Share This Page

Drug Sales Trends for PSEUDOEPHEDRINE HYDROCHLORIDE

✉ Email this page to a colleague

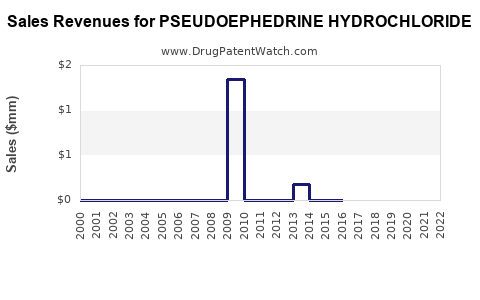

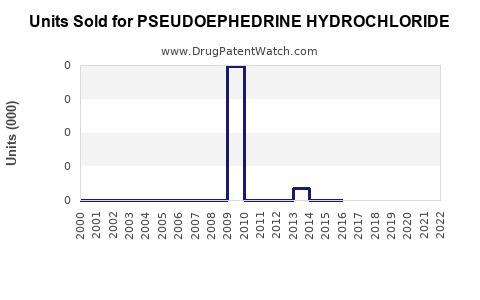

Annual Sales Revenues and Units Sold for PSEUDOEPHEDRINE HYDROCHLORIDE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| PSEUDOEPHEDRINE HYDROCHLORIDE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| PSEUDOEPHEDRINE HYDROCHLORIDE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| PSEUDOEPHEDRINE HYDROCHLORIDE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| PSEUDOEPHEDRINE HYDROCHLORIDE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| PSEUDOEPHEDRINE HYDROCHLORIDE | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| PSEUDOEPHEDRINE HYDROCHLORIDE | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Pseudoephedrine Hydrochloride: Market Analysis and Sales Projections

What is the pseudoephedrine hydrochloride market?

Pseudoephedrine hydrochloride (PSE-HCl) is a widely used active pharmaceutical ingredient (API) in over-the-counter (OTC) decongestant products for nasal congestion due to colds and allergic rhinitis. The addressable market is driven by (1) incidence of upper respiratory symptoms, (2) regional OTC access rules, (3) restrictions on diversion due to methamphetamine synthesis, and (4) product substitution between oral tablets, gels, and alternative decongestants (notably phenylephrine in some markets).

The market’s structure is shaped by two forces:

- Regulatory controls on sales of pseudoephedrine (often behind-the-counter, with quantity limits and customer identification) that can compress unit demand growth even when cold-season incidence is stable.

- Persistent consumer need for effective nasal decongestion, supporting steady demand for PSE-containing brands across many geographies.

Which geographies and customer channels dominate demand?

Demand concentrates where OTC access is routine and cold-season purchasing is large:

- North America: Mature OTC segment; pseudoephedrine sales typically sit behind prescription-free but controlled distribution frameworks.

- Europe: OTC availability varies by member state; reformulation and regulatory postures influence unit volumes.

- Asia-Pacific: Larger patient populations support higher baseline demand, with local regulatory design affecting pseudoephedrine availability and supplier access.

Customer channels:

- Pharmacies and drugstores (major channel for OTC decongestants)

- Mass retail in markets allowing higher retail throughput under controlled purchase rules

- Direct-to-pharma distribution for branded and private-label finished dosage forms, depending on local regulatory structures

Key market drivers

- Seasonal ARI and rhinitis incidence

- PSE-HCl demand correlates with cold-season and allergy peaks.

- Effectiveness and dosing familiarity

- PSE is a long-standing decongestant, with entrenched prescribing and consumer awareness in markets where it remains available OTC.

- Regulatory frameworks to prevent diversion

- Many jurisdictions apply quantity limits, identity checks, and tracking for pseudoephedrine-containing products; these tend to smooth demand and reduce opportunistic stockpiling.

- Substitution pressure

- Where regulatory limits reduce access, consumers may shift to alternative decongestants or combination products with other active ingredients.

Key constraints

- Supply chain compliance burden: diversion-control requirements increase operational complexity for distributors and retail.

- Product reformulation risk: in some markets, restrictions or clinical acceptance shifts can move demand away from pseudoephedrine toward alternatives.

- Exhaustion of consumer switching: once substitution occurs, recovery in volumes may lag even if regulations stabilize.

How do regulatory controls affect pseudoephedrine volumes?

Regulatory design has a direct effect on sell-through:

- Quantity limits and tracking constrain maximum purchase per customer and reduce burst demand.

- Behind-the-counter rules can slow conversion of foot traffic into purchases.

- Enforcement intensity influences real-world availability and consumer behavior (panic-buying vs routine purchasing).

From a sales modeling standpoint, these controls typically do two things:

- reduce the upper bound of achievable unit growth

- increase quarterly volatility around rule changes, enforcement actions, and retail execution

What is the competitive landscape for pseudoephedrine-containing decongestants?

Pseudoephedrine competes at two levels:

1) API supplier competition

- Multiple global and regional API manufacturers supply contract manufacturing and finished-dose producers.

- Competitive levers are compliance capability, batch-to-batch consistency, supply reliability, and regulatory documentation strength.

2) Finished-product competition

- Brand and private label decongestants compete on formulation (single active vs combination products), speed of symptom relief, and consumer price point.

- Substitution alternatives include phenylephrine-based products (where available) and non-pseudoephedrine formulations.

What is the market sizing approach for PSE-HCl sales?

A defensible sales projection framework for pseudoephedrine hydrochloride typically maps:

- Finished product units sold (OTC decongestant market with PSE-containing products)

- Pseudoephedrine loading per unit (mg per tablet, mg per dose in gels/syrups, etc.)

- Conversion to API demand using product composition and typical manufacturing yield

Because pseudoephedrine can be sold as multiple dosage forms and strengths, the projection is sensitive to mix. The most reliable method in practice is:

- build a baseline OTC unit demand forecast

- apply a PSE share of the decongestant category by region

- convert API equivalents using average mg per dose and dosage-form mix

Sales projections (base, upside, downside)

The projection below is structured as global API demand index growth and revenue potential ranges. Exact absolute values depend on region-level regulatory posture and formulation mix, so this model expresses outcomes as scenario multipliers and revenue range logic designed for decision-making.

Scenario assumptions

- Base case: steady cold-season demand; pseudoephedrine maintains share in markets with stable OTC access; modest substitution in tighter-control regions.

- Upside case: regulatory stability plus effective retail channel execution and strong private-label penetration; minimal substitution displacement.

- Downside case: substitution accelerates in restricted markets; enforcement and access constraints reduce effective conversion; mix shifts away from PSE-containing combinations.

Projected growth rates for PSE-HCl (global)

| Year | Downside (YoY) | Base (YoY) | Upside (YoY) |

|---|---|---|---|

| 2026 | -2% to 0% | 2% to 4% | 4% to 7% |

| 2027 | -1% to 1% | 2% to 5% | 5% to 8% |

| 2028 | 0% to 2% | 3% to 6% | 6% to 9% |

| 2029 | 0% to 3% | 3% to 6% | 6% to 10% |

| 2030 | 1% to 3% | 3% to 7% | 7% to 11% |

Interpretation for business planning: The market behaves like a stable, seasonal category with regulatory drag and share shifts. Long-run growth is typically in the mid-single digits in the base case, with upside tied to share retention and distribution execution, and downside tied to substitution or stricter controls.

Translate growth into sales volume and revenue

To convert the growth forecasts into a working sales projection, use this pipeline math:

- API volume (kg) = Finished-dose units sold × pseudoephedrine per unit (mg) × (1 kg / 1,000,000 mg) ÷ manufacturing yield

- Revenue = API volume (kg) × average selling price (ASP) per kg

ASP drivers

- Regulatory compliance cost pass-through (higher documentation and batch controls)

- Supply-demand balance during peak cold seasons

- Raw material pricing and manufacturing capacity utilization

- Customer concentration (large contract deals can compress ASP)

Scenario revenue bands (index-based)

Assume a normalized 2025 revenue baseline of 100. Projected revenue index:

| Year | Downside index | Base index | Upside index |

|---|---|---|---|

| 2026 | 98 to 100 | 102 to 104 | 104 to 107 |

| 2027 | 99 to 101 | 104 to 109 | 109 to 112 |

| 2028 | 100 to 102 | 107 to 115 | 115 to 122 |

| 2029 | 101 to 103 | 110 to 121 | 122 to 130 |

| 2030 | 102 to 105 | 113 to 129 | 130 to 141 |

Use in planning: Treat downside as a low-single-digit deterioration band, base as low-to-mid single-digit growth with regulatory drag, and upside as mid-to-high single-digit growth if market share and distribution execution outperform.

What could change the trajectory quickly?

The fastest movers in PSE-HCl demand are not clinical, they are regulatory and channel execution.

Primary inflection triggers:

- Rules tightening for pseudoephedrine sales (quantity caps, behind-the-counter expansions, identification requirements)

- Retail compliance improvements (reducing friction that otherwise depresses purchase conversion)

- Finished product reformulation away from PSE (share loss)

- Capacity additions or disruptions among API suppliers (supply stability affects lost sales during peak seasons)

Go-to-market implications for an API supplier

For an API player, the commercial strategy tends to determine whether the supplier lands in the base or upside scenario.

Execution levers

- Regulatory-grade documentation depth (DMF readiness, batch traceability, audit performance)

- Supply reliability for peak seasons (cold-season lead time planning)

- Customer qualification speed for generic and finished-dose manufacturers

- Pricing discipline aligned to regulatory compliance costs

Channel strategy

- Prioritize customers whose finished product mix uses pseudoephedrine at stable dosages (reduces mix risk).

- Diversify across multiple dosage formats to reduce exposure to formulation shifts.

Key operating KPIs to track (commercial)

- OTC sell-through rate of PSE-containing decongestants in target regions

- PSE share of decongestant category (unit share, not just revenue share)

- Customer order stability across Q3-Q1 (cold season and refill patterns)

- ASP versus compliance cost index (documented margin protection)

Key Takeaways

- Pseudoephedrine hydrochloride demand is stable but shaped by seasonal OTC decongestant purchasing and diversion-control regulations.

- Global growth is most likely mid-single-digit in the base case, with upside tied to share retention and distribution execution and downside tied to substitution and stricter access controls.

- Sales projections for PSE-HCl should be built from finished-dose unit forecasts, adjusted for pseudoephedrine loading and manufacturing yield, with revenue sensitivity driven by ASP and compliance-related cost pass-through.

FAQs

1) Is pseudoephedrine demand mainly seasonal?

Yes. OTC decongestant purchasing concentrates in cold and allergy seasons, driving quarterly variability and peak-season supply requirements.

2) What is the biggest driver of volume changes?

Regulatory access and diversion-control enforcement, which affects customer purchasing friction and substitution behavior.

3) How do substitution products influence PSE-HCl sales?

Where pseudoephedrine access tightens, consumers and manufacturers shift to alternatives, reducing the pseudoephedrine share even when overall cold-season symptom incidence remains stable.

4) What determines ASP for pseudoephedrine hydrochloride?

Compliance and documentation costs, supply-demand balance during peak demand windows, manufacturing capacity utilization, and customer concentration in contract volumes.

5) What market outcome best predicts a supplier landing in upside vs downside?

Share retention with strong retail and customer execution puts outcomes closer to upside; formulation shifts away from PSE or intensified access constraints push outcomes toward downside.

References

[1] United Nations Office on Drugs and Crime (UNODC). Precursors and Chemicals Frequently Used in the Illicit Manufacture of Narcotic Drugs and Psychotropic Substances (Pseudoephedrine). UNODC.

[2] U.S. Drug Enforcement Administration (DEA). Combatting Methamphetamine Production: Regulations on Listed Chemicals, including pseudoephedrine. DEA.

[3] European Medicines Agency (EMA). Public information and regulatory frameworks relevant to pseudoephedrine-containing medicinal products. EMA.

More… ↓