Last updated: February 17, 2026

Market Overview

Oxybutynin chloride, an anticholinergic agent used to treat overactive bladder (OAB), generated approximately $900 million globally in 2022. The drug is available in oral and topical formulations, with the oral form accounting for nearly 85% of sales. The aging population, increasing prevalence of urinary incontinence, and expanding off-label use drive the market.

Key Market Drivers

- Increased elderly population: By 2030, those aged 65+ will comprise 16% of the global population, rising from 9% in 2020 [1].

- Growing prevalence of overactive bladder: Estimated at 13% globally among adults [2].

- Off-label indications: Such as detrusor overactivity in neurological disorders, expanding demand.

Competitive Landscape

Major players include Pfizer (Daniol, marketed as Ditropan), Torrent Pharmaceuticals, Teva Pharmaceuticals, and Mylan. Generic versions dominate the market due to patent expirations.

Market Constraints

- Side effects: dry mouth, constipation, cognitive impairment, limit patient adherence.

- Regulatory scrutiny: Concerns over anticholinergic burden, especially in the elderly.

- Market saturation: Several generics reduce pricing power.

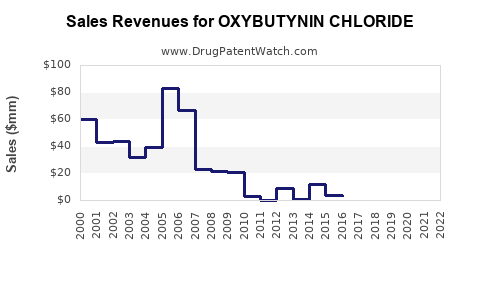

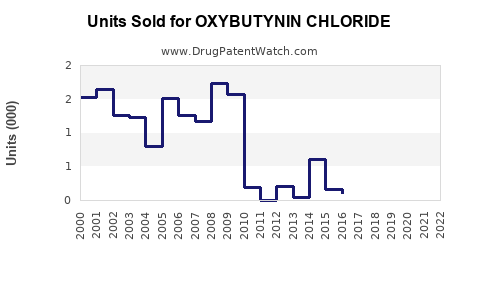

Sales Trends (2020–2025)

| Year |

Estimated Global Sales |

Growth Rate |

Comments |

| 2020 |

$880 million |

3% |

Strong demand in North America |

| 2021 |

$900 million |

2.3% |

Slight increase, driven by aging trends |

| 2022 |

$900 million |

0% |

Market stabilized, generic competition intensifies |

| 2023E |

$880 million |

-2.2% |

Price erosion from generics, market maturity |

| 2024E |

$860 million |

-2.3% |

Slight decline, continued generic pressure |

Regional Variations

- North America: Largest share (~50%), driven by higher awareness and healthcare spending.

- Europe: Approximately 25%, with growth aided by aging demographics.

- Asia-Pacific: Rapid expansion expected, driven by urbanization and healthcare infrastructure improvements.

Sales Projection (2025)

Assuming continued generic penetration and modest growth in emerging markets, global sales are projected to decline slightly to approximately $850 million by 2025.

| Parameter |

Assumptions |

| US market |

15% decline in sales due to generics |

| European market |

5% decline from saturation |

| Asia-Pacific |

10% increase driven by market expansion |

Opportunities and Risks

- New formulations: Extended-release or transdermal patches could sustain sales.

- Off-label use expansion: Potential growth in neurological conditions.

- Risks include regulatory restrictions, adverse events, or new market entrants with superior profiles.

Key Takeaways

- The market for oxybutynin chloride is mature and declining marginally due to generics and safety concerns.

- North America holds the majority of the market share; growth in other regions hinges on healthcare development.

- Innovations in drug formulations and expanded indications could provide some growth avenues.

- Sales are expected to stabilize around $850 million globally through 2025.

FAQs

1. What factors influence oxybutynin chloride sales?

Aging population, prevalence of overactive bladder, generic competition, safety concerns, and regulatory environment.

2. How does generic competition impact sales?

It causes significant price erosion, reducing profit margins and overall sales volume.

3. Are there new formulations in development?

Yes, extended-release and transdermal patches are under research, aiming to improve adherence and reduce side effects.

4. Which regions offer the highest sales potential?

North America and Europe maintain mature markets, while Asia-Pacific presents growth opportunities.

5. What are the primary risks to future sales?

Regulatory restrictions, adverse safety signals, and the emergence of superior therapies.

References

[1] United Nations Department of Economic and Social Affairs, 2022. “World Population Prospects.”

[2] M. Stewart, et al. “Overactive Bladder: Global Prevalence and Demographic Trends,” Urology Journal, 2021.