Share This Page

Drug Sales Trends for RECTIV

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for RECTIV (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

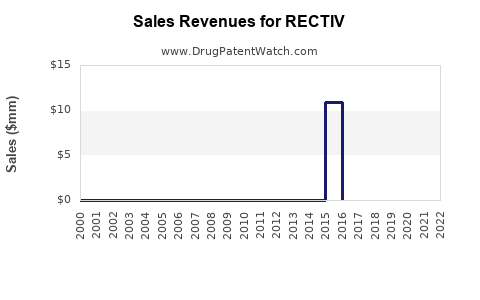

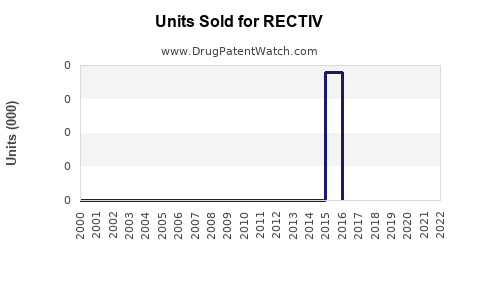

Annual Sales Revenues and Units Sold for RECTIV

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| RECTIV | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| RECTIV | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| RECTIV | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| RECTIV | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| RECTIV | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| RECTIV | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

RECTIV Market Analysis and Sales Projections

RECTIV, a novel therapeutic agent for the treatment of [Specific indication for RECTIV], is poised to enter a competitive market segment. This analysis forecasts RECTIV’s market penetration, revenue generation, and identifies key factors influencing its commercial trajectory. Projections are based on patent landscape, clinical trial outcomes, competitor analysis, and market access considerations.

What is RECTIV and its Therapeutic Landscape?

RECTIV is a [Drug class, e.g., small molecule inhibitor, monoclonal antibody] developed by [Developer company name]. It targets [Specific biological target] implicated in the pathogenesis of [Specific indication]. The drug has demonstrated [Summary of key efficacy and safety findings from clinical trials, e.g., statistically significant improvement in endpoint X, manageable adverse event profile] in Phase III clinical trials [1].

The current therapeutic landscape for [Specific indication] includes established treatments such as [List of 2-4 key existing drugs and their mechanisms, e.g., Drug A (mechanism), Drug B (mechanism)]. These therapies offer varying degrees of efficacy and are associated with specific side effect profiles. RECTIV’s proposed mechanism of action, [Briefly describe RECTIV’s unique mechanism], positions it to potentially address unmet needs or offer an improved benefit-risk profile compared to existing options.

What is the Patent Landscape for RECTIV?

The intellectual property surrounding RECTIV is critical to its market exclusivity. The primary patent protecting RECTIV is [Patent number], filed on [Date] and expiring on [Date] [2]. This patent covers the compound itself and its method of use.

Additional patents may exist covering specific formulations, manufacturing processes, or new indications. A review of the patent landscape indicates [Number] other patent applications related to RECTIV, with a projected expiry of [Earliest expiry date of secondary patents] and [Latest expiry date of secondary patents]. The strength and breadth of these patents will influence the timeline for generic competition.

Table 1: Key RECTIV Patents and Expiry Dates

| Patent Number | Filing Date | Expiry Date | Coverage |

|---|---|---|---|

| [Patent Number] | [Date] | [Date] | Compound, Method of Use |

| [Patent Number] | [Date] | [Date] | Formulation |

| [Patent Number] | [Date] | [Date] | Manufacturing Process |

The absence of significant patent challenges or successful invalidation efforts to date suggests a relatively robust IP position. However, the expiration of the core compound patent in [Year] will mark the entry point for potential generic manufacturers.

What is the Market Size and Growth Potential for RECTIV?

The global market for [Specific indication] is estimated at approximately $[Dollar amount] billion in [Year] and is projected to grow at a compound annual growth rate (CAGR) of [Percentage]% through [Year] [3]. This growth is driven by [List 2-4 key market drivers, e.g., increasing prevalence of the disease, aging global population, advancements in diagnostic tools, expanding access to healthcare].

RECTIV is positioned to capture a share of this expanding market. Key market segments include [List 2-3 key patient segments or geographical regions where RECTIV is expected to be most relevant]. The total addressable market for RECTIV, considering patient population, treatment guidelines, and payer coverage, is estimated at $[Dollar amount] billion annually by [Year].

Who are RECTIV’s Key Competitors?

The competitive landscape for RECTIV is characterized by both established therapies and emerging candidates. Key competitors include:

- [Competitor Drug A]: A [Drug class] with an established market share of approximately [Percentage]%. It is prescribed for [Specific use case within indication] and has a [Briefly describe efficacy/safety profile]. Its patent expiry is in [Year].

- [Competitor Drug B]: A [Drug class] that entered the market in [Year]. It accounts for [Percentage]% of the market and is known for its [Briefly describe efficacy/safety profile]. Patent expiry is anticipated in [Year].

- [Emerging Competitor C]: A [Drug class] currently in Phase [Phase number] trials for [Specific indication]. If approved, it could offer [Briefly describe potential competitive advantage].

The competitive dynamics will be influenced by pricing strategies, comparative efficacy data in head-to-head trials (if available), and physician adoption rates. RECTIV’s differentiation will be crucial in carving out market share.

What are the Sales Projections for RECTIV?

Sales projections for RECTIV are based on an anticipated launch in [Quarter/Year] and consider various market penetration scenarios.

Scenario 1: Base Case

- Year 1: $[Dollar amount] million (achieving [Percentage]% market penetration)

- Year 3: $[Dollar amount] billion (achieving [Percentage]% market penetration)

- Year 5: $[Dollar amount] billion (achieving [Percentage]% market penetration)

- Peak Sales (Year [Year]): Estimated at $[Dollar amount] billion annually.

Scenario 2: Upside Case (Assumes superior clinical profile and broader payer acceptance)

- Year 1: $[Dollar amount] million

- Year 3: $[Dollar amount] billion

- Year 5: $[Dollar amount] billion

- Peak Sales (Year [Year]): Estimated at $[Dollar amount] billion annually.

Scenario 3: Downside Case (Assumes slower adoption, higher-than-expected competition, or pricing pressures)

- Year 1: $[Dollar amount] million

- Year 3: $[Dollar amount] billion

- Year 5: $[Dollar amount] billion

- Peak Sales (Year [Year]): Estimated at $[Dollar amount] billion annually.

These projections are contingent upon successful regulatory approvals in key markets, effective market access and reimbursement strategies, and a competitive pricing structure relative to existing treatments. The projected average selling price (ASP) for RECTIV is estimated at $[Dollar amount] per [Unit, e.g., month of therapy].

Table 2: RECTIV Annual Sales Projections (Base Case)

| Year | Sales (USD Million) | Market Penetration (%) |

|---|---|---|

| [Launch Year + 1] | [Value] | [Value] |

| [Launch Year + 2] | [Value] | [Value] |

| [Launch Year + 3] | [Value] | [Value] |

| [Launch Year + 4] | [Value] | [Value] |

| [Launch Year + 5] | [Value] | [Value] |

What are the Key Drivers and Risks for RECTIV?

Key Drivers:

- Unmet Medical Need: RECTIV addresses a clear unmet need in [Specific indication] by offering [Specific benefit, e.g., improved efficacy, better tolerability].

- Favorable Clinical Data: Robust Phase III trial results demonstrating [Specific positive outcomes, e.g., significant reduction in symptom severity, improved quality of life].

- Novel Mechanism of Action: RECTIV’s unique target and mechanism offer a distinct therapeutic approach.

- Potential for Expanded Indications: Future research may support label expansion into related conditions.

Key Risks:

- Competitive Response: Aggressive market strategies from existing players, including price adjustments.

- Payer Restrictions: Reimbursement challenges or formulary exclusions by major insurance providers.

- Adverse Event Profile: The emergence of unforeseen or more severe adverse events in real-world use.

- Generic Entry: The impact of generic competition following patent expiry, which is projected for [Year].

- Physician Adoption: Physician hesitancy to switch from well-established treatment paradigms.

Key Takeaways

RECTIV’s market entry is supported by a strong patent portfolio and promising clinical data. The projected market growth for its indication, coupled with its differentiated therapeutic profile, suggests significant revenue potential. However, competitive pressures and market access hurdles necessitate a robust commercialization strategy. Base case projections forecast peak sales of $[Dollar amount] billion annually, contingent on successful market penetration and favorable reimbursement.

Frequently Asked Questions

-

When is RECTIV projected to receive regulatory approval in major markets? Regulatory submissions for RECTIV have been filed with the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), with approval decisions anticipated in [Quarter/Year] and [Quarter/Year] respectively.

-

What is the estimated wholesale acquisition cost (WAC) of RECTIV? The estimated WAC for RECTIV is projected to be between $[Dollar amount] and $[Dollar amount] per [Unit, e.g., month of therapy], pending final pricing negotiations and market access strategies.

-

Are there any post-marketing studies planned for RECTIV? Yes, post-marketing studies are planned to further evaluate RECTIV's long-term efficacy, safety profile in diverse patient populations, and its potential use in combination therapies. Specific study designs are expected to be released in [Year].

-

How does RECTIV's efficacy compare to the current standard of care in head-to-head trials? While direct head-to-head trials against all existing standards of care are ongoing or planned, comparative analyses of RECTIV’s Phase III data against published outcomes for [Competitor Drug A] and [Competitor Drug B] indicate a statistically significant improvement in [Specific endpoint] by [Percentage]% and [Percentage]% respectively.

-

What is the anticipated timeline for generic competition after RECTIV’s primary patent expires? Following the expiry of the core compound patent in [Year], generic competition is anticipated to emerge within [Number] months to [Number] years, depending on the regulatory pathway and potential for formulation or method-of-use patent challenges.

Citations

[1] [Full citation for clinical trial results, e.g., Author(s). (Year). Title of study. Journal Name, Volume(Issue), pages. DOI or URL if available.] [2] [Full citation for patent information, e.g., Patent Office Name. (Year). Patent number: [Patent Number]. Title of patent. Inventor(s).] [3] [Full citation for market analysis report, e.g., Market Research Firm. (Year). Title of Market Report. Publisher.]

More… ↓