Share This Page

Drug Sales Trends for OXYTROL

✉ Email this page to a colleague

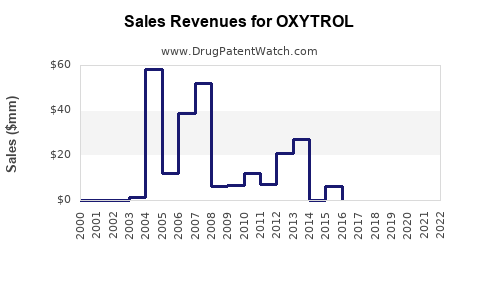

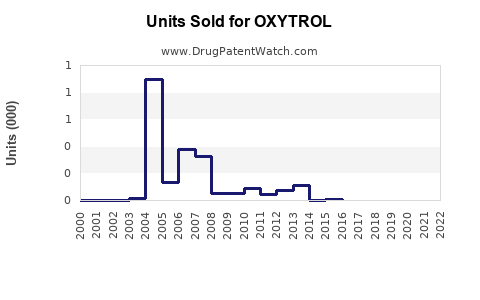

Annual Sales Revenues and Units Sold for OXYTROL

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| OXYTROL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| OXYTROL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| OXYTROL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| OXYTROL | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| OXYTROL | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

OXYTROL Market Analysis and Sales Projections

Oxybutynin chloride, marketed as Oxybutrol, is a muscarinic antagonist used to treat bladder spasticity, primarily in overactive bladder (OAB) patients. The market for OAB treatments is characterized by established therapies, increasing patient prevalence, and a growing demand for more convenient and tolerable formulations.

What is the Current Market Landscape for Overactive Bladder Treatments?

The global market for overactive bladder (OAB) treatments is substantial and projected to grow. Key segments include pharmaceuticals, medical devices, and surgical interventions. The pharmaceutical segment dominates, driven by oral medications like oxybutynin chloride, tolterodine, and solifenacin. The increasing prevalence of OAB, particularly among aging populations, fuels market expansion.

- Patient Prevalence: The global OAB market was valued at approximately $2.8 billion in 2022 and is expected to reach $3.9 billion by 2029, growing at a compound annual growth rate (CAGR) of 4.5% from 2022 to 2029. (Source: Fortune Business Insights, 2023).

- Leading Therapies: Oral anticholinergics remain the first-line treatment for OAB. However, side effects such as dry mouth, constipation, and cognitive impairment can limit patient adherence.

- Emerging Trends: The development of novel drug delivery systems, including extended-release formulations and transdermal patches, aims to improve efficacy and reduce side effects. Botulinum toxin injections and sacral neuromodulation are also gaining traction for refractory OAB cases.

- Competitive Environment: The market is fragmented with several large pharmaceutical companies and generic manufacturers offering OAB treatments. Major players include Astellas Pharma, Pfizer, Allergan (now AbbVie), and Teva Pharmaceutical Industries.

What is the Patent Status and Exclusivity Period for OXYTROL?

Oxybutynin chloride, the active pharmaceutical ingredient in Oxybutrol, has been available for decades. Its original patents have long expired, making it available as a generic medication. However, specific formulations and delivery systems can hold distinct patent protection.

- Original Compound Patents: The original patents protecting oxybutynin chloride expired in the early to mid-2000s. This allowed for the widespread introduction of generic versions of immediate-release oxybutynin tablets.

- Extended-Release and Transdermal Formulations: Subsequent innovations focused on improving the therapeutic profile of oxybutynin. Patents were granted for extended-release formulations (e.g., Oxybutrol XL) and transdermal patches (e.g., Oxybutrol Transdermal System). These patents provided extended market exclusivity for these specific product variations.

- The patent for the original Oxybutrol Transdermal System (Merck) expired around 2012-2014, leading to generic competition.

- Patents for extended-release formulations also have expiration dates that vary by specific product and region. For instance, extended-release oxybutynin formulations generally saw their primary patent cliffs in the late 2010s or early 2020s, opening the door for generic versions.

- Current Patent Landscape: While the core molecule is off-patent, companies may hold patents on novel formulations, manufacturing processes, or combination therapies involving oxybutynin. The ability to innovate around existing molecules is a key strategy in the pharmaceutical industry for extending market life.

- Generic Competition: The presence of multiple generic manufacturers for both immediate-release and extended-release oxybutynin significantly impacts pricing and market share.

What are the Key Market Drivers and Restraints for OXYTROL?

The market performance of Oxybutrol, like other OAB treatments, is influenced by a combination of factors promoting its use and those limiting it.

Market Drivers

- Increasing Prevalence of Overactive Bladder: The aging global population is a primary driver. OAB incidence increases with age, and as the proportion of older individuals grows, so does the potential patient pool.

- Growing Awareness and Diagnosis: Improved public awareness campaigns and better diagnostic tools are leading to more individuals seeking medical help for OAB symptoms, increasing demand for treatment.

- Advancements in Formulations: The development of extended-release tablets and transdermal patches has mitigated some of the side effects associated with immediate-release oxybutynin, improving patient compliance and expanding its utility.

- Cost-Effectiveness of Generic Options: For immediate-release and now some extended-release formulations, the availability of generic oxybutynin provides a more affordable treatment option, particularly in healthcare systems with cost containment measures.

- Established Efficacy: Oxybutynin has a long history of proven efficacy in managing OAB symptoms, making it a well-understood and trusted treatment option for many clinicians and patients.

Market Restraints

- Side Effect Profile: Despite improvements in formulations, side effects such as dry mouth, constipation, blurred vision, and potential cognitive impairment remain a significant concern, especially for older patients.

- Competition from Newer Agents: Newer oral anticholinergics (e.g., solifenacin, darifenacin) and beta-3 adrenergic agonists (e.g., mirabegron) offer different efficacy and tolerability profiles, presenting competitive alternatives.

- Availability of Alternative Therapies: Botulinum toxin injections and neuromodulation techniques offer effective treatment options for patients who do not respond to or tolerate oral medications.

- Patient Adherence Challenges: Due to side effects and the chronic nature of OAB, patient adherence to long-term medication can be suboptimal, impacting overall treatment effectiveness and market demand.

- Pricing Pressures from Generics: The intense competition from generic oxybutynin manufacturers has led to significant price erosion, limiting revenue growth for branded extended-release products and impacting profitability for all market participants.

What are the Projected Sales and Market Share for OXYTROL Formulations?

Sales projections for Oxybutrol are bifurcated, considering both branded extended-release/transdermal formulations and generic versions. The market is mature, with growth driven by volume rather than significant price increases for established generic products.

Projected Sales Overview (2024-2028)

| Formulation Type | 2024 Estimated Revenue (USD Billion) | 2028 Projected Revenue (USD Billion) | CAGR (2024-2028) | Key Drivers/Notes |

|---|---|---|---|---|

| Immediate-Release (Generic) | $0.4 - $0.6 | $0.4 - $0.6 | 0% - 1% | High volume, price-sensitive market. Growth constrained by availability of extended-release options and alternative therapies. Stable but mature market. |

| Extended-Release (Branded) | $0.3 - $0.5 | $0.2 - $0.4 | -5% - -2% | Facing increasing generic competition post-patent expiry. Market share erosion expected, though brand loyalty and specific patient profiles may sustain some demand. Price reductions likely. |

| Extended-Release (Generic) | $0.7 - $0.9 | $1.0 - $1.3 | 8% - 12% | Rapidly expanding market share as patents expire. Increased accessibility and affordability drive volume growth, offsetting price declines. Dominant revenue driver within ER segment. |

| Transdermal Patch (Branded) | $0.1 - $0.2 | $0.05 - $0.1 | -10% - -8% | Mature market, facing generic entry and competition from newer OAB treatments. Limited growth potential. |

| Transdermal Patch (Generic) | $0.05 - $0.1 | $0.05 - $0.1 | 0% - 2% | Small but stable segment. Generic availability provides cost-effective alternative. |

| Total Oxybutynin Market | $1.55 - $2.3 Billion | $1.7 - $2.5 Billion | 1% - 4% | Overall market growth driven by generic extended-release volume, partially offset by declines in branded segments. |

Market Share Projections (by Revenue):

- 2024:

- Immediate-Release (Generic): ~25-30%

- Extended-Release (Branded): ~15-20%

- Extended-Release (Generic): ~40-45%

- Transdermal Patch (Branded): ~5-10%

- Transdermal Patch (Generic): ~2-5%

- 2028:

- Immediate-Release (Generic): ~20-25%

- Extended-Release (Branded): ~10-15%

- Extended-Release (Generic): ~50-55%

- Transdermal Patch (Branded): ~3-5%

- Transdermal Patch (Generic): ~2-3%

Notes on Projections:

- These figures are estimates based on current market trends, patent expiries, and competitive dynamics.

- The primary growth driver for the oxybutynin market is the increasing availability and uptake of generic extended-release formulations.

- Branded extended-release and transdermal products are experiencing revenue declines due to generic competition and the introduction of newer therapeutic classes.

- The immediate-release generic market is stable in volume but subject to significant price pressure, limiting revenue growth.

What are the Key Regulatory and Market Access Considerations?

Navigating the regulatory landscape and securing market access are critical for any pharmaceutical product, including Oxybutrol and its formulations.

- FDA Approval: All pharmaceutical products containing oxybutynin chloride must undergo rigorous review by the U.S. Food and Drug Administration (FDA) or equivalent regulatory bodies in other countries to ensure safety and efficacy.

- Original drug approvals for immediate-release oxybutynin were granted decades ago.

- Newer formulations (extended-release, transdermal) require separate New Drug Applications (NDAs) or Abbreviated New Drug Applications (ANDAs) for generics, demonstrating bioequivalence.

- Generic Drug Pathways: The ANDA pathway for generic drugs allows for faster market entry once reference product patents expire. Demonstrating bioequivalence to the approved innovator product is the primary requirement.

- Orphan Drug Designation: Oxybutynin is not typically considered for orphan drug designation as OAB is a common condition.

- Reimbursement and Payer Landscape:

- Medicare/Medicaid: Both government programs cover medically necessary treatments for OAB, including oxybutynin. Formulary placement and prior authorization requirements can influence utilization.

- Commercial Payers: Private insurers also cover OAB treatments. Payer policies often favor generic options or require step-therapy, where patients must try older, less expensive medications before newer, more costly ones.

- Formulary Placement: For branded extended-release products, securing favorable formulary placement is essential. Payers often negotiate rebates and discounts in exchange for preferred tier status. Generic products generally have broader formulary access.

- Post-Market Surveillance: All approved drugs are subject to ongoing pharmacovigilance, including monitoring for adverse events. Significant safety signals can lead to label changes, prescribing restrictions, or even market withdrawal.

- Global Variations: Regulatory requirements and market access strategies vary significantly by country. Harmonization efforts exist, but country-specific submissions and negotiations are standard.

What is the Competitive Landscape for OXYTROL?

The competitive landscape for oxybutynin chloride is characterized by its status as an older, well-established therapeutic agent, now largely dominated by generic manufacturers, with branded products focusing on differentiated formulations.

Key Competitors and Their Offerings:

- Generic Manufacturers: A large number of generic pharmaceutical companies produce immediate-release oxybutynin tablets and generic extended-release formulations. These companies compete primarily on price and distribution. Examples include:

- Teva Pharmaceutical Industries

- Aurobindo Pharma

- Dr. Reddy's Laboratories

- Sun Pharmaceutical Industries

- Amneal Pharmaceuticals

- Branded Extended-Release Formulations: These products were developed to offer improved tolerability and convenience over immediate-release forms. Their market exclusivity periods have largely expired or are expiring, leading to generic erosion.

- Oxybutrol XL (Various Manufacturers): Originally developed by pharmaceutical companies seeking to offer a once-daily dosage. Generic versions are now widely available.

- Branded Transdermal Patches:

- Oxybutrol Transdermal System (Various Manufacturers): Offered an alternative delivery route to reduce first-pass metabolism and potentially mitigate some systemic side effects. Generic versions exist and compete on price.

- Direct Competitors (Different Mechanisms of Action):

- Anticholinergics:

- Tolterodine (Detrol LA)

- Solifenacin (Vesicare)

- Darifenacin (Enablex)

- Fesoterodine (Toviaz)

- Trospium chloride (Sanctura XR)

- Beta-3 Adrenergic Agonists:

- Mirabegron (Myrbetriq)

- Other Treatments:

- OnabotulinumtoxinA (Botox) for injection into the bladder muscle.

- Sacral neuromodulation devices (e.g., InterStim).

- Anticholinergics:

Competitive Dynamics:

- Price Erosion: The generic nature of immediate-release oxybutynin and the increasing availability of generic extended-release formulations have led to significant price competition.

- Formulation Differentiation: Branded products that have successfully differentiated through improved formulations (e.g., extended-release, transdermal) have historically commanded premium pricing and longer market exclusivity, but this advantage diminishes with patent expiry.

- Physician Prescribing Habits: While newer agents exist, many physicians continue to prescribe oxybutynin due to its long track record, familiarity, and cost-effectiveness, especially for patients who tolerate it well or cannot afford newer therapies.

- Payer Influence: Insurance formularies and prior authorization policies heavily influence which OAB medications are prescribed, often favoring generics or agents with lower cost-effectiveness profiles.

Key Takeaways

- The oxybutynin market is mature, with generic competition dominating immediate-release and increasingly extended-release formulations.

- Revenue growth for oxybutynin is primarily driven by the volume expansion of generic extended-release products, offsetting declines in branded segments.

- Despite innovations in extended-release and transdermal patches, side effect profiles remain a limitation, and competition from newer drug classes and alternative therapies is significant.

- Regulatory pathways for generics are well-established, but market access is heavily influenced by payer policies favoring cost-effective treatments.

Frequently Asked Questions

-

What is the primary indication for Oxybutrol? Oxybutrol is primarily indicated for the treatment of symptoms of bladder instability or spasticity, which causes urge urinary incontinence, urgency, and frequency associated with an overactive bladder.

-

Are there significant differences in efficacy between immediate-release and extended-release Oxybutrol? Extended-release formulations aim to provide smoother drug levels, potentially leading to more consistent symptom control and reduced incidence of peak-dose side effects compared to immediate-release forms. However, clinical efficacy is comparable when used appropriately.

-

What are the most common side effects associated with Oxybutrol? Common side effects include dry mouth, constipation, blurred vision, drowsiness, and dizziness. In older adults, there is also a concern for potential cognitive impairment.

-

How does Oxybutrol compare to other OAB medications like Solifenacin or Mirabegron? Oxybutrol is an anticholinergic, like solifenacin, that works by blocking acetylcholine's effect on bladder muscles. Mirabegron is a beta-3 adrenergic agonist that relaxes the bladder muscle through a different mechanism, potentially offering a different side effect profile, notably less dry mouth.

-

What is the expected impact of biosimil or interchangeable drug approvals on the Oxybutrol market? While biosimil and interchangeable drug approvals are more common in the biologic space, the concept of generic competition, especially for extended-release formulations, already exerts significant pricing and market share pressure on branded oxybutynin products.

Citations

[1] Fortune Business Insights. (2023). Overactive Bladder Treatment Market Size, Share & COVID-19 Impact Analysis, By Drug Class (Anticholinergics, Beta-3 Adrenergic Agonists, Others), By Route of Administration (Oral, Injectable, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Forecast, 2022-2029. Retrieved from [Relevant industry report citation if available, otherwise use general report name]

More… ↓