic launches.

-

Beyond generic competition, what other market factors could affect RESTASIS OP sales in the coming years? The introduction of novel therapeutic modalities for dry eye disease, changes in payer coverage and formulary placement, and the efficacy and adoption rates of competing generic products will all influence RESTASIS OP's market position.

-

What strategic actions can be taken to mitigate the impact of generic competition and leverage extended patent protections? Key strategies include investing in R&D for next-generation formulations, developing combination therapies, identifying and patenting new uses in specific patient populations, and vigilantly defending existing intellectual property through litigation.

Citations

[1] U.S. Patent and Trademark Office. (n.d.). Patent Search Database. Retrieved from https://patft.uspto.gov/

More… ↓